We have put together a list of questions & answers that advisers & planners regularly ask us.

If you have questions we have not answered, please get in touch by emailing enquiries@ibossltd.co.uk or calling 01423 878 840.

We have put together a list of questions & answers that advisers & planners regularly ask us.

If you have questions we have not answered, please get in touch by emailing enquiries@ibossltd.co.uk or calling 01423 878 840.

Yes, but currently only the Core MPS portfolios. Distribution Technology have reviewed and profiled 5 of the 8 discretionary portfolios within the risk profiles used on Dynamic Planner. The main objective of the DT risk profiles and fund risk profiling service is to provide you and your clients with a meaningful measure of the long-term investment risk of fund strategies and a mechanism for selecting solutions appropriate for investor appetite and capacity for risk.

The profiles which DT have assigned to the portfolios are set out below.

Portfolio | Assigned risk profile

Core MPS Portfolio 1 | ![]()

Core MPS Portfolio 2 | ![]()

Core MPS Portfolio 4 | ![]()

Core MPS Portfolio 6 | ![]()

Core MPS Portfolio 7 | ![]()

Core MPS Portfolio 8 | ![]()

Please email Kevin@ibossltd.co.uk for a copy of our risk profile report.

Yes, but currently only on the Core and Sustainable ranges.

Risk Ratings are numbered from 2 to 10, where 2 is a solution that has a very cautious investment

approach, and 10 a speculative approach. These match Defaqto’s client Risk Profiles, which range from 1 to

10, and where a client with a Risk Profile of 1 would be most suited to investing in bank account

cash.

The highest risk rating also has an upper boundary, and may not be suitable for clients wishing

to invest in a very high risk, unbound, solution.

The Risk Ratings that Defaqto have assigned to the portfolios are set out below.

Portfolio | Risk Rating

Core MPS Portfolio 0 | ![]()

Core MPS Portfolio 1 | ![]()

Core MPS Portfolio 2 | ![]()

Core MPS Portfolio 3 | ![]()

Core MPS Portfolio 4 | ![]()

Core MPS Portfolio 5 | ![]()

Core MPS Portfolio 6 | ![]()

Core MPS Portfolio 7 | ![]()

Core MPS Portfolio 8 | ![]()

Sustainable MPS Portfolio 1 | ![]()

Sustainable MPS Portfolio 2 | ![]()

Sustainable MPS Portfolio 3 | ![]()

Sustainable MPS Portfolio 4 | ![]()

Sustainable MPS Portfolio 5 | ![]()

Sustainable MPS Portfolio 6 | ![]()

Sustainable MPS Portfolio 7 | ![]()

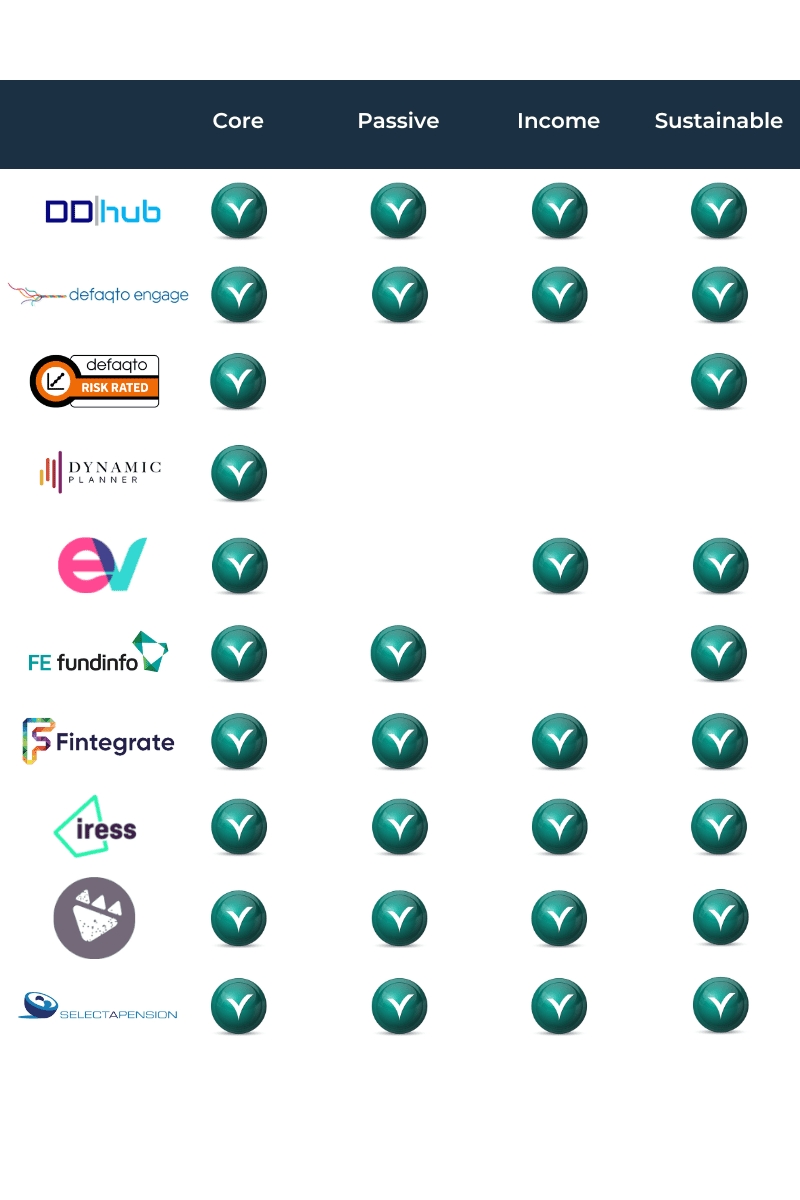

Defaqto’s end-to-end financial planning software solution Engage allows advisers to extract their clients’ mandates in a compliant manner, and to find suitable funds to match these.

The MPS range is available on the following research tools:

The IBOSS discretionary MPS range on platform is 5 Star Rated, this shows it provides one of the highest quality offerings on the market. Star Ratings look at the features and benefits of a product or propositions, rather than solely focusing on cost.

In addition, the Core MPS is 5 Diamond Rated, meaning it offers an excellent proposition relative to the peer group across charges and other fund manager features including the business, team and investment process.

There are various ways an agreement can be arranged between a financial adviser and a Discretionary Fund Manager (DFM).

Two of the main options are:

Agent as Client (AAC)

Reliance on Others (ROO)

There are advantages and disadvantages to both relationships, and it is vital that advisers understand the difference between the two popular DFM MPS agreements. The key objective is that the adviser, DFM and investor understand how the arrangement has been structured and the responsibilities each party has, as well as any possible implications.

Click here to read or download our ‘DFM Agreement Options’ adviser guide

The value assessments for each of the individual IBOSS DFM MPS ranges can opened in PDF by clicking the link underneath the corresponding range on the Managed Portfolio Service page here.

The IBOSS OEIC Fund Range is 4 Diamond rated as a fund family, meaning the funds offer a good proposition relative to the peer group across charges, performance, risk shape and other features.

Each IBOSS fund has also been rated individually within the Multi-Manager Returned Focused category. IBOSS fund 2 has been 5 Diamond rated, offering an excellent proposition relative to the peer group across charges, accessibility, performance and other features. IBOSS funds 1, 4 and 6 have all achieved 4 Diamonds.

Yes. Distribution Technology have reviewed and profiled the 4 funds offered by IBOSS Asset Management within the risk profiles used on Dynamic Planner. The main objective of the DT risk profiles and fund risk profiling service is to provide financial advisers and their clients with a meaningful measure of the long-term investment risk of fund strategies and a mechanism for selecting solutions appropriate for investor appetite and capacity for risk.

The profiles which DT have assigned to the funds are set out below.

Fund | Assigned risk profile

MGTS IBOSS 1 | ![]()

MGTS IBOSS 2 | ![]()

MGTS IBOSS 4 | ![]()

MGTS IBOSS 6 | ![]()

Please email Kevin@ibossltd.co.uk for a copy of our risk profile report.

The OEIC is available on the following platforms:

If your preferred platform isn’t listed, please let us know and we will try to facilitate it. We are led by adviser demand.

Also available through Elevate, Advance by Embark, Fundment, Hubwise, Parmenion, Praemium and Utmost Wealth.

We don’t want to be constrained by an asset allocation tool.

Therefore, when creating the portfolios IBOSS studied numerous economic principles, including Harry Markowiztz’s modern portfolio theory, and those of Watson Wyatt and respected fund managers, as well as long term historical performance data. We then compiled our core asset allocation defining the percentages allocated to each asset class.

The emphasis was on:

Historical data and economic context

High levels of diversification and low levels of correlation

Geographical market conditions

Using multiple funds in each sector further reduces volatility, as no fund manager gets it right every time and it reduces the risk of one manager adversely impacting on the performance.

We consequently hold approximately 35-40 funds in each portfolio.

The reason for the large number of funds is our preference for multiple funds in each sector to offset manager and style risk.

This has proved to be a very effective strategy to reduce overall drawdowns.

Simply give us a call or send in your question by email and we’ll make sure you get an answer.

Our Investment Team enjoy speaking to advisers and planners, and feel this level of personal interaction helps them stay in touch with client concerns.

Please contact jack@ibossltd.co.uk

Two potential advantages of an ETF over a passive are:

The first point doesn’t really interest us, as we tend to take relatively long term positions. We would not choose to use a passive or ETF to time markets, instead we would use them to either maintain diversification of the portfolio or purchase cheap beta to a broad index should a market look fundamentally cheap.

The second point is more interesting, the wide range of ETFs available mean that you can get exposure to fairly niche sectors or subsectors that passive products don’t necessarily cater for. This being said, we tend to take a broad, flexible view when picking funds, preferring to leave alpha generation to the underlying managers. Picking a specific sector or geographical ETF is taking that decision out of the managers hands and into ours instead, this is not our core competency which is selecting the very best managers, who get most decisions right most of the time, and constructing fully diversified investment offerings.

That being said, we have previously held the Physical Gold ETC in the OEIC funds as a defensive position and diversifying position. So we will use ETF/ETCs should we feel it necessary.

A disadvantage of the ETF proposition in comparison to Passives is:

Basically, if we are not using the advantages of an ETFs flexibility then, in our opinion, we should take advantage of the cost benefits of passives.

Governance of the Risk Management framework is the ultimate responsibility of the Board of Directors, which performs the Governing Function of the Firm under the supervision of the ACD. The Board of Directors are responsible for all aspects of the business, including setting the culture and ensuring that the firm acts honestly, fairly, professionally and independently.

Your investment will be spread across one or more of the IBOSS OEIC sub-funds. Unlike a bank, Margetts, our Authorised Corporate Director (ACD), do not hold client assets on their balance sheet.

The MGTS IBOSS OEIC sub-fund assets are held by the depositary, Bank of New York Mellon Ltd, which is one of the biggest trustee / depositary and custodians in the world. The assets held by Bank of New York Mellon Ltd are ring fenced as a separate legal entity, with the exception of some cash which is held on deposit with the Bank of New York Mellon Ltd. The cash is held to the order of the sub-funds; this does not include money in transit but only when it arrives into the fund and not before or after leaving.

In the unlikely event that Margetts fails, the most likely action would be that the depositary would appoint a replacement operator (referred to as the Authorised Corporate Director), or return your investment plus any gain or loss.

There should be no direct effect from this action other than the normal movements of the underlying assets and a change the Authorised Corporate Director.

Margetts Fund Management is a regulated firm who are also required to hold reserves, which in a worst case scenario should allow the firm to close in an orderly fashion.

In the very unlikely event that Bank of New York Mellon fails, the most likely action would be that the fund is moved to another depositary and there could be a short delay in your ability to trade in or out of the fund.

Whilst an absolute guarantee cannot be provided, OEICs are regarded as one of the most secure asset structures within the UK market. The funds are UK Authorised Collective Investment Schemes and are authorised and regulated by the Financial Conduct Authority.’

In the unlikely event of a failure of Margetts, which causes a loss, the Financial Services Compensation Scheme could become available.

Again, another common, and very sensible, question.

Whilst Chris heads up our Investment Team, it is just that, a team. If Chris were unable to carry out his duties in the short-term Chris Rush would take charge.

Because we follow a house view, life would continue unchanged with the same investment approach and philosophy, until Chris returned to work.

If Chris were unable to return to work our Continuity Plan provides for resources to replace key members of our team who can no longer fulfil their role.

Whilst we don’t set any minimum investment amounts, depending on the platform of choice there may be some restrictions.

However, in the majority of cases, this is normally as low as £100.

{kind=link}