This update covers the period, year-to-date, up to September 12th. This period has been one of the most successful in IBOSS history, and much of that success can be somewhat surprisingly attributed to Trump’s second presidency. His second term in office has brought an end to the extended period of the US being the most prominent destination for many international assets, including stocks, bonds, and currency. In fact, while money is still flowing into US equities, for the first time, overseas buyers are now buying more of them hedged than unhedged. While it remains the biggest and most important market for all these asset classes, the search for alternatives across much of the globe, and the relative outperformance of other geographies, marks a paradigm shift in investing behaviours.

Making the World Ex US Great again… again

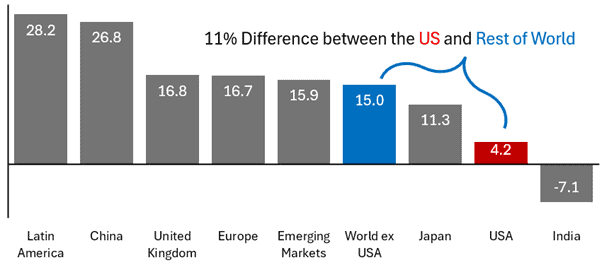

We have made this point in previous performance updates, but with so much positive news in the press surrounding investment returns, it is worth retreading the same ground. Despite their recent rally, US equities continue to lag most regions this year. In fact, the US is the worst-performing developed market by quite some margin.

The chart below highlights a broader basket of equities. Of note is the performance from emerging markets, particularly Latin America and China. This may come as a surprise to some, considering both regions have been under considerable scrutiny by the US president and have often been the focus of tariff discussions.

Fig 2: MSCI Index Returns – Year to date to 12/09/2025

As many readers will know, we often talk about the benefits of diversification. While it is widely accepted that diversification can protect investors in falling markets, recent market performance shows that diversification can also be incredibly powerful in rising markets, as portfolios gain exposure to a broader selection of opportunities.

Asset Allocation accounts for (insert figure here) of total returns.

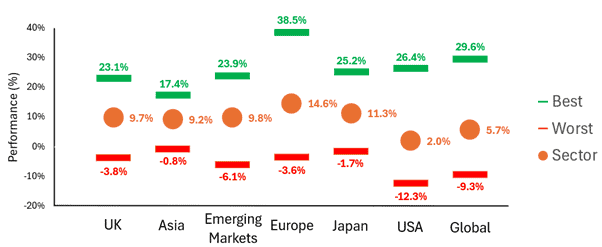

We have all likely heard the phrase that asset allocation accounts for a considerable portion of overall portfolio returns. However, this year, while it has been important, fund selection has also played a vital role.

The chart below indicates the best-performing funds in a sector, the worst-performing funds, and the sector average. As you can see, it has been very possible to get the asset allocation call correct yet still experience returns well outside what you expected.

In fact, across all regions, it has been possible to generate negative returns this year if you invested in the wrong fund. We can talk about fund selection all day, but a key contributor to performance this year for all our ranges has been fund selection.

Spread of fund returns this year – IA Sectors to 31/08/2025

All that Glitters is Gold … and commodities haven’t done so badly either

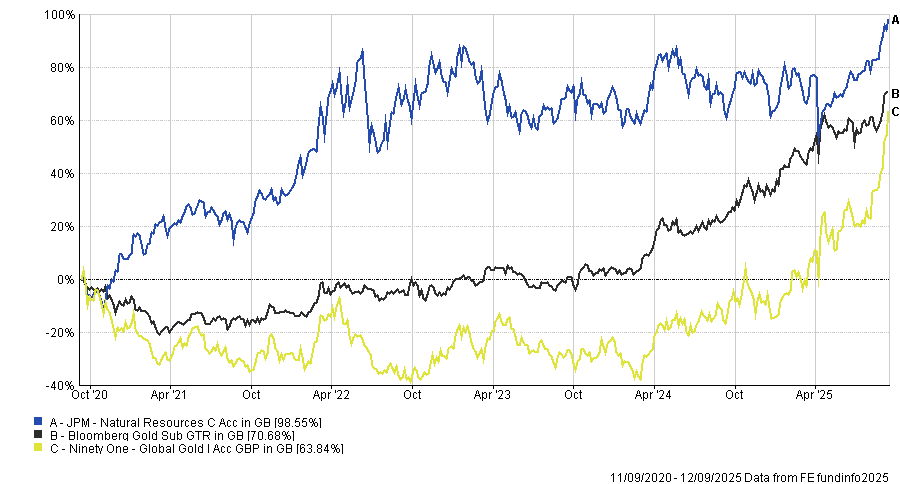

Gold has continued to shine in recent months, with the price rallying around 6.6% from August through September 12th. Within our portfolios, JPM Natural Resources and Ninety One Global Gold, both of which hold gold miners, have delivered particularly strong results. Over the same period, Ninety One rose an impressive 35%, while JPM gained 9%. Although these remain relatively minor positions in the portfolios, they have made a meaningful contribution both for the month and for the year.

We are often asked about this Ninety one fund in particular, and whether the best of its performance is already behind us. While it is impossible to say with certainty, we continue to hold the fund as a diversifying source of return. Historically, gold has tended to perform well during periods of uncertainty. This, combined with significant purchases by central banks globally, has supported both gold and gold miners, leading to the strong run we have seen.

The chart below shows that the fund’s phenomenal returns this year have brought it back in line with the gold price over the past five years, following a period where it had been starting from a relatively low base.

5 year performance to 12/09/2025

Performance Review

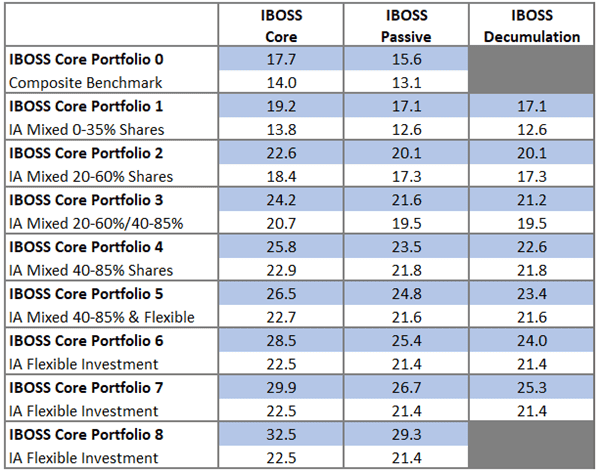

August delivered another strong month for the IBOSS ranges. All Core and Decumulation portfolios outperformed their IA benchmarks, with most of the Passive range also ahead.

Perhaps more striking is how this strength translates into the longer term. The chart below shows three-year performance for Core, Passive, and Decumulation portfolios, all of which have outperformed their peers.

It is worth remembering that nearly three years have passed since interest rates began rising to combat inflation. Over this period, investors have been rewarded for holding a more diversified mix of assets.

3 Year Performance against benchmark to 12/09/2025

Positioning and Outlook

We remain firmly focused on diversification across assets. While this update has primarily highlighted equities, our portfolios also hold a wide range of other asset classes, including property, fixed income, commodities, and gold. Each has played a role in delivering positive outcomes this year, with diversification once again proving its value not just as protection in downturns but also as a driver of returns in rising markets.

So, US equities remain the clear laggards in global markets. At the same time, emerging regions such as Latin America and China have delivered surprisingly strong performance, despite ongoing political and trade tensions. Careful fund selection has been critical, with the spread of returns across regions and sectors showing how the right choices can make a significant difference to outcomes. Small positions in areas such as gold miners have also added meaningful contributions, highlighting the benefits of a broad opportunity set.

Looking ahead, uncertainty around interest rates, inflation, and global growth remains. This backdrop continues to favour a diversified approach that does not rely too heavily on any single market or theme. By combining asset allocation with careful fund selection and by maintaining exposure to a wide mix of asset classes, our portfolios are well-positioned to navigate the challenges and opportunities of the months to come.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 267.9.25