Consumer Duty

The FCA’s consumer duty is a set of rules and principles aimed at ensuring financial firms prioritise the best interests of their customers, fostering fair treatment and transparency.

Consumer duty came into force on July 31, 2023 for all new products and services, as well as existing products or services that are open for sale or renewal.

The new rules set clear expectations for all firms in the distribution chain that provide products or services for retail clients to raise their standards and ensure that what they deliver is fit for purpose and offers fair value.

Our Approach to Consumer Duty

IBOSS puts retail customers at the heart of our business by providing products and services designed to meet customer needs and treating them fairly.

We are dedicated to supporting financial advisers, serving as both manufacturer and distributor.

Consumer Duty is embedded in all business areas and all staff have received the relevant training and will continue to develop their knowledge in this area.

We maintain close collaboration with financial advisers and industry experts to ensure we actively continue to enhance our services to promote good consumer outcomes.

Consumer Understanding

IBOSS must ensure financial advisers and planners fully understand all of the content and material that we provide, so that they can make informed decisions regarding products and services that best meet their clients’ needs.

We work closely with advisers when retail client communication is produced and have introduced opportunities for clients to feedback on their level of understanding. Additionally, we test end client communication with non-financial individuals before it is distributed. We continue to monitor the feedback and share this with the respective financial adviser. Where possible, we improve our future communications based on the relevant feedback received and report the results to the board of directors each quarter.

We strive to continually improve our communications, as well as how we offer the ability for clients to share their level of understanding.

IBOSS Support Material

We have created several documents to assist advisers and planners with consumer duty requirements. Please see the links below to download our Model Portfolio Value Assessments and our Target Market documents.

Model Portfolio Value Assessments

Model Portfolio Target Markets

How often will you update your Value Assessments?

Our Value Assessments will be reviewed and updated at least annually or sooner if there is a regulatory recommendation or a significant change to our service.

How do you make decisions on the target market?

IBOSS model portfolios are regularly monitored to ensure they meet the target market and have been distributed appropriately.

Please see the Model Portfolio Target Market documents above for more information.

What is your approach to vulnerable clients?

The financial adviser assesses the retail client for characteristics of vulnerability.

If they need specific assistance or support, advisers can inform us and we will endeavour to support their requirements where appropriate.

Under the ‘Reliance on Others’ agreement, we must be notified if there are any considerations we need to account for when providing our services to the investor.

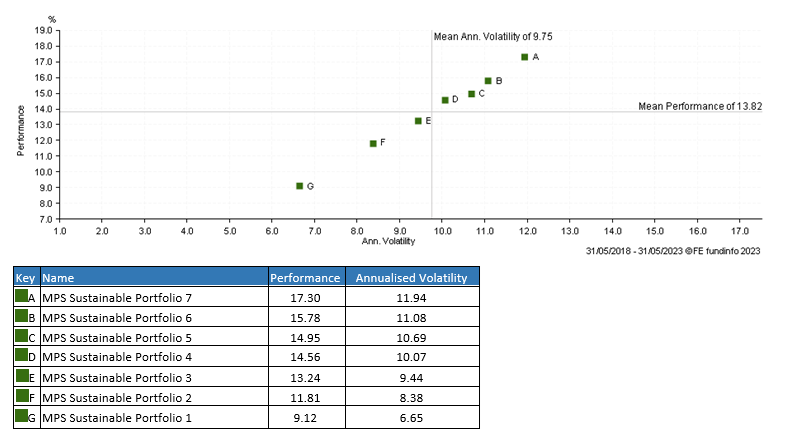

How do you risk rate the portfolios?

We use volatility to assign a risk rating to each portfolio. The scatter chart below demonstrates that the portfolio number reflects the risk taken (as measured by volatility) relative to other portfolios in the range. This information is then provided to support the Financial Adviser when completing their own risk questionaires.

FCA Support Material

In June 2023 the FCA published 10 questions for firms to consider:

- Are you satisfied your products and services are well designed to meet the needs of consumers in the target market, and perform as expected? What testing has been conducted?

- Do your products or services have features that could risk harm for groups of customers with characteristics of vulnerability? If so, what changes to the design of your products and services are you making?

- What action have you taken as a result of your fair value assessments, and how are you ensuring this action is effective in improving consumer outcomes?

- What data, MI and other intelligence are you using to monitor the fair value of your products and services on an ongoing basis?

- How are you testing the effectiveness of your communications? How are you acting on these results?

- How do you adapt your communications to meet the needs of customers with characteristics of vulnerability, and how do you know these adaptions are effective?

- What assessment have you made about whether your customer support is meeting the needs of customers with characteristics of vulnerability? What data, MI and customer feedback is being used to support this assessment?

- How have you satisfied yourself that the quality and availability of any post-sale support you have is as good as your pre-sale support?

- Do individuals throughout your firm – including those in control and support functions – understand their role and responsibility in delivering the Duty?

- Have you identified the key risks to your ability to deliver good outcomes to customers and put appropriate mitigants in place?

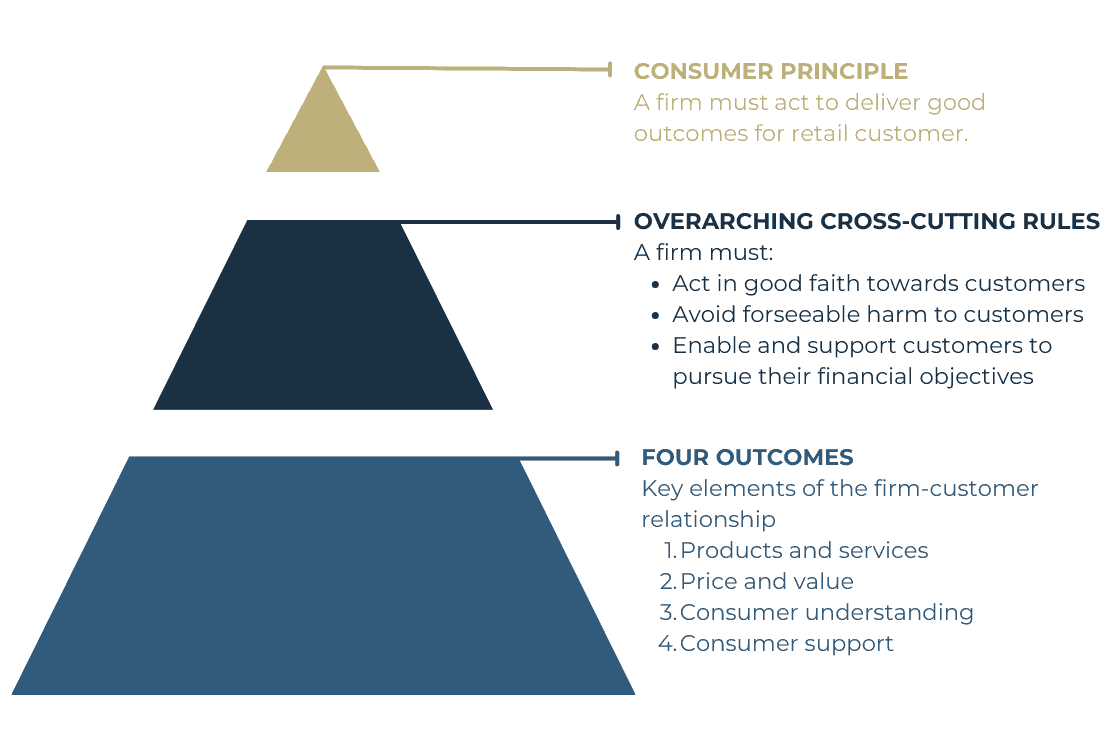

Consumer Duty’s 3 Key Elements

Helpful resources by the FCA

Consumer Duty – information for firms | FCA