Clients often look to their advisers for clarity and reassurance during turbulent market periods. In the first part of this blog, we covered some of the questions we had received in the aftermath of the Trump tariff sell-off. Since then, we have received many more questions from concerned advisers and their clients. These additional questions can be broadly categorised into two groups. The first one has more questions about what an investor should do during heightened market uncertainty. The second one is something that many people haven’t considered for many years, if at all. Is the policy of ‘Sell America’ part of a paradigm shift or a temporary phase before pre-2.0 Trump market conditions return?

What should I be doing right now?”

Answer:

Periods like this can create a strong urge to act—but the most valuable thing many investors can do is stay invested, remain properly diversified, and avoid making emotional decisions. It’s important to remind clients that markets have navigated wars, recessions, pandemics, and political upheaval in the past—and over time, portfolios that stayed the course typically recover and deliver strong returns.

Exposure to various asset classes and geographies allows portfolios to adapt to changing conditions without needing to chop and change constantly. Long-term wealth is rarely built through reactionary decisions—but rather by being positioned correctly and holding your nerve through the volatility. We all know that the idea is to buy assets when they are cheap and sell them when they are expensive. If somebody runs to cash after a market sell-off, they are hard-wiring for the opposite outcome.

Why Stay Invested

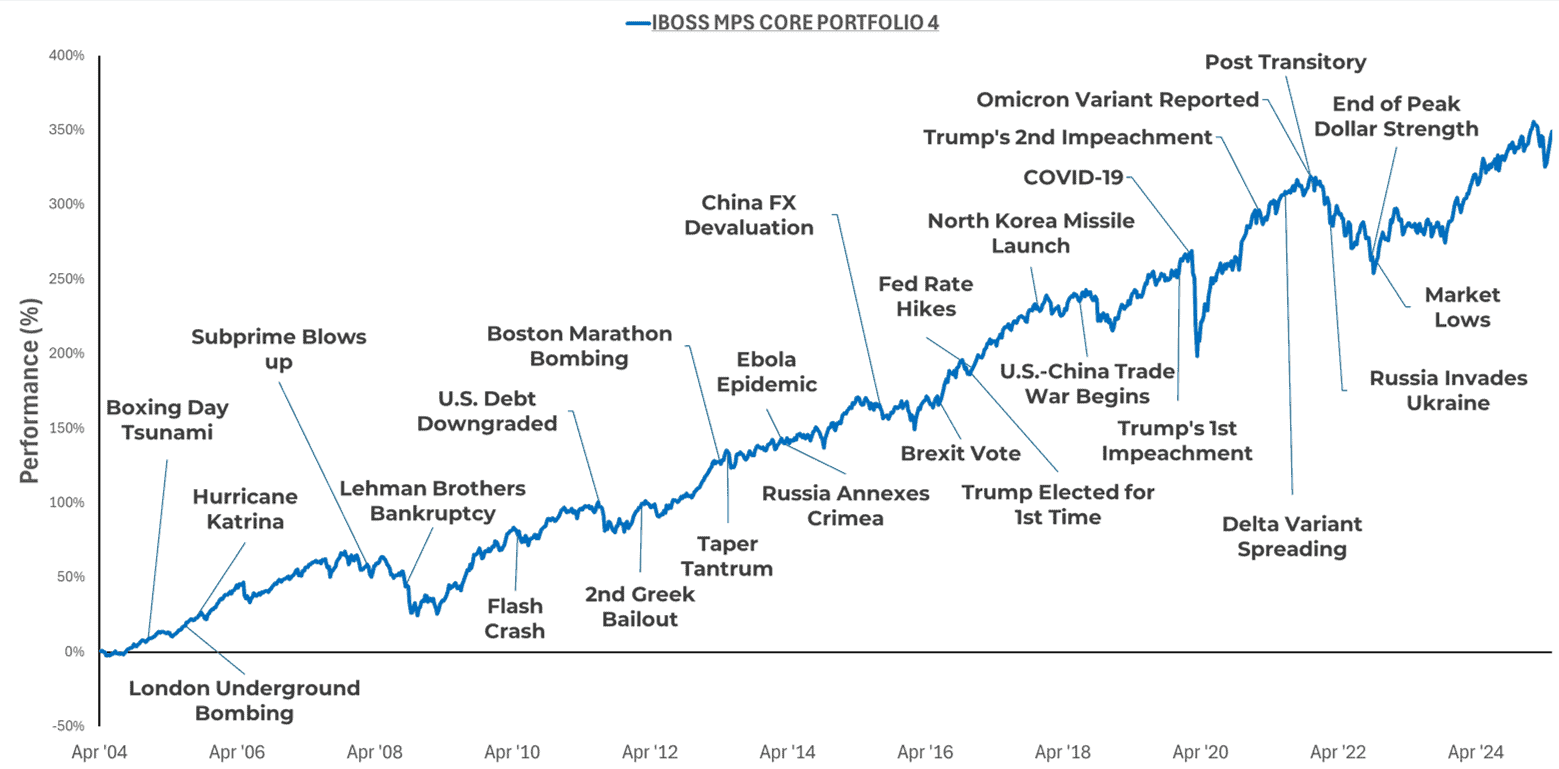

IBOSS Core MPS Portfolio 4 Performance > 01/04/2004 – 15/05/2025

The DFM MPS Core range launched on 1 November 2018. Performance figures before this date are simulated, based on the actual asset allocation and fund selection used by IBOSS Limited in its Portfolio Management Service from 31 October 2008. Simulated performance prior to November 2008 is based on back-tested assumptions and does not represent actual performance. Past and simulated performance are not reliable indicators of future results.. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

“Are we in a bear market, and why would it matter?”

Answer:

Not quite—but we’re certainly flirting with one.

A bear market is typically defined as a sustained downturn where a stock index closes 20% or more below its most recent peak. This threshold signals widespread investor pessimism and often a sense of panic about the market outlook. While specific indices and sectors, particularly those tied to US equities, AI-driven tech, or tariff-sensitive industries, have come close to that level, just as quickly, we have seen a rapidly rising market led once again by the US retail contingent. Many other geographies didn’t see anything like the falls in the US. Simply put, they created the problem and would have to own it.

However, the market sentiment right now reflects many of the same dynamics you’d expect in a bear market: uncertainty, nervousness, and sharp daily moves. Much of this is driven by short-term headline risk—tariff announcements, geopolitical tensions, conflicting political messaging, and major structural shifts in global leadership. These forces create volatility and market swings but don’t necessarily reflect the assets’ underlying value or long-term prospects.

Predicting when (or if) markets will officially enter or exit bear territory is notoriously tricky—even for seasoned professionals. More importantly, history shows that markets often recover when investor sentiment is still negative. Sharp rebounds can and do happen before the broader picture feels settled.

This is why timing the market is so risky. Missing even a few of the best-performing days during a volatile period can significantly impact long-term returns. Remaining invested in a diversified, actively managed portfolio puts clients in the best position to benefit when the recovery begins—whether next week, next quarter, or further down the line.

“Are there any opportunities you see right now despite the chaos?”

Answer:

Despite current volatility, compelling opportunities are emerging across several areas—beyond the traditional defensive plays.

With trust in the US market regime shaken, other regions such as Europe, Latin America and parts of Asia are adapting quickly and creating potential structural tailwinds. For instance, the EU appears more unified than it has been in years. Latin America is actively diversifying its trade partners, and China is pushing domestic stimulus as it adjusts to a post-globalised world. These shifts create opportunities for investors willing to look beyond the US-centric playbook of the last decade.

There’s also renewed opportunity within active fixed income. Recent bond market dislocations—caused by erratic policy movements, inflation fears, and geopolitical disruption—have widened the gap between passive and active bond strategies. Skilled managers who can navigate interest rate changes, sector rotations, and policy noise are better placed to take advantage of these inefficiencies.

Gold also stands out as an attractive option in the current environment. It recently reached all-time highs, and although this has led to some nervousness among investors, the fundamentals remain strong. Unlike previous hype cycles—such as during the AI boom—gold’s appeal is rooted in profound historical and macroeconomic relevance.

Three primary reasons exist for maintaining or increasing gold exposure: a hedge against inflation and currency devaluation, protection against conflict and trade tensions and diversification benefits.

It’s worth noting that central banks are currently some of the biggest buyers of gold—crucially, they are not price-sensitive. That’s a very different dynamic from, for example, retail investors piling into overvalued tech stocks during the peak of the AI bubble. Gold, as a non-yielding asset with no earnings estimates to miss, operates on an entirely different basis and has proven its resilience over millennia.

“The situation in the US is concerning; shouldn’t we invest elsewhere?”

Answer:

We have had more questions from clients voicing concern about the US than at any time in our seventeen-year history. While US equities have performed strongly over the last decade, the environment has changed. The combination of tariff uncertainty, political volatility, and declining trust in US leadership suggests the dominance of US assets may not continue in the same way. Whilst it might be easy to dismay client concerns emanating from the chaos in America, we think it’s worth reminding ourselves that the clients don’t care about the adviser’s or asset manager’s benchmarks. They won’t thank anybody for pushing them into a more concentrated portfolio full of expensive assets because of the career risk of staying properly diversified.

That doesn’t mean avoiding US exposure entirely, but it points to the importance of broad global diversification. Investors should avoid concentrating solely in any one region or theme, particularly when the global landscape is evolving. One of the hardest things to do in investing is to change your opinion about an asset. The second Trump presidency and the commoditisation of AI, starting with DeepSeek, have fundamentally altered the investing landscape. Investors who can get their heads around the new paradigm and invest based on the world as it is now and not as it was before have a significant advantage over their peers.

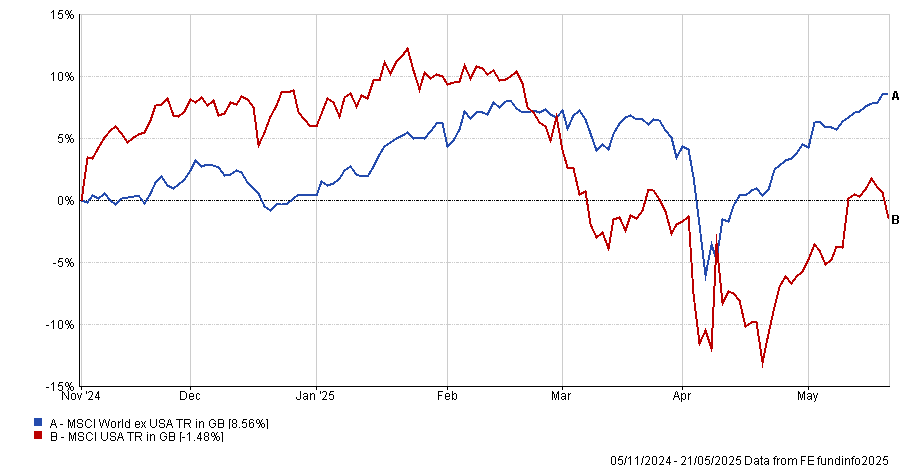

Trump’s 2.0 USA Vs The World ex USA > 05/11/2024- 21/05/2025

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 133.5.25