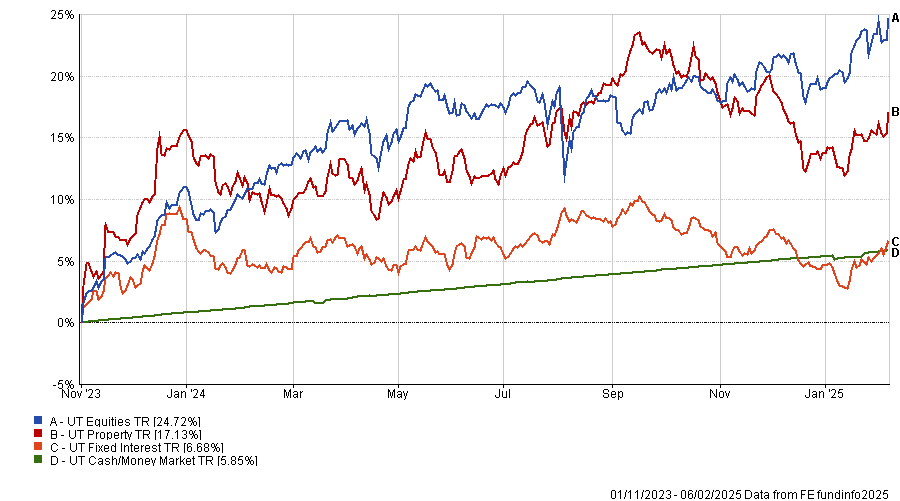

This update covers the period up to January 9th. As usual, we have taken the basic asset class chart (fig.1) back to the end of October 2023, the latest full Powell pivot, where he signalled victory over inflation and strongly suggested rate cuts were coming in 2024.

Macro & Markets

January is behind us, and it has been an eventful start to the year. On 15 January, Donald Trump officially took office, and while markets had been bracing for impact since his election victory last year, even the keenest minds would have struggled to predict the speed and scope of his immediate policy moves.

One area where Trump wasted no time was tariffs. Below, we break down the tariff policies already shaping global trade in 2025.

Tariffs on Canada and Mexico: A Rocky Start

President Trump imposed a 25% tariff on Canadian and Mexican imports, citing illegal immigration and drug trafficking concerns. After negotiations, the US agreed to a 30-day pause as both countries pledged to strengthen border security and combat drug trafficking.

Tariffs on China: The Trade War Resumes

The U.S. imposed a 10% tariff on Chinese imports, citing China’s failure to stop fentanyl precursor exports. In response, China placed 10–15% tariffs on U.S. goods, including crude oil and automobiles, and restricted rare earth metal exports.

The Columbian Tariffs that never were

One of the most dramatic (and short-lived) trade conflicts came from an unexpected source: Colombia. In late January 2025, Colombia’s refusal to accept deported migrants on US military planes led President Trump to impose 25% tariffs on Colombian imports, threatening to raise them to 50%. The dispute was resolved within days, with the tariffs paused and never fully enacted.

(Potential) Tariffs on Europe: Or lack thereof

Despite early threats from President Trump, the European Union has managed to avoid tariffs thus far. While the US considered imposing tariffs on EU goods, particularly targeting sectors like automobiles and steel, diplomatic negotiations have kept these measures at bay. However, the looming threat of tariffs continues to hang over future trade relations.

The UK Tariff free since… well last time

With Trump back in office, there is speculation that he may reintroduce tariffs on UK goods. During his last presidency, he imposed small tariffs on aluminium, Scotch whisky, cashmere, and some food products. However, the UK has avoided his latest tariffs, partly due to the balanced trade relationship between the two countries, with both reporting trade surpluses.

What does this mean for my portfolio?

No action can be taken at a portfolio level in response to Trump’s whack-a-mole approach to tariffs. At a fund level, we know from speaking to managers that they are doing their best to trade around what they expect to be sectors and/or geographies that will either benefit from or provide a layer of protection from the worst excess of Trump’s favoured method of bringing other counties to heel.

A Short comment on DeepSeek

We typically avoid commenting on individual stocks, but we felt this was worth addressing, given that NVIDIA now comprises 7% of the S&P and experienced a record $600 billion single-day loss due to DeepSeek.

Since then, things have somewhat calmed down, and retail investors continue to “buy the dip” en masse. However, this situation highlights how quickly market sentiment can shift and the risks of large, concentrated positions. It serves as a potent reminder of the importance of diversification in protecting portfolios from sudden and unexpected news flow. DeepSeek won’t be the last disruptor that the US tech giants will have to contend with, and the stakes are very high.

Performance & Positioning

So far this year, all IBOSS Core Portfolios have delivered above benchmark returns, ranging between 1.8% and 4.7% led by some exceptions returns from the underlying active managers. Our Passive Portfolios also produced positive returns for clients, however experienced slight underperformance in January, though they have largely tracked their respective benchmarks. In the case of all ranges, much of this performance was led by equities.

For details on the performance of our Decumulation and Sustainable ranges, please get in touch with a member of the IBOSS team.

Equity Markets: A Strong Start to the Year

Equities had a solid start to 2025, with the average IA Global Equity fund returning 4.95% in January. Despite ongoing macroeconomic uncertainty, markets delivered positive performance across a diverse range of regions.

Considering the ongoing economic and political turmoil I think it’s safe to say that few would have predicted Europe to emerge as the best performing market in January with a bumper return of 7.9%.

Both UK and U.S. equities also delivered strong returns of 4.5% and 4.7%, respectively and Emerging markets posted positive but more modest returns of 2.7%, lagging their developed market peers. A key drag on performance was India, which had a particularly challenging month despite its growing role in the global economy.

Fixed Income Markets: A positive if slower start

While fixed income assets have had a more muted start to the year, they have still made a positive contribution to overall returns. Corporate bonds were up 1.79%, Strategic Bonds increased by 1.63%, and UK Gilts rose by 1.59%. Surprisingly, the standout performer was Emerging Market Bonds, where the average fund in the sector delivered a return of 3.12%, outperforming its equity counterpart. This highlights how these assets can behave quite differently from traditional bonds and, in some cases, may even offer better capital protection as part of a diversified portfolio.

Although these returns may seem modest compared to equities, with cash yielding only 0.51% over the month, an allocation to fixed income assets has been positive for portfolios positions.

Looking forward

As in last month’s review, we remain optimistic about the long-term outlook for risk assets. However, with rapidly shifting political dynamics and some equity markets at all-time highs, we should anticipate continued—and at times sharp—bouts of volatility. As Harry Markowitz famously said, “Diversification is the only free lunch in investing,” a principle that feels more relevant now than ever.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 41.2.25