Diversification Strikes Back

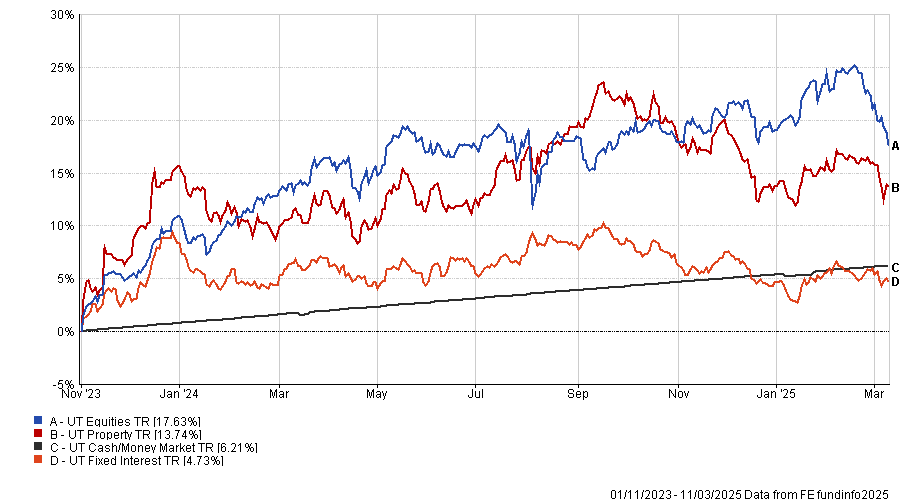

This update covers the period up to March 11th. As usual, we have taken the basic asset class chart (fig.1) back to the end of October 2023, the latest full Powell pivot, where he signalled victory over inflation and strongly suggested rate cuts were coming in 2024.

Macro & Markets

Asset Class Performance- 01/11/2023-11/03/2025

Diversification is Back

We’ve frequently emphasised the importance of diversification within portfolios. Not only does it help to mitigate downside risk, but it also opens up a broader range of growth opportunities.

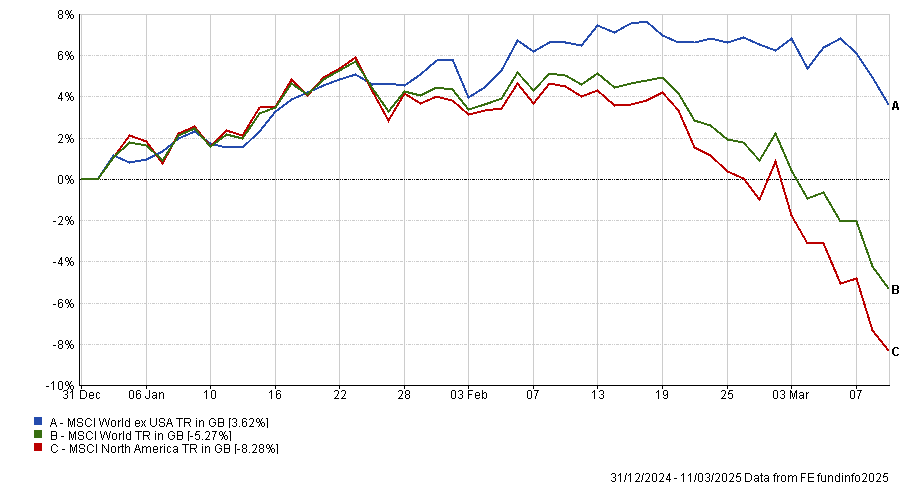

The chart below highlights a striking 11.9% performance gap between US equities and international equities year to date. This difference underscores how quickly market dynamics can shift and how concentration in a single market can work against investors as easily as it can benefit them.

We have highlighted previously that many investors have been drifting slowly and, in some cases, rather quickly towards a heavily concentrated position in US stocks, particularly the Mag 7. The pandemic led stimulus cheques for US investors saw US growth stocks surge as consumers put their free money to work. This herding was then exacerbated by the hype surrounding AI. However, since many buyers were narrative-sensitive rather than price-sensitive, it didn’t matter that valuations have moved to historically extreme levels.

Year to Date Performance – US Equities vs. Global Equities ex US – 31/12/2024-11/03/2025

US Equities: Year to Date performance -8.28%

The US equity market (MSCI North America) has faced a challenging year, declining 8.28%. A significant contributor to this downturn has been Trump’s Tariffs and the potential for ongoing trade wars. These Tariffs were initially suggested as unequivocally beneficial for the US economy but are now coming with a caveat. Namely, Americans should expect “some short-term pain” before the inevitable benefits materialise.

These tariffs have also prompted retaliatory actions from other nations, and the US now finds itself embroiled in a trade conflict of its own making on multiple fronts. Whilst the outcome is unknowable, the increase in uncertainty has left investors concerned about future growth prospects, specifically in the US.

Additionally, the outlook for AI-related stocks remains clouded, especially with the launch of DeepSeek. Whether or not DeepSeek “wins” is less important than the emergence of any potential new disruptor in the AI space. This could dramatically alter the investing landscape as we enter a quickly realised commoditisation of Al. The MSCI information Technology sector is down 13.7% year to date; however, this uncertainty weighs most heavily on some of the most expensive US stocks, markedly down from their highs.

| % below 52-Week high (11/03/2025) | |

| S&P 500 | -9% |

| Apple | -15% |

| Microsoft | -19% |

| -21% | |

| Amazon | -19% |

| NVIDIA | -29% |

| Tesla | -53% |

| Microstrategy | -52% |

Equities ex US: Year to date performance +3.62%

Diversification is back, and compared to the US, international equities have shown much more resilience, with a positive return of 6.1%. Within this World ex-US cohort, several regions have posted strong gains, providing a positive offset to the US market’s reality check. However, it’s not all countries that are benefiting from this new paradigm. India, having been a standout equity market for the past 5 years, has been slumping in recent months, and that has only gotten worse in light of the increased global trade tensions.

- UK Equities: +4.96%

- European Equities: +9.42%

- Chinese Equities: +14.34%

- Japanese Equities: -1.76%

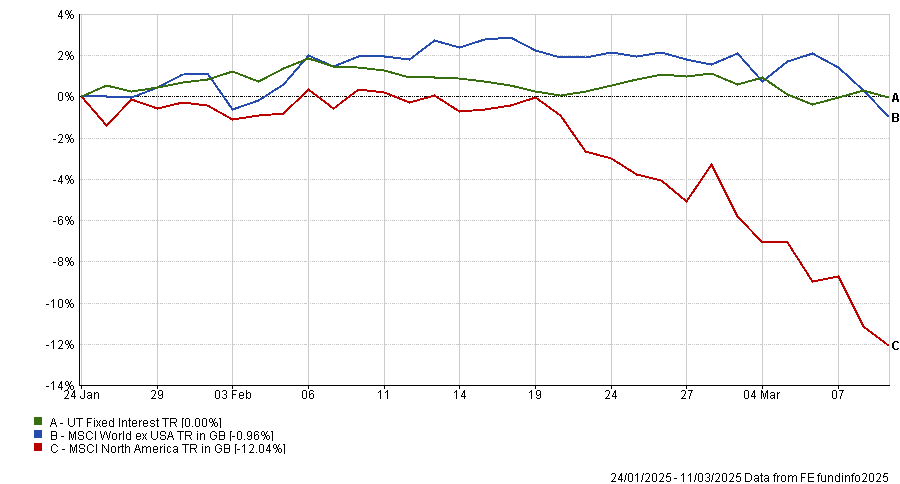

Fixed Income: Year to date performance +0.11%

The fixed income market has not sold off like some equity markets, and it has generally provided flat to positive returns this year. Importantly, many of these assets have performed well relative to other assets, protecting capital as US equity markets struggle.

Bond markets have performed particularly well relative to equities since DeepSeek burst onto the scene on the 26th of January. We strongly believe that many investors and commentators alike have underestimated the impact of DeepSeek on the valuations of many growth stocks, especially members of the Mag 7. The euphoria around AI was not just an idiosyncratic factor in elevating some tech valuations skyward; it was also driving market sentiment more broadly. There has now been a simultaneous collapse in sentiment and confidence in US tech stocks and a renewed enthusiasm for ex-US tech stocks.

Post DeepSeek Performance – Fixed Income vs. US Eqs vs. Global Eqs ex US – 24/01/2025 – 11/03/2025

Performance & Positioning

This year, all IBOSS Core and Decumulation Portfolios have outperformed their benchmarks, delivering 2% to 3% returns. As noted in last month’s update, much of this strong performance has been driven by the returns of our underlying active managers.

February’s market movements have been particularly challenging for some passive indices, especially those with a heavy weighting in US equities. However, all our Passive Portfolios have delivered positive returns for clients. While three portfolios have marginally underperformed their benchmarks, the majority have outperformed.

The IBOSS range has collectively made one of its strongest starts to a year since 2017. February was particularly strong, as markets rewarded a broader range of assets.

We had previously raised concerns about the increasingly concentrated assets held within many multi-asset portfolios. These participants have chased their US allocations higher on the basis of the American Exceptionalism narrative. However, America looks to be increasingly less exceptional. US companies are forced to deal with ongoing policy changes, and whilst they may present the world with a calm exterior for fear of being singled out, they are facing very uncertain market conditions. We therefore expect volatility to remain high for the foreseeable future.

While this may be unsettling for clients, it could also create valuable opportunities for investors with the flexibility to capitalise on market fluctuations. The problem was always going to be that America would hit a speed bump at some point, and the potential market fall would be outsized due to its starting valuations. We, as investors, must remember that America has some great companies, but there are many other opportunities in the investing world.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 67.3.25