The Road Ahead

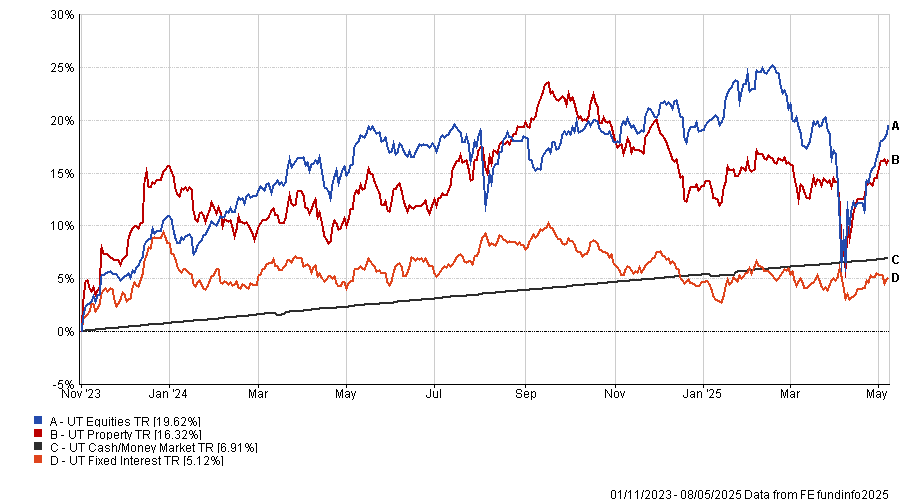

This update covers the period up to May 7th. As usual, we have taken the basic asset class chart (fig.1) back to the end of October 2023, the point of Powell’s latest full pivot, where he declared victory over inflation and strongly signalled that rate cuts were likely in 2024.

In recent days, there has been a noticeable shift in tone coming out of the White House, and more significantly, from Trump himself. Just last week, he remarked that American kids might “have two dolls instead of 30 dolls” a striking departure for someone who has consistently touted the success of his policies. Alongside other recent comments, he appears to be dropping broad hints that the path ahead may be tougher and more complex than his earlier campaign rhetoric suggested.

Macros & Markets

Basic Asset Class – 01/11/2024 – 08/05/2025

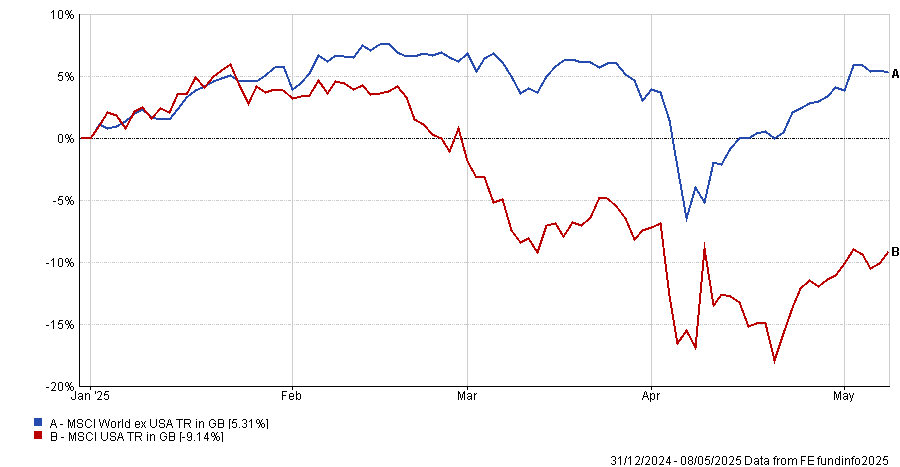

Trump- Making the World Ex-USA great again

It’s impossible to know exactly what Trump expected global equity markets to look like in 2025, but it’s safe to say they likely don’t resemble the current landscape. While US markets have recovered from the initial post-tariff announcement lows, so too have markets elsewhere (and many didn’t fall as sharply to begin with).

At present, market behaviour is fairly straightforward: every time there’s an exemption, rollback, pause, or extension on tariff measures, a market or sector rallies. Conversely, when tariff measures are raised or expanded, markets retreat. And with the Trump administration’s tariff policy shifting almost daily, market reactions have been similarly volatile. Autos and semiconductors, in particular, have been on a rollercoaster ride. Since April 2nd, 2025, some of the hardest jobs in commerce are held by those navigating US imports and exports. As America becomes more isolationist, other nations are being forced to look inward, forging new partnerships with more stable and dependable allies.

Year-to-date performance – USA against the rest of the world- 31/12/2024 – 08/05/2025

Is dollar weakness a sign of concern?

The US administration has told us to keep an eye on two things: the dollar and the 10-year Treasury yield. The dollar has certainly weakened, and the 10-year yield has essentially returned to where it stood when Trump was re-elected. However, it was the spike in bond yields that arguably forced the administration into granting the 90-day extension on tariff implementation.

We believe the key potential checks on Trump’s economic policy are the bond and equity markets, though the “put” level on equities — the point at which the administration steps in — may be lower than previously assumed. We would also add poor opinion polls and increasing calls from CEOs for changes to tariff and economic policy as additional pressure points. These four factors combined give markets multiple potential avenues through which some of the more extreme policies could be softened or even reversed.

US Dollar Index – 07/11/2024 – 07/05/2025

Source: Investing.com

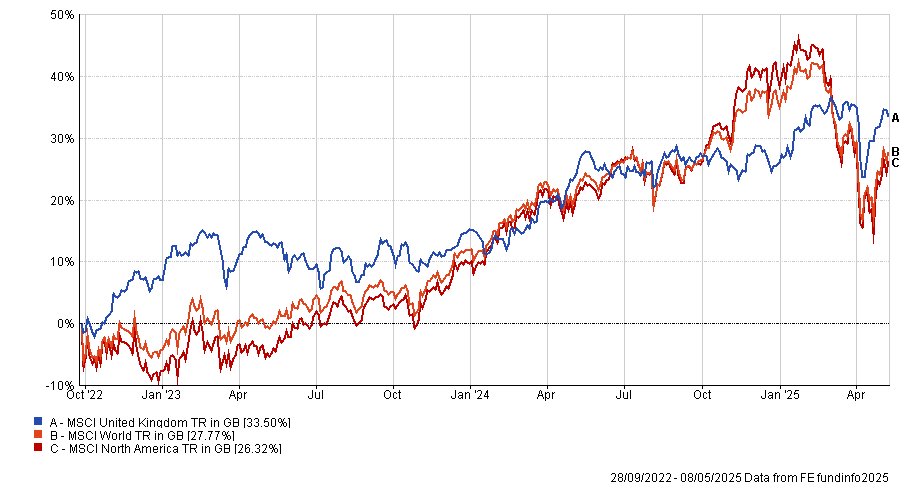

UK Equities – Be greedy only when others are fearful

Since the turmoil around the Truss budget and the collapse of the gilt market, UK equities have quietly regained their footing. Despite facing fresh challenges, including bumps from the first Reeves budget, the UK market has benefited from its attractive starting valuations. Over the past year in particular, UK equities have outperformed many of their global peers and have done so with notably less volatility. A welcome change from the post-Brexit era leading up to the Truss crisis.

UK Equity Performance from the Liz Truss budget – 28/09/2022 – 08/05/2025

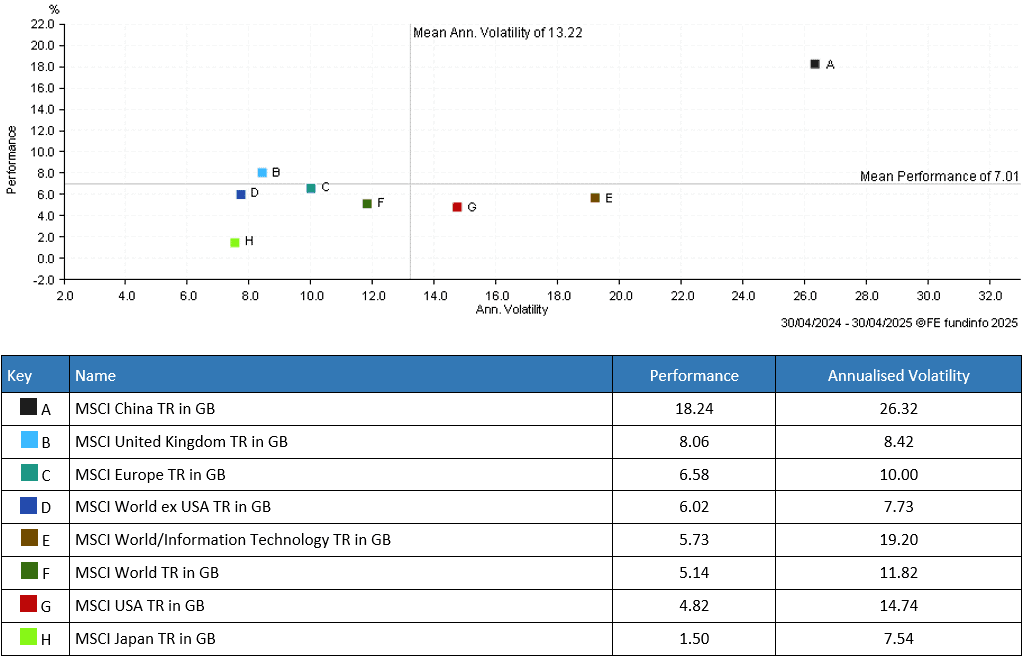

1 Year Scatter – Global Equities – 30/04/2024 – 30/04/2025

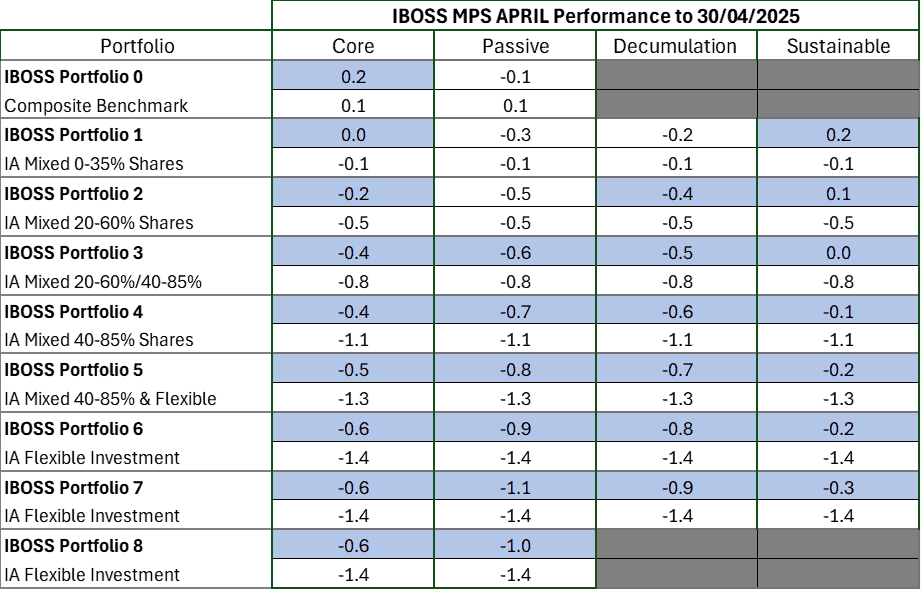

IBOSS Performance Review

In last month’s performance update, we included data up to April 1st, which did not capture the markets’ reaction to the Trump tariffs following Liberation Day. As a result, much of April’s performance was driven by the portfolio’s response to the uncertainty these tariffs introduced.

That said, the initial panic triggered by the tariffs was largely reversed. While benchmarks still delivered negative returns for the month, all Core and Sustainable portfolios outperformed their respective benchmarks, with most Decumulation and passive portfolios also showing similar outperformance.

This builds on the strong relative performance seen across the ranges since the start of the year. As the chart below highlights, the Core, Decumulation, and Sustainable ranges have all outperformed year-to-date. Notably, the lower-risk passive portfolios have faced relative challenges, as many active fixed income managers have delivered significant outperformance so far in 2025.

As with last month’s update, much of the positive performance can be traced back to the portfolios’ more diverse equity positions relative to benchmarks. This factor has had a more pronounced impact on the higher-risk portfolios with greater equity allocations.

Looking over longer periods, the picture continues to improve. All ranges are outperforming over one year, with Core Passive and Decumulation portfolios ahead over three years, and the majority of portfolios outperforming over five years and beyond.

We often highlight the benefits of diversification for long-term investors and the importance of keeping clients engaged through market cycles. We continue to believe this approach is vital, especially as market uncertainty is likely to remain elevated, and the leaders of the past may well differ from those of the future.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 124.5.25