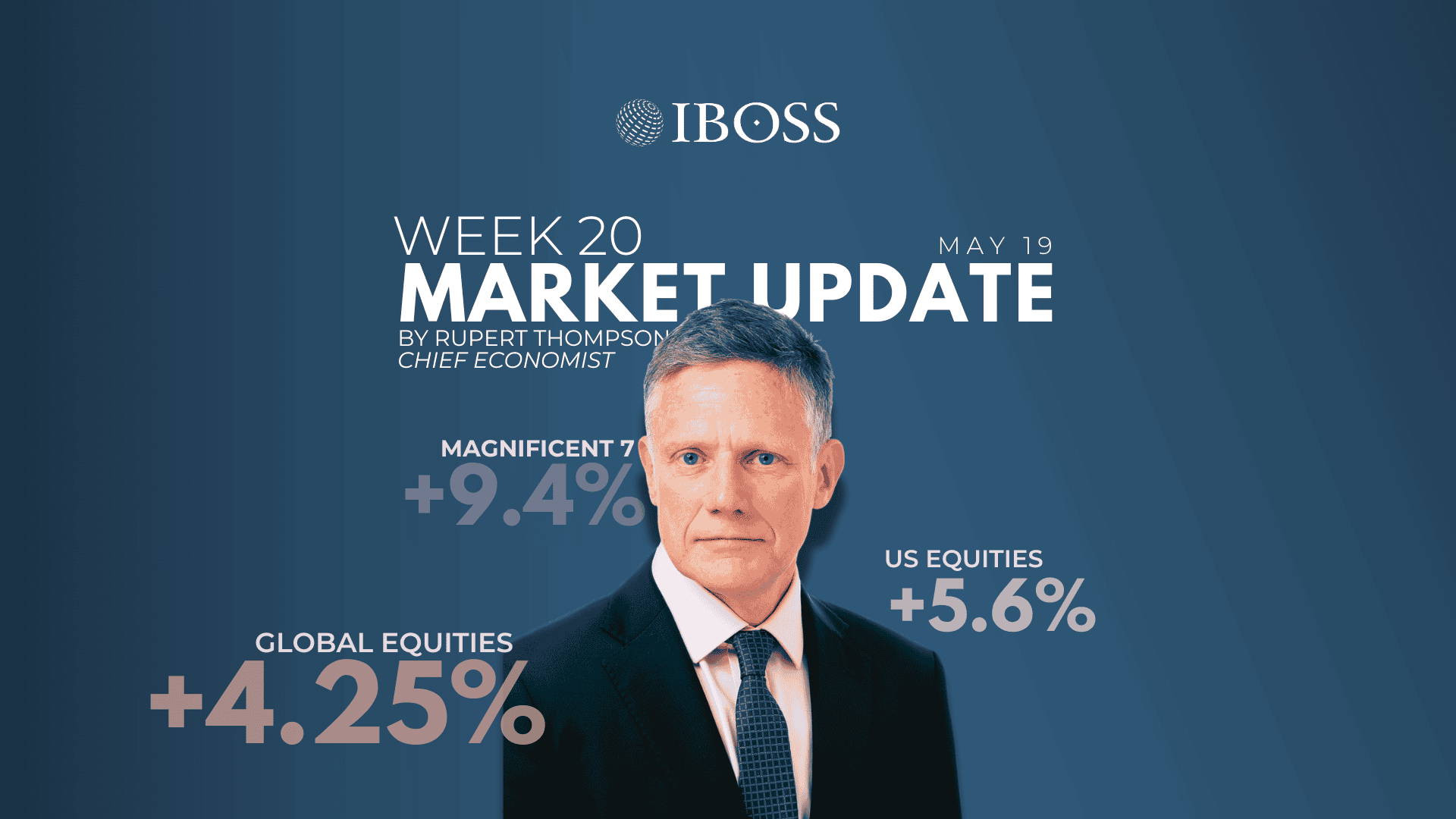

Equities posted strong gains last week with global markets up around 4¼% in both local currency and sterling terms. The prime driver was last Monday’s news that the US and China would for a 90-day period slash their tariffs on each other from 145% to 30% and 125% to 10% respectively.

US equities were the biggest beneficiary, gaining 5.6% in sterling terms versus a rise of 2.0% for the rest of the world. The US outperformance was in part driven by the Magnificent Seven which bounced as much as 9.5%.

These gains mean the US market is now up just under 20% from its April low and up slightly year-to-date. Even so, this still leaves the US trailing significantly other markets since the start of the year, with the gap magnified by the decline in the dollar. While the US has lost 3.9% in sterling terms, the rest of the world has returned 6.2%.

The size and speed of the rebound in equities highlights the perils of trying to take advantage of current market volatility, particularly when the moves are being driven very much by the unpredictable whims of just one person.

We expect markets to remain volatile over coming months with crucial tariff negotiations over this period. For the moment, however, investors seem to have donned their rose-tinted spectacles with valuations of the US but not other markets looking concerning again. The US price-earnings ratio is now back up to 23x, close to last year’s high.

Even though the economic outlook now seems considerably better than at the start of April, it remains significantly worse than at the start of the year. Most likely, we are still looking at the average US tariff ending up at around 15%, the highest level since the 1930s and up from 2.5% before.

This means higher inflation and weaker growth, even if the risk of an outright recession now seems much reduced. On which note, last week’s US inflation numbers proved a non-event. The core rate was unchanged at 2.8% in April while headline inflation edged down to 2.3%. US retail sales and consumer confidence, however, were rather weaker than expected with the latter falling further in May close to its all-time low in 2022.

Reduced worries of recession have unsurprisingly led to expectations of Fed easing being scaled back. The market now expects only two rate cuts later this year with the Fed holding off on any move until September. This in turn has led to US Treasury yields moving higher again in recent weeks, although they remain below their high at the turn of the year.

Budget deficit concerns may also keep US bond yields under some upward pressure. Trump’s ‘big, beautiful tax bill’ is wending its way through Congress and the tax cuts it contains – even though partially offset by spending reductions and tariff revenues – point to the US deficit remaining a worryingly high 7% of GDP or more for the foreseeable future.

Case in point, the credit rating agency Moody’s downgraded on Friday the rating of the US by one notch, moving into line with the other rating agencies. While the downgrade does not have any big implications, it does highlight the background concerns over the US fiscal situation which have the potential to unsettle markets down the road.

Here in the UK, there was some unreserved good economic news with GDP posting a larger than forecast 0.7% increase in the first quarter, up from 0.1% in the previous quarter. Rather than stalling following a good gain in February, as had been expected, activity continued its upward trajectory in March.

While UK growth looks set to slow again – the latest labour market data show payroll employment falling in the last three months – these numbers do show the damage done by the tax hikes in the Budget was less than feared. Moreover, today’s reset of trade relations with the EU may be limited in scope (as was the recent trade deal with the US) but these deals at the margin do provide a welcome boost to the UK’s longer term growth potential.

This coming week should see the less welcome news on Wednesday that UK inflation moved back up in April to 3.3% from 2.6%. Elsewhere, the main focus will be on the US, EU and UK business confidence numbers for May released on Thursday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 134.5.25