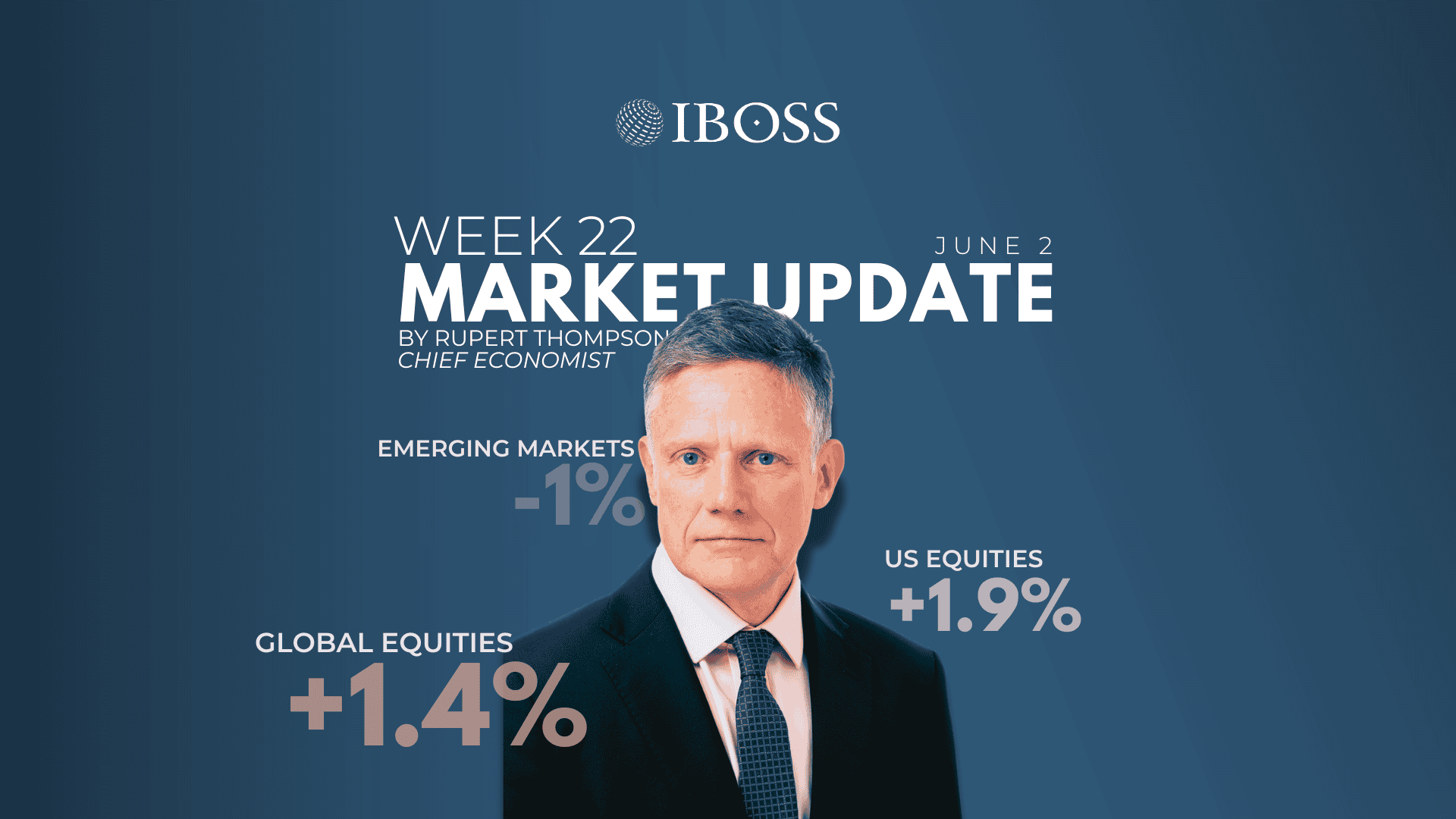

Equities gained 1.4% last week, reversing some of their decline the previous week and leaving them up 5.7% and 4.7% in local currency and sterling terms respectively over the month. US equities led last week’s increases with a rise of 1.9% while emerging markets lagged and were down 1.0%. UK equities gained 0.7% with small cap leading the way – the latter rose 2.3% to be up a strong 7.8% in May overall.

Just for a change, tariffs were centre stage and a source of volatility with the news changing literally by the day. The previous week had ended with Trump threatening to double the tariff on Europe starting on 1 June from 25% to 50%, only for him on Monday to delay the tariff hike until 9 July.

Then, we had an unexpected US court ruling that the majority of Trump’s tariffs were unlawful, only for the Administration to appeal and the order to be put on hold. The court has only ruled that the tariffs are not justifiable under the particular piece of legislation currently being used by the Administration.

If the ruling is upheld, it will certainly make it more complicated for Trump to impose tariffs. But it looks unlikely to prevent them as there are other more solid pieces of legislation which the Administration can draw upon if necessary.

The tariff drama didn’t stop there with Trump proceeding to up the ante with China, accusing it of violating the 90-day truce which allowed the removal the bulk of the massive tariffs both sides had put in place. To cap it all, Trump then announced a doubling in the tariff on steel and aluminium imports to 50% from 25%.

While these machinations did cause some wobbles, markets appear still solidly signed up to the so-called TACO trade (Trump Always Chickens Out) and the idea that the tariff levels ultimately imposed will not be high enough to do much damage. This acronym was even brought to Trump’s attention and he was not amused.

Although tariffs no longer look likely to cause a recession, a significant slowdown in growth is still on the cards and the market rebound is beginning to look a tad overdone, now equities have regained the bulk of their losses earlier in the year.

Equity markets, however, took heart last week from two additional pieces of news. First, one of the two main measures of US consumer confidence recovered in May a good part of its recent sharp decline. Second, Nvidia – the chip manufacturer and poster child of the Magnificent Seven – posted a set of stellar and better than expected results despite US restrictions on its sales to China.

Fixed income has also been in the news recently as a result of concern over the upward pressure on long-dated government bond yields. Worries have stemmed in part from Trump’s ‘big, beautiful tax bill’ which is now wending its way through the US Congress.

This will not only reinforce the upward trajectory of US government debt as a proportion of GDP over the coming decade but also currently contains a provision potentially allowing tax rates to be raised on foreign holders of US investments. The US Treasury Secretary even felt the need over the weekend to state that the US would never default on its debt.

Concerns are not just centred on the US. The UK’s public finances are also looking increasingly problematic, which will no doubt be highlighted when the Chancellor presents the conclusions of her government spending review on 11 June.

Japan has also become a source of some apprehension. The fear here is that the recent sharp rise in Japanese yields may lead to Japanese investors switching away from US Treasuries back to their home market, now domestic yields are looking rather more attractive.

Despite these background concerns, government bond yields in all three regions ended the week a little lower. 10-year yields in the US and UK are currently 4.4% and 4.7% respectively and remain some 0.2% or so below their highs at the start of the year.

We believe recent concerns are likely to continue and lead to further volatility in the capital value of bonds. However, with interest rates expected to decline further in the US and the UK over the coming year, this should prevent a sustained spike higher in yields. Indeed, we believe current yield levels look attractive, particularly with UK cash set to be returning less than 4% pa later this year.

This coming week, the US macro data will be a major focus, not only for the markets but also the Fed, with the May payroll numbers released on Friday. Elsewhere, the ECB looks very likely to lower rates to 2.00% from 2.25% on Thursday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 149.6.25