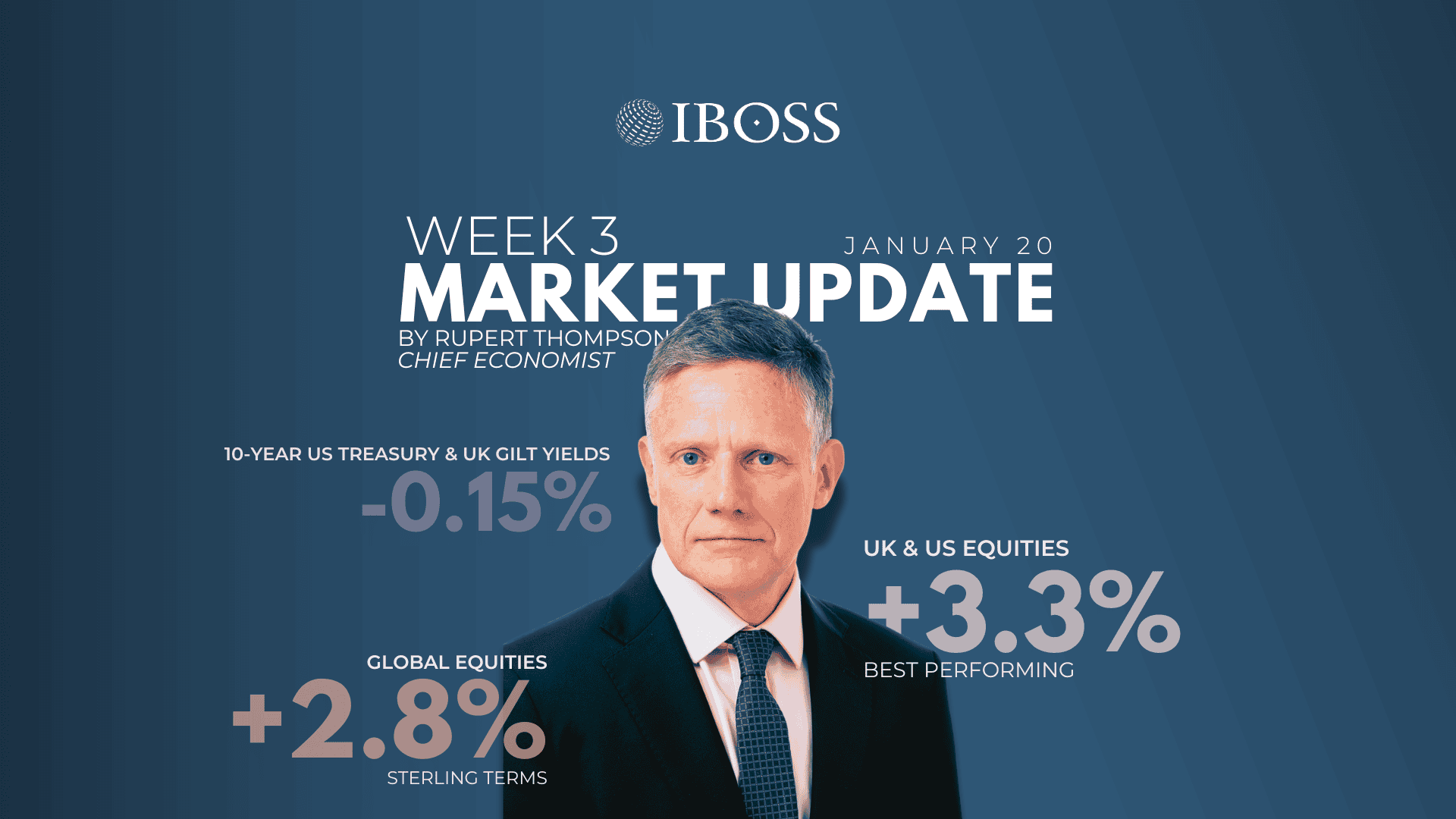

Global equities performed well last week, gaining around 2.4% and 2.8% in local currency and sterling terms respectively. This left markets up 1.8% year-to-date in local currency terms and a rather larger 4.3% in sterling terms as a result of a 2% fall in the pound. The UK and US led last week’s rise with increases of around 3.3% in sterling terms.

Bonds also had a good week. 10-year US Treasury and UK gilt yields both declined around 0.15%, reversing much of their recent rise and leaving yields only slightly up on the end of last year. Treasuries and gilts duly returned 1.6% and 0.9% over the week, leaving them broadly flat on the year so far. To mix my metaphors, this decline in yields confirms that the recent sell-off in gilts was more a storm in a teacup than another Liz Truss moment.

It would be nice to think the market gains last week were down to a ceasefire in Gaza finally being agreed but the reality was rather more prosaic – better than expected US inflation numbers and a strong start to the fourth quarter US earnings season.

The core US inflation rate unexpectedly edged down in December to 3.2% from 3.3%. This was enough to soothe the inflation angst of recent weeks and allow markets to regain some hope that the Fed will be able to lower rates another 0.5% or so over the coming year, even if the next cut has to wait until the summer.

Meanwhile, the big US banks kicked off the reporting season with a bumper set of results, on the back of buoyant trading and investment banking revenues, and the sector was up as much as 7% over the week. The good news this quarter should not be confined to the banks, with overall earnings of the S&P 500 forecast to be up 11% on a year earlier, up from 9% in the previous quarter. If earnings beat expectations, as conveniently they almost always do, this will mark the largest rise for three years.

The UK also saw some good news last week, at least on the inflation front. Headline inflation edged lower to 2.5% in December and the more important core rate fell more than expected to 3.2% from 3.5%, with services inflation slowing significantly from 5.0% to 4.4%. However, a good part of this decline was down to a 20% fall over the month in airfares which tend to be erratic at this time of year.

Unfortunately, the inflation news over coming months is unlikely to make such pleasant reading with both core and headline rates set to head higher again. Still, this should not prevent the Bank of England from lowering rates by a further 0.25% in Feburary to 4.5%, particularly after last week’s downbeat data on activity.

Although UK GDP did edge up 0.1% in November, reversing its October fall, the bigger picture is that the economy has flatlined since the summer. We still expect growth to pick up again but this will require a rather cheerier consumer and there was little evidence of this in December which saw an unexpected fall in retail sales.

Even so, there is rather more cheer at the moment in the UK than Germany which remains very much the sick man of Europe – not that we’re included in that category any longer. German GDP contracted 0.2% in 2024, the second consecutive annual decline. The UK, by contrast, should manage a gain of 0.8% last year, which looks quite respectable as long as we don’t cast our gaze across the Atlantic where US growth should be around 2.8%.

If the official numbers are to be believed – the only problem being that most people don’t – China is the place to go if one’s looking for growth. Friday saw the reporting of a surprise rise in growth in the fourth quarter to 5.4% from 4.6%. This coincidentally just happened to leave the gain for the year as a whole at 5%, bang in line with the government’s target.

All the anecdotal evidence is that Chinese activity is considerably more depressed than these rather rosy numbers suggest. With Trump’s plans to hike tariffs set to impose an additional drag on the economy, it makes it all the more necessary and likely that the Chinese authorities will follow through on their pledges to boost their support for the consumer.

This coming week, President Trump’s inauguration speech later today will be the big focus as investors will desperately search for clues as to which of his many pronouncements he is actually likely to implement. Other than that, Tuesday sees the release of UK labour market data and on Friday we have business confidence numbers for the US, UK and Europe as well as a Bank of Japan meeting which could see rates raised for the first time since July.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 21.1.25