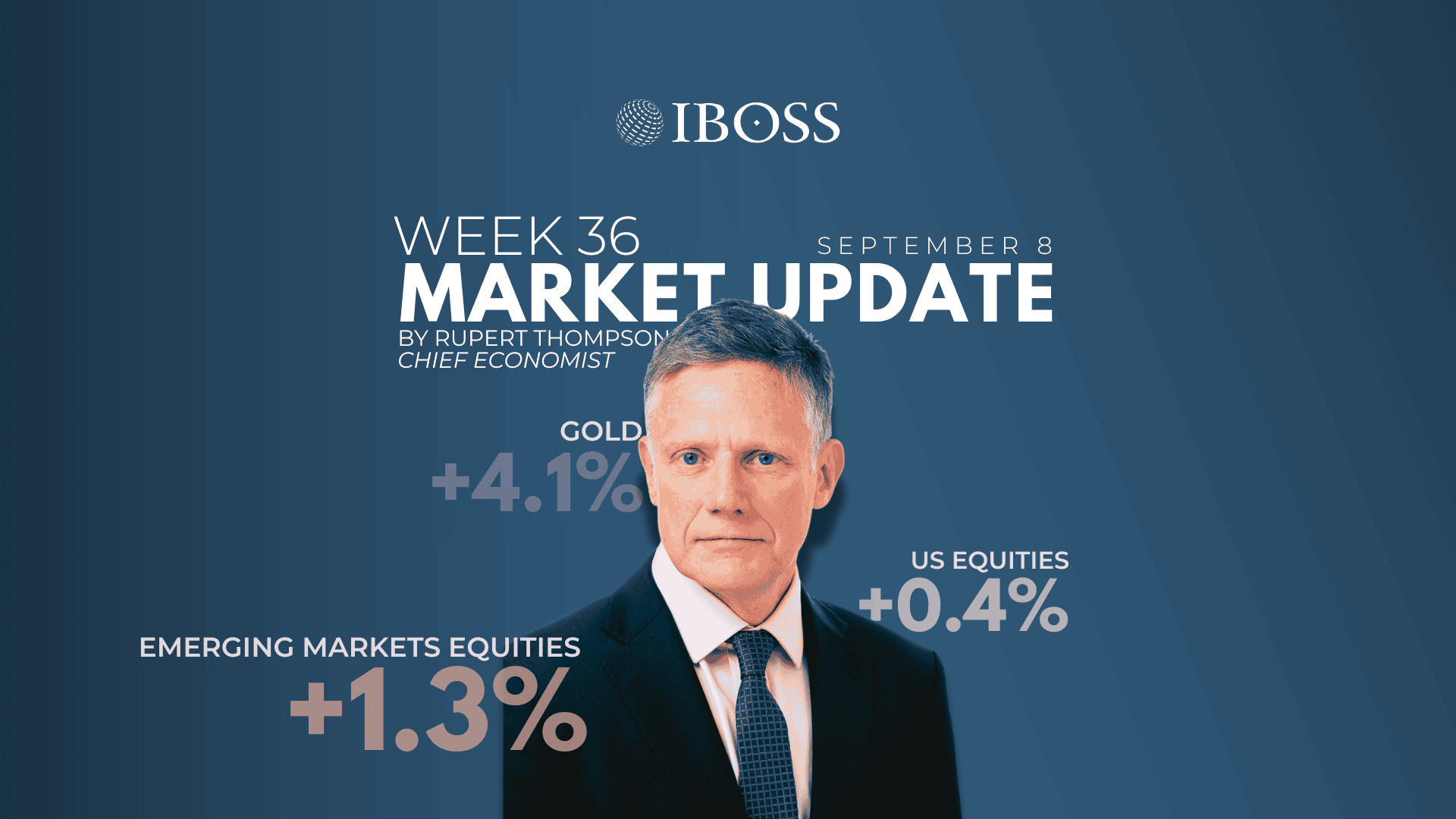

Equity markets had another quiet week, edging up 0.4% in both local currency and sterling terms. Emerging markets led the gain with a rise of 1.3% while the US rose 0.4% and the UK 0.2%.

It seems strange to mention individual stocks almost in the same breath as countries and regions. But with Nvidia at its August peak accounting for as much as 5.1% of total global market capitalisation, trumping the 3.5% of the UK, this is the world we now live in.

Anyway, last week highlighted the growing divergence in performance within the Magnificent Seven. Nvidia fell back a further 4% and is now down 8% from its high. Alphabet, by contrast, was up 10% on the back of a US court ruling that it would not be required to sell off Google’s Chrome browser as had been feared.

Meanwhile, bonds had a good week with UK gilts and US Treasuries returning 0.7% and 0.9% respectively. However, gold once again stole the limelight, jumping 4.1% and breaking above $3600/oz this morning – leaving the USD price up as much as 38% since the start of the year.

The big event for the markets was the US payroll numbers on Friday, which came in lower than expected. Employment increased a mere 22,000 in August, confirming a marked weakening in the labour market. By way of comparison, employment growth had been averaging around 150,000 a month until the spring but in the last three months has averaged a mere 29,000.

The US unemployment rate is rising as a result, although only slowly, edging up to 4.3% last month. It remains subdued in large part because Trump’s crackdown on immigration means the labour force is now barely growing.

These numbers left an interest rate cut at the Fed’s next meeting on 17 September looking all but a done deal, barring a big shock from this week’s inflation numbers. Indeed, the market now sees a faint chance that the Fed could cut rates by as much as 0.5% – as it did last September – rather than by just 0.25%. Either way, rates are now seen falling from their current 4.25-4.5% to 3.6% by year-end and to as low as 3.0% by next summer.

Despite all the angst whipped up by the media over the pressure on the bond markets from fiscal worries, both here and in the US, there has been no sustained upward pressure on yields this year – other than for UK bonds with maturities as long as 30 years. Instead, the direction of interest rates remains the main driving force behind bond yields. US 10-year Treasury yields have fallen significantly since the spring and last week fell a further 0.13% to 4.07%.

10-year UK gilt yields also edged lower to 4.66%, dragged down by the gravitational pull from Treasuries and are currently bang in the middle of this year’s 4.5-4.9% trading range. 30-year yields have climbed a bit higher this year to 5.5% but this seems mostly to do with the secular fall in pension fund demand for such long-dated bonds – courtesy of the ending of most private sector defined benefit schemes and the Lizz Truss debacle.

Gold liked the payroll numbers even more than bonds did. Increased hopes for lower rates are generally good news given gold pays no yield and is at less of a disadvantage in this respect if bond yields and interest rates are falling. The effect is being reinforced this time by worries that Trump’s attempts to pack the Fed with his appointees may increase inflation risks down the road.

But the biggest factor behind the surge in gold over the last couple of years has been heavy buying by central banks as they seek to diversify their holdings away from the dollar which has rather lost its appeal under the current US Administration. Global central banks in fact now hold more gold than US Treasuries and August saw the Chinese central bank increase its holdings further.

We’ve got so far without mentioning the curious incident of an underpayment of stamp duty on a flat in Hove despite the ructions and reshuffle of the Cabinet deck chairs it caused. This is because it had precisely zero obvious impact on the UK markets. The pound was virtually unchanged over the week and UK equites and bonds just followed the lead of other markets.

However, we did finally get a date for the diary. The Budget will be on 26 November, leaving us with the delightful prospect of another full three months of kite-flying and rumour mongering. Rather surprisingly and encouragingly, given the already intense focus on the need for further substantive tax rises, business confidence recovered further in August, hitting its highest level for twelve months.

The market’s indifference to the UK’s political manoeuverings may in part reflect that the UK will shortly be joined by France and now Japan in such machinations. The French government looks certain to lose its confidence vote this afternoon, no doubt leading to weeks if not months of desperate scurrying around by President Macron to try and form another barely credible government.

As for Japan, its Prime Minister resigned over the weekend, reaping the consequences of the ruling LDP failing in the elections over the past year to gain a majority in either the lower or upper houses of parliament.

This coming week, Thursday’s US inflation data will be the highlight. The ECB meeting on the same day should be rather less noteworthy with rates looking certain to be left unchanged. UK GDP data for July is out on Friday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 265.9.25