This update covers the period year-to-date up to 13 November 2025 and continues to be a strong one for the IBOSS Core range, in both absolute and relative terms. Diversification, which has long been the favourite word in the IBOSS lexicon, is now trotted out by an increasing number of other managers on a daily basis. However, we still see many peers reluctant to give up on long-held positions that served them so well up until the second coming of Donald Trump.

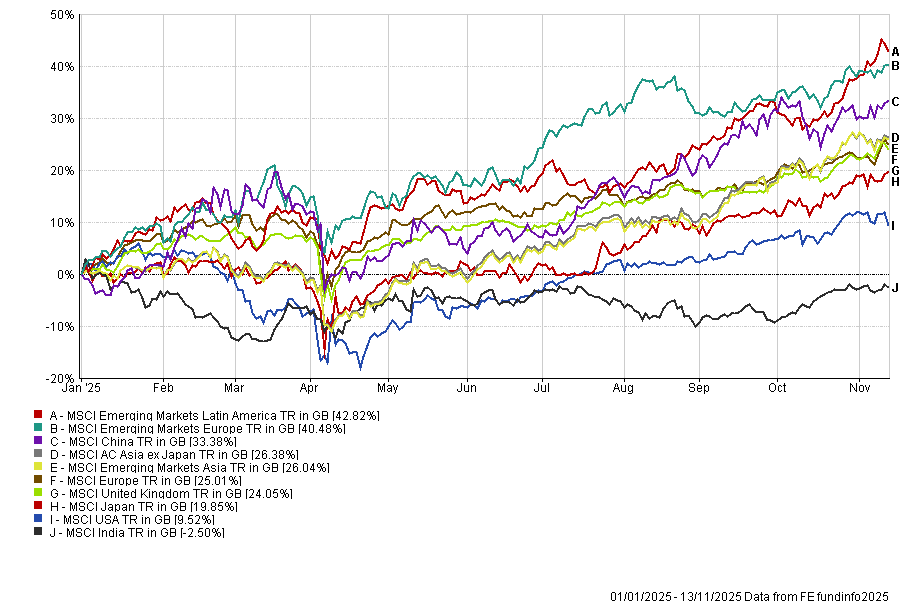

As the chart below (Fig.1) shows, despite near-blanket media coverage around US stocks, the US and India continue to be the global laggards in 2025. Coming into the year, they were also the two most expensive markets.

MSCI Selected Country Indices > 13/11/2025 (Fig.1)

Macro & Markets

In the US, we have just had the first elections of the Trump 2.0 period. We would not ordinarily care about elections such as the New York City mayoral race nor the election of a new Virginia governor, but in this unprecedented era they do give us some early feedback on how Trumpian economics are landing in the real world.

In short, the Trump administration had little to cheer about in the recent, albeit small-scale, elections. Democrats are now battering Republicans with the same issues they themselves were hammered for in the last presidential election, i.e. inflation, affordable housing and the overall cost of living.

This matters because it is already changing the language around tariffs, and attention has already turned to the midterms.

What’s Changed?

The second Trump administration came out all guns blazing just over a year ago with threats, tariffs and dressing-downs for friends and foes alike. It is early days, but we may see a similar dialling down of the rhetoric and even policy that we have witnessed on the international stage, this time on the US domestic front.

Trump has not delivered on his pledge to end the war in Ukraine, and he has learnt that, amongst other things, rare earths clearly show that China is not as weak and vulnerable as his team had previously indicated. Indeed, the tech race with China does not show the US pulling away, but rather the Chinese potentially closing the gap on multiple fronts such as AI and robotics, and leading in areas such as renewables, battery technology and drones.

Toned Down

There has been a noticeable toning-down of rhetoric emanating from the White House in recent weeks. We have also had less obvious pressure on the Fed, as the lack of US government data has made it harder to justify calling for rate cuts.

Trump is now floating ideas squarely based on changing the mood music on both the economy and affordability issues, and we expect a more conciliatory tone, and rather ironic pleas for patience, to persist. If the data do not fall into line, however, it is anybody’s guess what tactics the administration will employ to try and wrestle back the narrative and everybody and every country will need to consider themselves fair game.

Positioning and Outlook

The portfolio changes that came into effect from 1 November were to reduce smaller-company exposure in the US and increase exposure to large caps, broaden out European equity exposure, and increase active management in Asia. There were small increases to cash and a reduction of risk in the UK.

There remain, as ever, considerable opportunities in global assets across the world, but increasingly being more stock/bond-selective is paying off.

Price Matters

What you pay for an asset really does matter, but there can be very long periods where it is hard to see exactly why the price paid is so important. In the era of narratives, often built on short-term self-interest and the cult of personalities, it can take a frustratingly long time for the genuine investment case for anything to play out.

Aphorisms and proverbs become what they are because enough people subscribe to what they say, but Schopenhauer best sums up the perennial challenge: “All truth passes through three stages. First, it is ridiculed. Second, it is violently opposed. Third, it is accepted as being self-evident.”

This can be applied to many aspects of life, but it certainly captures narratives in the investing world. In the 1980s you had to be “all in” on Japan; post-GFC, you had to be “all in” on the US, and to question the longevity of such a stance would attract exactly what Schopenhauer stated. Sectorally, in the late 1990s we had the dot-com mania; from 2022 we continue to live through AI euphoria, it seems like there is always something going parabolic.

This Time Is Definitely Different!

Maybe a final word on the late-1990s period, because it’s often said that pets.com is not the same as Nvidia, and that is obviously true after all, Jensen Huang has yet to enter the cutthroat world of worming pills. However, a much more prescient comparison might be the fibre-optic mania starring companies like Global Crossing and WorldCom.

In summary, they built up massive amounts of inventory that never paid off to the extent they convinced themselves, and many around them, it would do. So, is the eye-watering capex by the “Mag 7” and others, including governments, justified? History suggests it isn’t. And if the investment case turns out to be wrongly calibrated and the price you paid for the assets was also wrong, then the potential for losses is considerable in some areas. Its not to say that tech and AI related themes should be avoided but we are perhaps highlighting a more ‘buyer-beware’ approach

The answer is to be price-aware, well diversified, and to understand how the investing world is shaping up now, not how it was from the GFC (2008) until November 2024.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 357.12.25