You’re probably fed up hearing about Donald Trump, his policy changes, and the constant tariff talk. Unfortunately, these factors shift so frequently that we can’t afford to ignore them, and whether we like it or not, they can have real implications for investor sentiment and asset prices. What may be a little surprising is how fast ‘tariff fatigue’ has set in, but if there is one thing Trump doesn’t like, it’s being ignored, so surely he will actually start doing things soon as opposed to firing off threats and social meida posts?

Tariff ‘Victims’- The diminishing returns of Trump’s words on markets

Select Global Equity Performance: 05/11/2024 – 25/11/2024

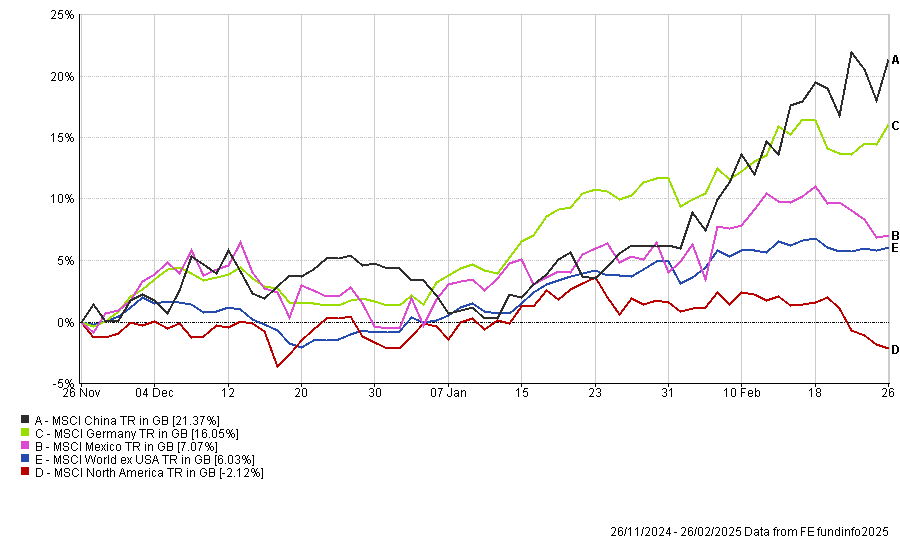

Select Global Equity Performance: 26/11/2024 – 26/02/2025

Market Sentiment Under Trump 2.0

Since Trump returned to the White House, his policy decisions have again dominated market discussions, and almost all markets have to be seen through a Trumpian lens. His focus on stock market performance, deregulation, and tax cuts certainly provides opportunities. At the same time, radically overhauling the immigration policies (or lack thereof), which has often benefitted the US economy in many sectors, is causing companies to question their spending plans. Threatening global supply chains that directly or indirectly affect the US companies he professes to be helping is a further cause for concern, especially for smaller US companies. We have already witnessed some serious underperformance by many medium- and small-sized companies.

Trump has always been vocal about his belief that the stock market is a measure of his success. If the markets aren’t reacting favourably, he’s willing to say or do things that will potentially help short-term market gains but potentially at the expense of longer-term ones. Unlike many global leaders, he sees stock market performance as an extension of his power. An early victim of his ire could be the Chair of the Federal Reserve. Not for sixty years, and the epic fallout of President Lyndon B Johnson and then Fed Chairman, William McChesney Martin Jn, have we had the backdrop for a clash of this magnitude. Trump will want interest rates cut whatever the economy is doing, and Powell has said he will only cut if inflation is sufficiently tamed; the evidence so far isn’t; something has to give.

Global Politics and a Weakening US Economy

The headlines have also been dominated by geopolitical tensions between the US and Europe, particularly concerning Ukraine. Trump has so far sided with Putin about what and who caused the war. Branding Zelensky, a dictator whom most people consider not to be, and not calling Putin a dictator whom most people consider to be one was a shock to many, but it’s very much on trend for Trump’s view of the world. However, beyond the political posturing around global conflicts, recent economic data suggests that the US economy may not be in as rude health as some believed. Instead, fresh concerns have emerged that growth could be slowing.

A string of disappointing data releases has sparked these fears, including larger-than-expected declines in housing starts and retail sales in January, and sharp drops in business and consumer confidence throughout February. The market reaction has been swift, with US equities showing uncharacteristic signs of weakness. Adding to the unease, Elon Musk once again made headlines by issuing an ultimatum to government employees via his Department of Government Efficiency (DOGE), putting a million jobs at risk. Even if he doesn’t follow through, he has created unprecedented uncertainty, which will endure whilst ever he is in charge of the DOGE. As we have seen with the Tesla share price and the collapse of sales in Europe, actions and words can sometimes have unintended consequences that are hard to undo.

Trump’s Tariff Policy: A Mixed Bag for Markets

Trump’s tariff approach has been aggressive and dynamic, impacting multiple economies. His initial imposition of a 25% tariff on Canadian and Mexican imports, citing immigration and drug trafficking concerns, was paused for 30 days following negotiations. Meanwhile, the US-China trade war reignited with a 10% tariff on Chinese goods, prompting retaliatory tariffs from China on American crude oil, automobiles, and rare earth metals.

One of the most short-lived tariff battles in history came from Colombia, where Trump imposed a 25% tariff after the country refused to accept deported migrants on US military planes. This was swiftly resolved, with tariffs suspended before they took effect. Interestingly, the UK has escaped Trump’s latest tariff plans, maintaining a trade-friendly relationship with the US despite previous minor tariffs on goods like Scotch whisky and aluminium. While the UK appears to have dodged tariff threats, European economies are now in the crosshairs, and negotiations remain tense. The possibility of future levies has added another layer of uncertainty. As a result, we may see shifts in foreign investment, particularly from US companies reassessing their European exposure. Trump doesn’t like supranational organisations, and his latest tirade cited the “EU was formed to screw the United States”. Contrast this with former President Obama’s infamous “Britain would go to the back of the queue” 2016 speech as the British went to the polls on leaving the European Union.

IBOSS’ US Allocation: A Strategic Shift, Not an Overweight Position

We made a conscious decision to increase our exposure to US equities slightly. However, it’s important to clarify that, historically, we have been underweight relative to many of our peers. The changes we’ve made do not mean we’re now overweight the US—it means we are less underweight.

The rationale behind increasing US exposure is simple: despite Trump’s unpredictability, his policies have the potential to benefit certain segments of the market. Small and mid-cap US companies, in particular, could gain from his deregulatory push in the long run. Unlike the retail investors focused on the ‘Magnificent Seven’, we see at least as much value in the other 493 companies in the S&P 500 that don’t grab headlines but present good opportunities.

We’ve taken a multi-faceted approach to achieve this, maintaining our positions in active funds like M&G North American Value and Federated Hermes US Smid Equity while adding to passive allocations such as the L&G US Index Trust (an S&P 500 proxy). Like many global trackers, the L&G International Index Trust also provides significant US exposure. We’ve also maintained our holding in the Rathbone Global Opportunities fund, which offers exposure to US equities but with careful stock selection, ensuring no overconcentration in hyped stocks like Nvidia.

Diversification Remains Key

While we acknowledge the potential opportunities in US markets, our portfolios remain well-diversified. Trump’s policy shifts can be abrupt, and while this can create rapid market upside, it can also bring sharp downturns. A prime example was the recent tech correction, which saw AI-linked stocks experience a sharp sell-off. Our diversified approach meant that IBOSS portfolios were well insulated, balancing exposure to high-growth areas with more defensive holdings.

As I’ve often said, trees don’t grow to the sky, and we must be prepared for corrections in overextended market areas. Our job is to look after longer-term client returns, which our track record demonstrates. To do this, we will inevitably experience periods of relative underperformance as some investors and markets pile into momentum play sectors and geographies. If investing were as simple as buying more of whatever has worked in the recent past, then there would be no need for portfolio managers. People hold on to narratives that they feel they can understand, such as ‘China is uninvestable’ or ‘American exceptionalism.’ However, they are sweeping generalisations and fail to acknowledge the dynamism of global markets. Anchoring is a key risk to investor returns; like all behaviours, its outcome requires regular re-evaluation.

The Outlook: A Dynamic but Uncertain Future

If history is any guide, we should expect rapid shifts in Trump’s policy direction, particularly in response to market movements. His approach to trade deals, tariffs, and regulation will remain a significant driver of volatility but an opportunity for active investors willing to adapt, even using passive vehicles to express their views. This dynamic approach is the one adopted for our Passive MPS range.

We remain committed to a balanced investment strategy that captures opportunities while mitigating risks. The key takeaway for financial advisers and planners is that while Trump’s economic policies may inject unprecedented uncertainty into markets, diversification remains ‘the only free lunch in investing’.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 57.2.25