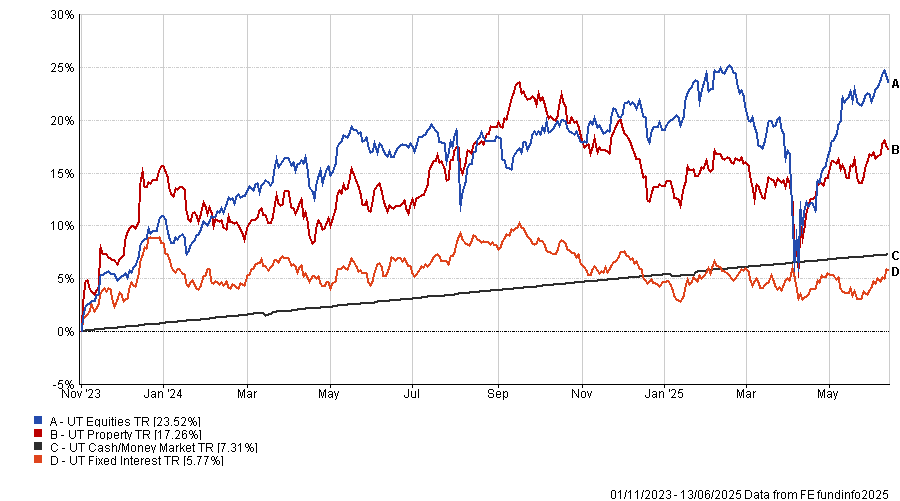

This update covers the period up to June 17th. As usual, we have taken the basic asset class chart (fig.1) back to the end of October 2023, the point of Powell’s latest full pivot, where he declared victory over inflation and strongly signalled that rate cuts were likely in 2024.

Macro & Markets

Markets delivered markedly positive returns in May, even as volatility remained elevated due to ongoing trade and tariff negotiations. The idea that “Trump Always Chickens Out” (dubbed the TACO trade) gained traction among investors, many of whom appeared increasingly ambivalent toward the barrage of tariff-related headlines.

While this relief rally was certainly welcome, particularly considering the global equity market is now up 14% since their lows in March) we remain cautious. Tariffs are still elevated by historical standards, even after recent rollbacks. Although we’ve seen a series of pauses, delays, and recalibrations in trade policy, the broader implications for markets and the global economy remain uncertain.

The US Leads the Charge in April

Unlike prior months the U.S. equity market led the way in April, driven largely by a rebound in several of the Magnificent 7 names that had previously faced pressure. However, this was far from a one-sided rally and global equities also performed strongly, with the average ex U.S. stock rising around 4%, compared to a 5% gain for U.S. equities.

While this is clearly short-term data, it underscores a key point: underestimating the U.S. in the near term can be just as risky as overcommitting to it. We expect continued volatility, but as the chart below illustrates, the U.S. still has meaningful ground to cover to reverse its recent underperformance relative to a broader basket of global equities.

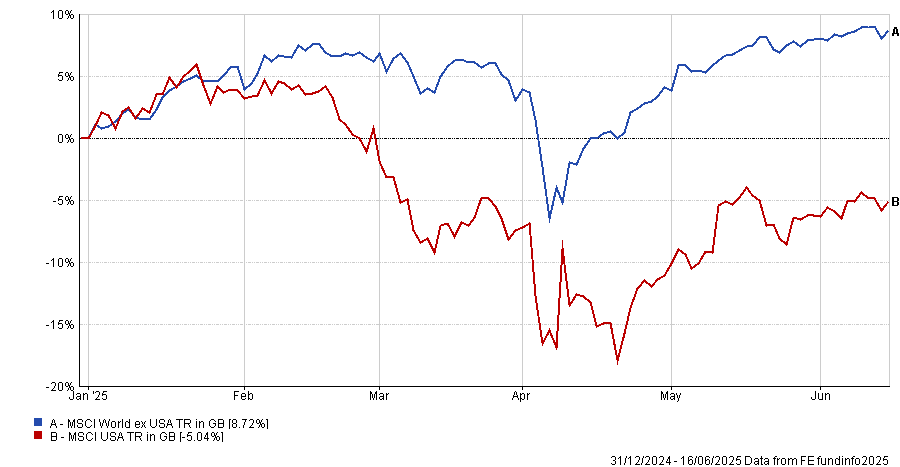

Year to Date Performance – US and Rest of World

Bond Markets Steady but Not Without Friction

April was a quieter month for bond markets compared to equities. U.S. Treasury yields drifted higher amid ongoing supply and softer auction demand. In Japan, JGBs faced similar headwinds with weaker demand at several auctions, while UK Gilts experienced challenges that led to a focus on shorter-dated auctions.

On a positive note, active bond managers continued to outperform passive strategies, and allocations to corporate and emerging market bonds contributed positively to overall returns.

We’ve previously noted that the higher interest rate environment is generally more favourable for bond investments than the low-rate conditions before 2022. That said, like equities, we expect ongoing volatility and wouldn’t rule out a “Liz Truss” style shock in other bond markets. In any case this can be a good opportunity for actively managed investments.

The Dollar Story

This is the third time we’ve mentioned the dollar in our monthly update. While the situation remains largely unchanged, the recent moves in currency continue to be important. The U.S. administration has highlighted two key indicators to watch: the dollar and the 10-year Treasury yield.

We’ve already covered Treasuries, but the dollar has continued to weaken and is down 11% from its January peak and slipping another 1% in April. Without repeating ourselves, it’s worth noting that the MSCI USA index is up 3% in dollar terms this year, but down 5% in sterling terms, underscoring just how much currency fluctuations can impact client returns.

IBOSS Performance Review

Much of the performance update this month remains similar to that of last month from a relative performance perspective with the majority of the IBOSS portfolios continuing to deliver strong returns in 2025 compared to their respective benchmarks. However, whilst April was marginally negative for the main asset classes May saw positive returns for risk assets including equities and property.

As mentioned previously the US lead the charge from an equity perspective, however, there remains a large dispersion of returns between the best and worst performing funds this year – and markedly positive fund selection has meant that the majority of core portfolios outperformed over the month.

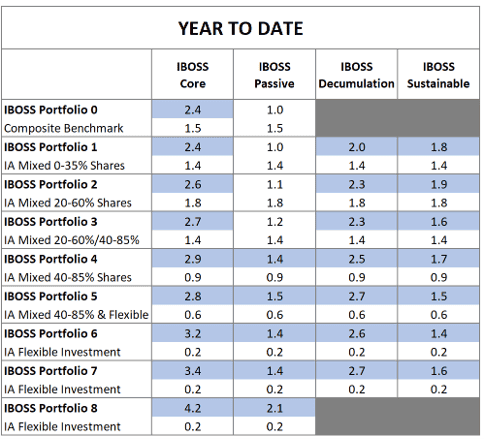

This builds on the strong relative performance seen across the ranges since the start of the year and now leaves all IBOSS portfolios positive for 2025 As the chart below highlights, the Core, Decumulation, and Sustainable ranges have all outperformed year-to-date. Notably, the lower-risk passive portfolios have faced relative challenges, as many active fixed income managers have delivered significant outperformance so far in 2025.

Year to Date Performance to 31/05/025

As with last month’s update, much of the positive performance can be traced back to the portfolios’ more diverse equity positions relative to benchmarks. This factor has had a more pronounced impact on the higher-risk portfolios with greater equity allocations.

Looking over longer periods, the picture continues to improve with Core, Passive and Decumulation portfolios ahead over three years, and the majority of portfolios outperforming over five years and beyond.

We often highlight the benefits of diversification for long-term investors and the importance of keeping clients engaged through market cycles. We continue to believe this approach is vital, especially as market uncertainty is likely to remain elevated, and the leaders of the past may well differ from those of the future.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 172.6.25