Markets last week were yet again held hostage by events in the Middle East, particularly the stream of conflicting pronouncements emanating from the White House on an almost daily basis. The week started with Trump extending his 48-hour deadline to reopen the Strait of Hormuz by 5 days until Friday, only for him to extend it on Thursday by an additional 10 days to Easter Monday.

The picture was confused further by the conflicting stories surrounding the negotiations supposedly underway to end the war. Iran at one point denied the talks flagged up by the US had even taken place. In reality, both sides as yet seem far away from reaching a compromise with the 15-point ceasefire plan put forward by the US as uncompromising in its demands as Iran’s own proposal.

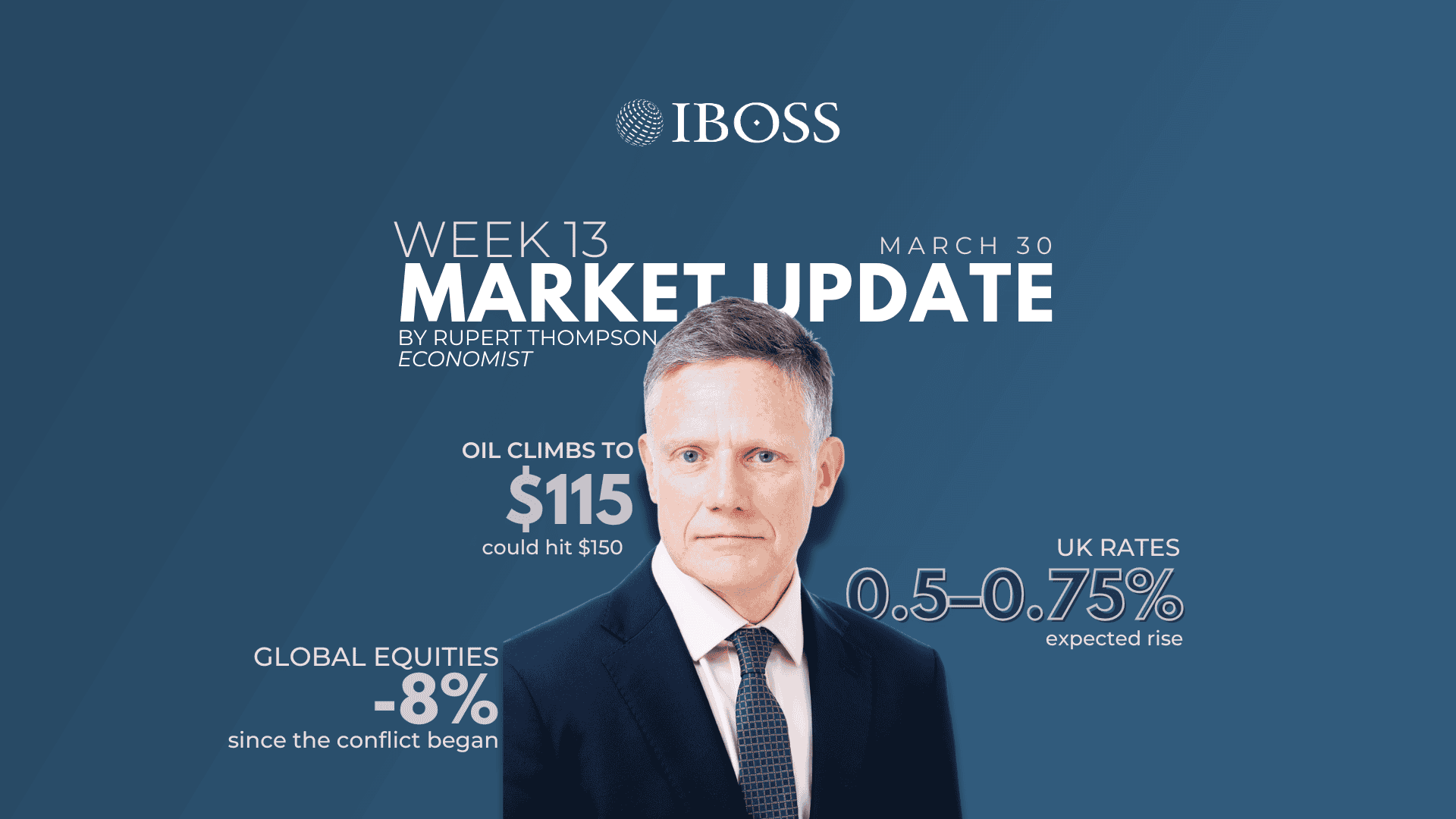

Unsurprisingly, oil prices had quite a volatile week on the back of all this with equities taking their lead from them. The Brent crude price dipped below $100 per barrel mid-week but ended it little changed at around $110 and is up to $115 this morning.

Global equities finished the week down around 1.3% in both local currency and sterling terms. Whereas the US and emerging markets both lost 1.5-2% in sterling terms, the UK, Europe and Japan were all up a modest 0.5% or so.

Since the conflict began, global equities are now down 7% and 8% in local currency and sterling terms respectively and have basically erased their gains since the autumn. The US has held up a bit better than the rest of the world, helped by a strengthening of the dollar and its economy being energy self-sufficient, and is down 6.5% versus an 8% decline elsewhere. Nevertheless, this still leaves the US trailing the rest of the world by close to 7% year-to-date.

Government bonds were little changed last week but US Treasuries and UK gilts have lost 2% and 4% respectively since the war started. The Fed and Bank of England may have kept policy on hold at their meetings last week and emphasised the extent of the uncertainties surrounding the war and its impact on the economy. But markets have been much quicker to jump to conclusions.

Prior to the war, interest rates had been expected to be cut a further 0.25-0.5% later this year in both countries. Now by contrast, the market expects rates to be kept unchanged in the US and to be raised 0.5-0.75% in the UK.

In the case of the UK, this looks like an over-reaction. For sure, inflation is headed higher. Last week’s numbers showed headline and core inflation running at 3.2% and 3.0% respectively in February and the headline rate now looks likely to rise to 3.5-4% later this year. Against that, tough talk from the Bank, along with the hit to growth from the rise in energy prices, should limit the pass-through to underlying inflation and probably keep any rate hikes to a minimum.

Still, there is no getting away from the uncertainty surrounding the current situation. The surge in gasoline prices in the US will be putting increasing pressure on Trump to end the conflict and re-open the Strait of Hormuz as soon as possible. But this will hinge on Iran as much as the US.

We are left with two very different scenarios. The first comprises a cease-fire deal being agreed over the next few weeks which both sides would need to be able to portray as a victory. If this were to happen and the SOH largely reopened again, markets would very likely unwind their losses in short order.

The second involves the US ending up deploying the troops it has now amassed in the region to try and secure Kharg Island and/or the SOH. The general view here is that this will be hard to achieve with US troops likely to come under continued attack from Iran and the SOH could remain closed for weeks or months to come.

In this case, oil could very well head up to $150 per barrel and lead to the global economy falling into recession at least briefly later this year as the price hike and shortages take their toll. Last week’s US, EU and UK business confidence data showed the conflict hitting sentiment in March although it still remains in expansionary territory.

Estimates of the potential damage done to the global economy have been rising as it has become clear that the closure of the SOH and damage to the energy infrastructure is not only restricting oil and gas supplies but leading to shortages and price hikes in other products such as fertiliser and helium.

Attacks by the Houthis on Israel over the weekend have also highlighted the danger that they could start targeting shipping coming through the Bab-al-Mandab strait at the Southern end of the Red Sea, adding to the disruption to oil and trade flows more generally.

If the second scenario comes to pass, equities would undoubtedly fall further. But with the first scenario still quite possible given the mounting pressure on Trump to resolve the conflict quickly, the danger of cutting equities now is being whipsawed given markets are already off significantly from their highs and the situation changes on a daily basis.

As we have pointed out before, the lesson from most past wars and geo-political crises is very much that one should resist the urge to sell and stay the course. Indeed, it is worth remembering that back in 2003, US equities started to recover the very day US troops moved into Iraq.

Other than the war, the only other news of note last week was that Meta and Google were found guilty in the social media addiction trial in the US. While they will appeal the verdict, the danger is that this sets the scene for further such cases and will require the companies to put in safeguards which restrict their growth. Meta and Alphabet (Google’s parent company) ended the week down 11% and 9% respectively.

This week, Iran will obviously remain the key to market moves, particularly with Trump’s deadline due to expire on Easter Monday. Still, we do also have Eurozone inflation numbers for March on Tuesday, which will be boosted by the surge in energy prices, and US payroll data for March on Friday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 108.4.26