At the time of writing (06:28 on 14 April), markets are feeling positive. As investors rather than traders, daily or weekly movements rarely matter unless accompanied by a change in underlying investment conditions.

What Does Matter?

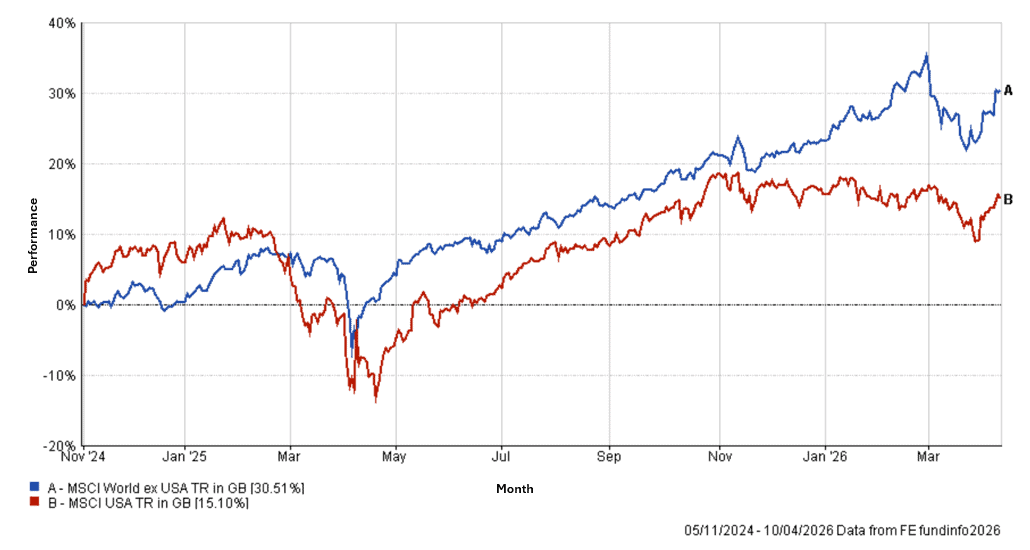

In the early days of the second Trump presidency, US markets hoped for a repeat of his first term. A period characterised by the outperformance of US assets. By December it became clear that this was a more emboldened, better organised administration with a radically different agenda to the first iteration. Trump 2.0 has been more of a tailwind for other markets than the US, with World ex-US outperforming by 100%.

Total Return Performance Line Chart Since the Beginning of President Trump’s Second Term – 05/11/2024-10/04/2026

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends. Investors should consider longer-term performance data and other relevant factors before making investment decisions.

Over this period, the administration has largely alienated its friends and further antagonised its enemies, to the point where it is hard to define who its ‘friends’ are. So much so that new agreements and co-operation between countries other than the US seems to increase on almost a weekly basis.

Faith in the US government’s willingness to stick to deals or tariffs continues to diminish. Trust between nations has rarely been more valuable, nor scepticism higher. Trump 2.0 has driven the biggest shift in how nations approach energy security, supply chains, defence strategy and economic partnerships since the Second World War.

This new landscape, though initially unsettling, creates opportunities at both country and company level. Looking five to ten years ahead, little is certain, but the world is unlikely to revert to its pre–Trump 2.0 state. Portfolios must reflect where we are and where we are going, not where we were, implying the need for greater diversification and meaningful allocations to regions in the ascendency, notably Asia and Latin America.

A Safe European Home

One recent event with potentially broad implications is the ousting of Viktor Orbán after sixteen years as Hungarian president. For much of his tenure, he was a thorn in the EU’s side, notably blocking aid to Ukraine.

His removal is a boost for EU and Ukrainian morale and particularly welcome for EU countries pressured by the Trump administration. J.D. Vance’s late attempt to support Orbán failed. His removal may reinvigorate EU cohesion and support for Ukraine at a crucial time.

When assessing opportunities, we believe Europe should be firmly included. Some of the best opportunities arise when a headwind is removed rather than a tailwind introduced. While Hungary was not the EU’s only issue, it was among the most potentially intractable.

The Next 30 Months

We do not believe either the Iranian Revolutionary Guard or the Trump administration knows how the conflict will evolve from here, and neither do we. What we do expect is a continued stream of executive orders through to the next election, aimed at reinforcing a Trumpian agenda under a similar Republican leadership and into a new presidential term.

These policies likely include pressure on the Fed to cut rates, fiscal spending where possible, and efforts to reduce petrol prices. Economic stimulus, explicit or otherwise, will be a priority and could support US equities. We retain a large position in the region, however there remains a risk that such measures fail or prove ineffective.

Outside the US, we believe that countries will look to deepen new alliances, secure energy through stable partnerships, and pursue bilateral and multilateral agreements among aligned nations.

At a portfolio level, this reinforces the need for genuine diversification across geographies and sectors. Central banks are unlikely to raise rates significantly without damaging demand, therefore easing pressure on smaller and mid-sized companies and creating opportunities in more beaten-down areas. The risk/return profile of REITs and infrastructure also appears increasingly attractive.

In short, multiple opportunities remain in the investment era that began in November 2024 and looks set to persist for years.

IBOSS Performance Update

60% of IBOSS portfolios outperformed their respective benchmarks in March across Core, Passive and Decumulation ranges. Overall, portfolios with lower allocations to equities performed best relative to their benchmarks, helping to protect capital amid rising uncertainty following the closure of the Strait of Hormuz and the market volatility that followed.

By contrast, portfolios with higher equity exposure saw some underperformance against benchmarks, as several regions that had previously delivered strong returns experienced some underperformance. This period was impactful but very short lived as the US dollar acted as something of a safe haven asset for a total of two days. As a result, US assets held up better than those in other regions, an area where the portfolios remain strategically underweight in favour of broader regional diversification, which has historically supported more consistent returns and risk outcomes over the longer term.

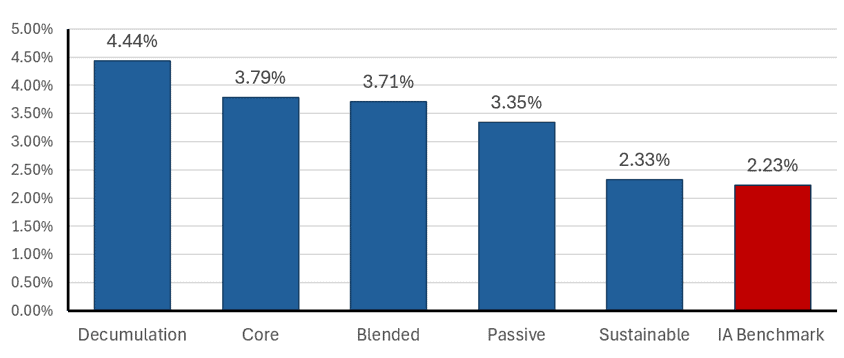

It is also worth noting that when there are signs of the conflict easing, US dollar strength has tended to fade quickly, with a return to earlier trends, namely a weaker dollar and stronger performance in other regions. This has been reflected in year to date results, where all Core, Passive and Decumulation portfolios, along with all but one Sustainable portfolio, have outperformed their benchmarks.

Portfolio 4 performance across IBOSS MPS ranges – Year to date (10/03/2026)

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends. Investors should consider longer-term performance data and other relevant factors before making investment decisions.

While all ranges have delivered strong performance relative to their peer groups this year, the Decumulation range stood out in March, helping to shield investors from the more challenging conditions that emerged at the onset of the conflict in Iran.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 112.4.26

Approved April 2026