At the time of writing, discussions of asset allocation, macroeconomic outlooks and geopolitical events continue to dominate the headlines. Advisers are frequently presented with arguments why one region’s fundamentals may be deteriorating, another is undervalued and unloved or why now may be the right moment to rotate exposure.

However, while asset allocation will always be an important component of returns and portfolio construction, it is not the only one. Fund selection is also very as important and its these two factors combined that determines whether outcomes will meet expectations.

Since the start of 2025, markets have moved into a new paradigm, one which is seeing relationships forged over many decades being reinterpreted or even discarded altogether. The period of initiated by Trump’s second term is the most seismic shift in markets dynamics since the GFC.

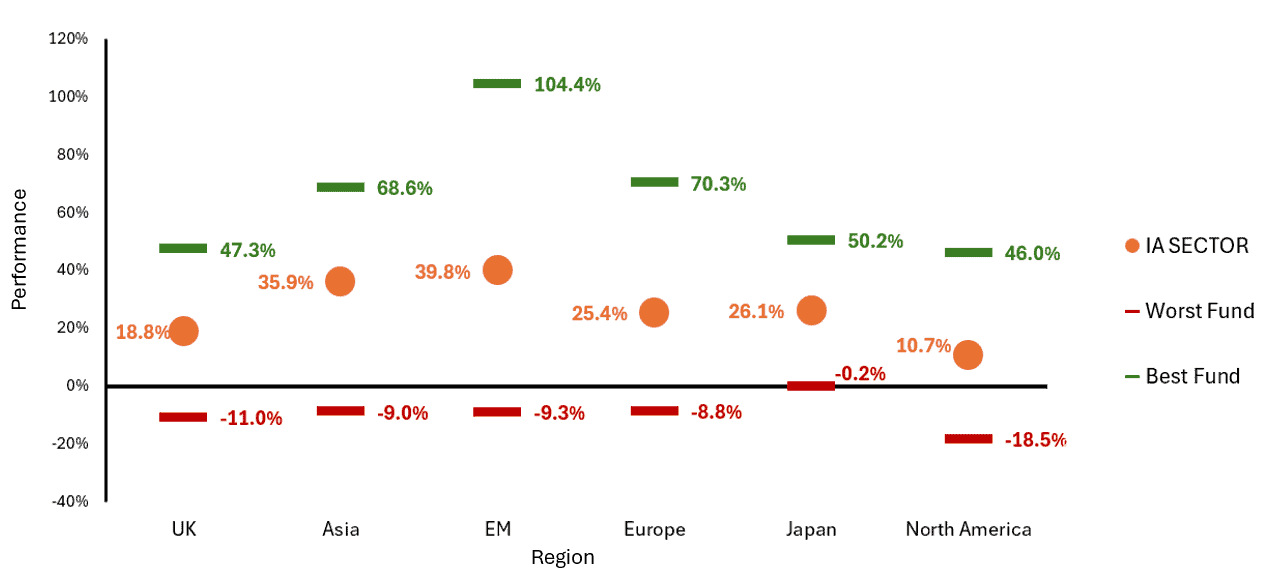

As illustrated in Figure 1, the dispersion between the best and worst?performing funds across key IA sectors has been pronounced. In environments where this divergence is most stark, fund selection can be as influential to client outcomes as broad asset allocation itself.

Figure 1 – Equity Attribution Analysis – Fund Selection in 2025 & 2026 to date*

Source: FE fundinfo *31/12/2024 to 24/04/2026

The Reality of Passive Investing

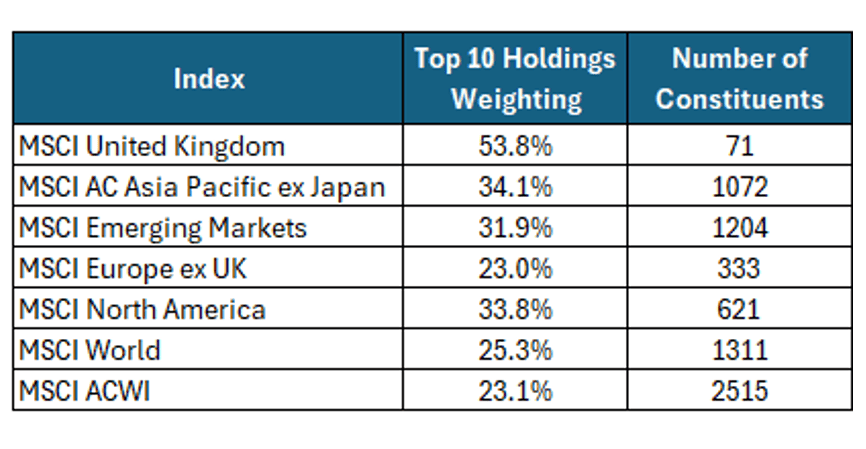

Passive investing is often positioned as a diversified way to access broad markets. However, in practice, it has become increasingly concentrated, with returns driven by a relatively small number of large-cap companies.

This is particularly evident across indices such as Asia Pacific and Emerging Markets, where roughly one?third of index weight sits in the top 10 despite more than 1,000 constituents. At a global level, the MSCI World and MSCI ACWI indices exhibit a similar dynamic, with 23-25% of weight concentrated in the top 10 (see figure 2).

As a result, passive strategies may appear diversified by the number of holdings, but in practice, outcomes are increasingly driven by a narrow group of dominant companies.

Figure 2 – Regional Equity Index Top 10 Weighting and Number of Constituents

Source: MSCI, as at 31/03/2026

Active vs Passive

The relative performance of active managers is often framed in broad terms; however, the reality is more nuanced. Recent data from Morningstar highlights a clear divergence between asset classes, and even within equity markets.

Within equities, it’s common to speak negatively of active equity managers who have continued to face significant challenges, with the increased dominance of passive investing. With a one?year success rate of 31.2% up to 31st December 2025, it still indicates that the majority failed to outperform passive alternatives. However, this masks the most important point, which is the wide dispersion in outcomes. As illustrated in Figure 1, the gap between the best- and worst-performing funds within the same sector can be substantial, with the top Emerging Markets fund returning over 100% compared to a decline of over 9% for the weakest performer. This is particularly notable given the relatively higher success rate of active managers within Emerging Markets, at 49.6% in 2025. Highlighting that even in areas where the odds of outperformance improve, the range of outcomes remains wide.

In contrast, fixed income has presented a more favourable environment for active management particularly since 2021and the ‘transitory’ misstep, and with the success rate for 2025 being 55.8%.

This divergence highlights an important point. In an environment where performance dispersion is elevated and returns are increasingly concentrated; fund selection becomes an important determining factor of outcomes rather than a secondary consideration. While the majority of active managers may underperform, those that do outperform can have a meaningful impact on overall portfolio performance.

The Cost of Selecting the Wrong Fund.

Selecting the wrong fund can have two significant consequences for a client’s portfolio.

The first is opportunity cost. This is illustrated within Emerging Markets (Figure 1), where over the period analysed, the best?performing fund returned 104.4%, the sector average returned 39.8%, and the weakest?performing fund declined by 9.0%. In a period of strong positive rising markets, a key risk to a client’s portfolio is for a fund to fail to participate in the higher level of returns available from other funds within the same sector. In portfolios containing more concentrated positions, a lagging fund can become a persistent drag on overall portfolio performance.

The second consequence is the potential damage to long-term returns. Holding one of or even the worst-performing fund doesn’t simply result in a short-term underperformance; it also creates a recovery hurdle. For example, the worst-performing fund in IA North America since the start of 2025 to 24th April 2026 has declined 18.5%. A client holding that fund now requires a return of more than 22% just to recover their original capital. While the broader market continues to grow, that holding is forced into recovery mode, potentially widening the gap in outcomes over time.

Translating Percentages into Pounds

Performance is often discussed in percentages, quartiles and basis points. For clients, however, the impact is ultimately experienced in pounds sterling.

Using the IA North America example, consider a client with a £500,000 portfolio, aligned to a medium?risk benchmark (IA 40-85% Shares) with an approximate 31.5% allocation to North American equities. This equates to £157,500 invested in the sector.

Over the period analysed in Figure 1, the difference between holding a top?quartile fund returning 14.53% (25th Percentile) and the worst returning fund (-18.5%) within the sector equates to a potential shortfall of approximately £52,000 on that allocation alone.

These figures represent meaningful differences in future lifestyle outcomes, driven solely by fund selection rather than asset allocation or client risk appetite.

The IBOSS Approach

Elevated levels of return dispersion are not a short?term anomaly. History shows they are a persistent feature of markets. Managers who have performed strongly over recent years can just as quickly fall behind peers as conditions change, often for reasons that are not immediately apparent or predictable.

This reality reinforces a simple truth; fund selection is hard. It requires ongoing scrutiny, a clear framework for assessing performance and risk, and the discipline to respond when funds no longer behave as expected. It is not a one?off decision, but a continuous on-going process.

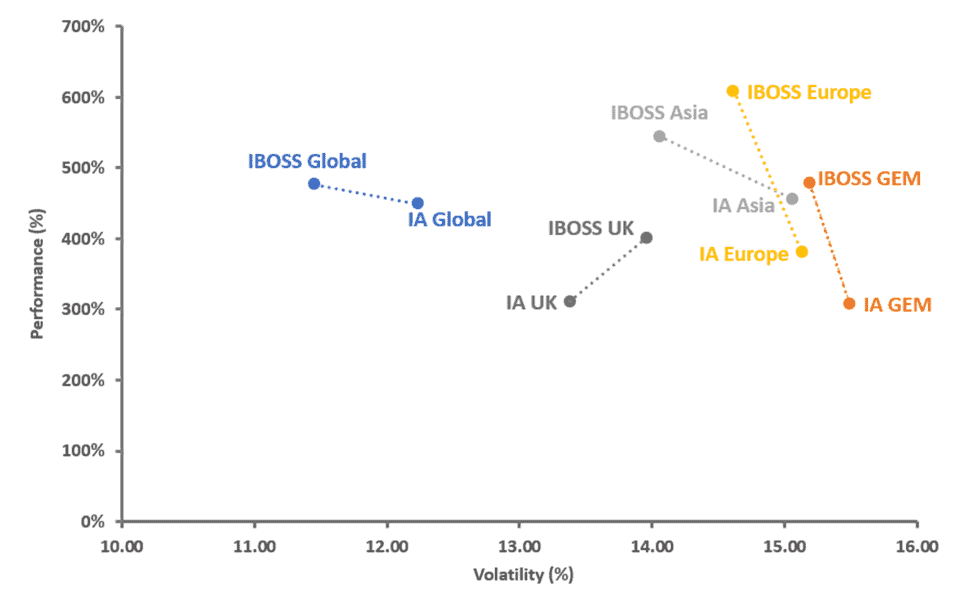

For nearly 18 years, IBOSS has partnered with advisers by taking on this burden of choice. Our focus has been on maintaining a consistent and repeatable approach to fund selection, portfolio construction and oversight, with the aim of delivering good outcomes for clients over the long term. As illustrated in Figure 3, each of IBOSS Core MPS 4 regional equity allocations illustrated has outperformed its respective sector average, while the majority have done so with lower volatility.

Figure 3 – Equity Sector – Fund Selection 31/10/2008 to 31/03/2026

Source: FE fundinfo

Returns shown net of fees, income reinvested. Benchmark: IA sector average, used for comparison purposes only.

Ultimately, prudent fund selection and thorough governance can contribute significant value that helps ensure the portfolios meet the client objectives over long term. In an environment where outcomes can diverge significantly, having a dedicated investment partner (IBOSS) focused on this challenge can make a meaningful difference.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 129.5.26