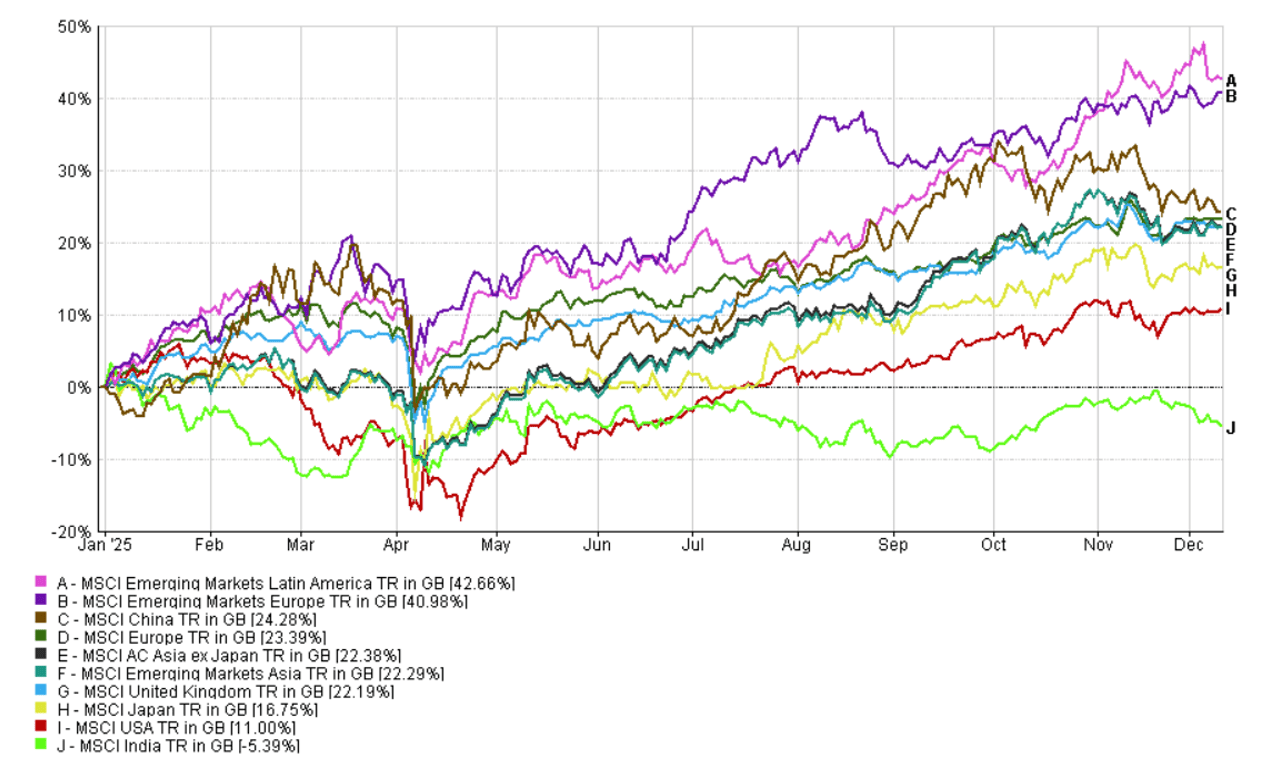

This update covers the period year to date to 10 December 2025. On the surface, looking at markets over the last few weeks, it might seem little has changed but under the surface, we are witnessing a ratcheting up of some major geopolitical situations and some renewed questioning of AI related stock valuations. The winners (Fig.1) however have remained broadly the same, though China continues to give back performance with significant economic headwinds yet to be offset by sufficiently increased stimulus.

MSCI Selected Country Indices > 11/12/2025 (Fig.1)

Source: FE Fundinfo

So many wars, so little time

The Trump administration has temporarily at least moved away from Middle East issues to focus on the Russia and Ukraine situation while simultaneously becoming ever more aggressive with Venezuela. Aside from the threats to the sovereign states and the human tragedy that accompanies all wars, declared or otherwise, both these conflicts have major implications for markets. First and foremost, it’s the commodity complex which affects global prices, but then sectors such as defence, infrastructure, and consumer staples etc will also be affected to differing degrees but not uniformly across the geographies. Of less impact for markets but just as miserable for humanity, the Trump administration last week brokered a peace accord between Rwanda and the Democratic Republic of Congo (DRC). Unfortunately, but almost inevitably, fighting escalated in eastern DRC shortly afterward, with the Rwanda-backed rebel group M23 making further territorial gains. The US president is very quick to take the plaudits from stopping wars but realpolitik is much messier than would ideally be the case. However, what critics of Trump’s unconventional approach to ending wars often don’t tall about is how they would do things differently to bring disputes of all kinds to an end. Africa is becoming ever more important to many nations efforts to control their supply chains. Any country who doesn’t control their supply chains will by definition be beholden to other countries and who knows which countries can be trusted these days. One thing is for sure, time is of the essence to become self-reliant where possible and where it isn’t, work out who your new friends are.

Practice Run?

On the 10th December we witnessed another factor that will be a theme throughout 2026 and beyond. Oracle’s results came out and they were fine in themselves but then the markets quickly digested the huge cap ex spending coupled with higher debt levels and leading to the stock falling 12% in after hours trading. As usual the supporters of valuations of AI related stocks going “to the moon” say there is nothing to worry about and the ‘bubble brigade’ wheeled out the canary in the coalmine analogy. We are not clever enough to understand what fair value for any of the tech stocks is but the ratio of bulls to bears does seem to be going towards the bearish end of the spectrum. Those same stocks have supported the broader US index throughout 2025. However, only in the US is their such a large concentration of very high valuations in such a small cohort of companies. Of course, it can be argued that TSMC is circa 40% of the Taiwanese market, but the main difference is that US stocks make up 70% of global indices and that matters, especially to passive investors and we remain unconvinced about how many people realise how concentrated ‘global’ as a sector is these days.

Advantage Active?

All this means a dynamic backdrop of threats and opportunities which in theory at least should favour active management. Indeed, this has been the case through much of 2025 and as a company that run the whole gamut of active, passive and blended portfolios, we agnostically surmise that the current global macro factors favour managers that have choice about not just what to own but as importantly what not to own.

We have been here many times before and active managers as a single entity will also produce some returns better and some worse than the passive alternatives. It must be said though that the divergence of returns withing sectors and geographies has never been greater. This doesn’t feel to us like a time where just buying cheap beta is going to be a winning strategy and we say that whilst acknowledging that that a cheap beta strategy had worked for much of the period between the GFC and the start of President Trump’s second term.

Performance Update

As the year draws to a close, we’re pleased to report that the IBOSS MPS ranges have performed well relative to their respective peer groups this year, following another positive month of relative performance through November.

The regional allocation of the IBOSS portfolios equity position tends to be more diversified than much of the peer group, and whilst many investors accept that diversification can be beneficial in more difficult market conditions, it can also drive returns in a rising market that rewards a broader spread of assets.

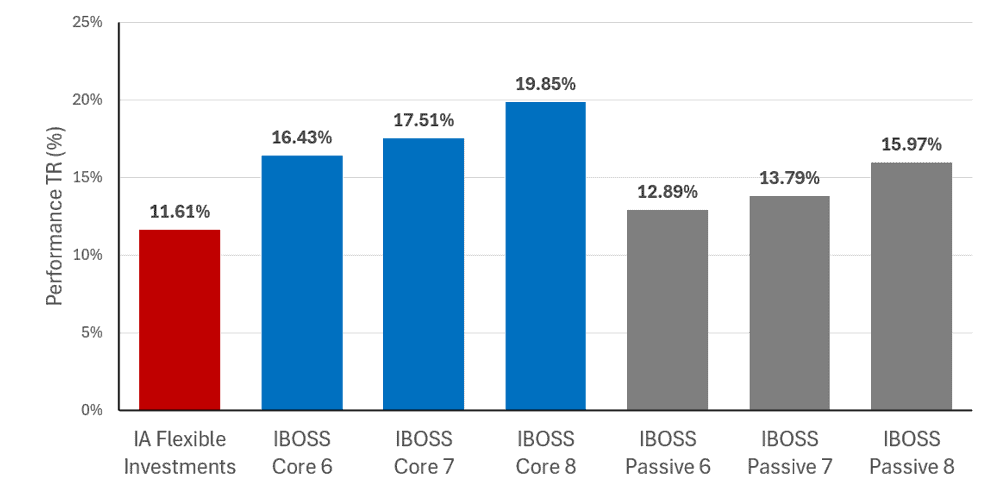

This is perhaps best reflected in our higher risk portfolios which have so far outperformed their respective benchmark (fig2). This outperformance has been driven by a combination of fund selection and asset allocation and a broader exposure to global equity markets, including emerging markets, Europe and the UK.

Looking ahead to 2026, we expect investors to continue to be rewarded for diversification as global uncertainty remains high. As a result, investors can anticipate a similar approach from IBOSS: one that remains focused on broad diversification, risk management and the ability to participate in growth across a wide range of markets and asset classes.

Fig 2: 2025 Performance – Higher Risk Core/ Passive Portfolios

Source: FE Fundinfo

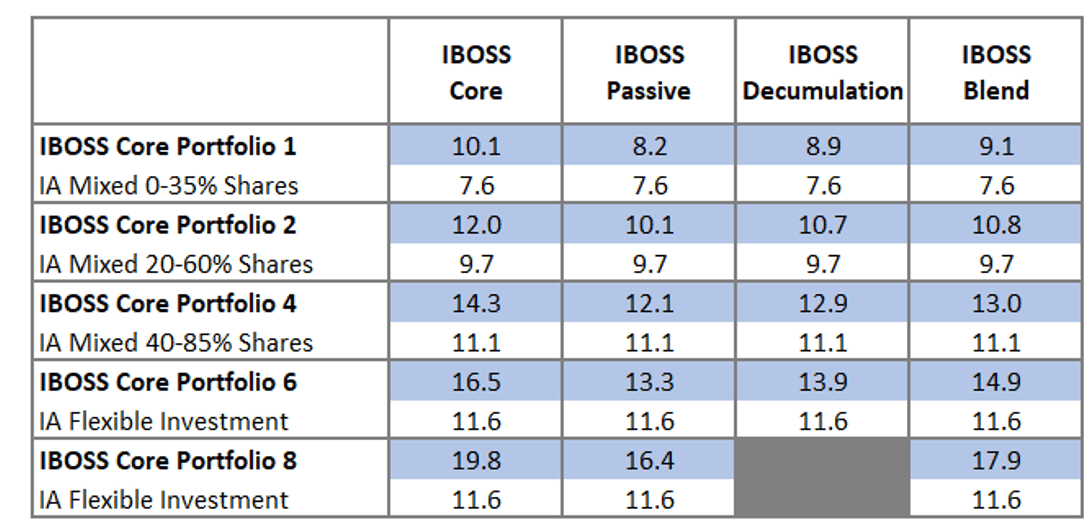

Fig 3: IBOSS Core / Passive / Decumulation / Blend MPS – Year to Date

Source: FE Fundinfo

Whilst all ranges have outperformed their respective benchmarks this year, the Core range has outperformed the other ranges. This has largely been due to fund selection where 2025 has seen many active managers outperform their passive equivalent.

IBOSS Sustainable MPS

Whilst sustainable portfolios on the whole have struggled over recent years, the IBOSS sustainable range has continued to perform well against other sustainable MPS portfolios. The chart below demonstrates the Risk characteristics and performance figures for the Sustainable range against this peer group.

Cumulative Performance to 30/11/2025 ranked against MPS Peers

Source: FE Fundinfo

5 Year Scatter against Sustainable Peers

Source: FE Fundinfo

As ever please do contact a member of the team if you have any queries, and look out for our new blog post which covers some of the frequently asked questioned posed to the IBOSS investment team.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 360.12.25