Following the supposed ‘banking crisis’ in late March, market movements during April have reflected a further easing in concerns over the banking sector. There has been no real news, but the absence of any new nasty surprises has been viewed as encouraging.

After a prolonged period of market participants being rewarded for concentrated bets in growth, commonly large tech and often US-listed stocks, the playing field has been somewhat levelled. Central banks worldwide have progressively diverged interest rate policies, leading to, amongst other factors, the currency you invest in becoming increasingly important.

The key to portfolio stability though, so far in 2023, has been diversification across geographies and asset classes.

Europe – a surprise winner

The news flow emanating from Europe was already somewhat negative at the beginning of 2022, but it got dramatically worse following Russia’s Vladimir Putin’s invasion of Ukraine.

The predictions of blackouts and an ensuing economic collapse seemed extremely plausible as Autumn approached. Several factors meant that the most pessimistic scenarios were avoided, and the most significant contributing reason was the mercifully mild winter. As is often the case with investing, it is rarely a good idea to be too confident in any one outcome.

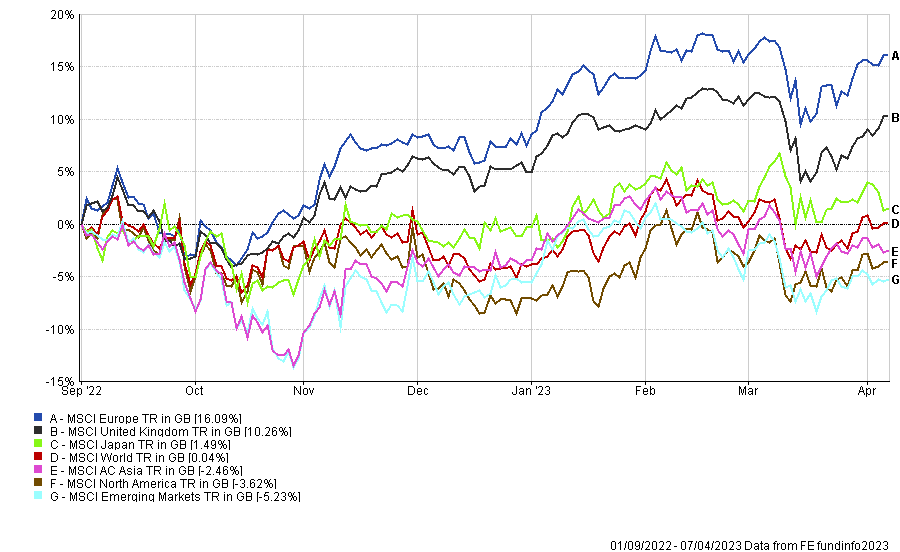

While many investors were understandably nervous about European prospects, the reality is that European equities have easily been the best-performing market since peak pessimism in September last year (fig 1). The second best-performing market has been UK equities, and both areas have far outperformed the US equity markets.

MSCI Global Index Performance – 01/09/2022 to 07/04/2023 | (fig 1)*

The Return Of Bonds

It has now been well-documented that 2022 was one of the worst years in history for the combined global bond market. Governments and central banks worldwide will remember factors such as the near catastrophic mini budget in the Autumn for years to come. What has transpired since then is another lesson in market psychology and yet another example of why investing using the rearview mirror can harm an investor’s returns.

Since the middle of October, when many bond markets hit their lows, UK Gilts and corporate bonds are up approximately 13%, with index-linked gilts up almost 30%. At the time of writing, all the major fixed-income sectors are in positive territory, with only exceptions being some bond funds with concentrated positions in banks and financials. Even here, the risks of taking too concentrated sector positions have become clear again. Whilst some say the banking sector issues were inevitable in a rapidly rising interest rate environment, we cannot recall many people saying it beforehand.

Gold

Our gold-related allocation in portfolios has a low correlation to our mainstream bond and equity holdings, meaning it remains a beneficial source of diversification within this year’s market environment.

Earlier in the month, gold rose to $2,045/oz, close to the previous high of around $2,050 in August 2020 and March 2022. At the time of writing (20/04/2023), the price of gold remains above $2,000/oz and is supported primarily by the weak dollar and hopes of interest rate cuts.

Within our portfolios, we allocate to the Ninety One Global gold fund. The fund invests in gold miners rather than directly in the precious metal. The fund is up circa 16% year to date and almost 40% from its lows in September of last year.

Harvesting the Opportunities

As the age of deglobalisation and central bank divergence plays out, it will throw up new winners and losers. It seems highly likely that the winners of the ‘just in time’ supply chains’, highly synchronised economies and beneficiaries of the low inflation, low-interest rate era will not be the same as they were for much of the last decade. We can expect more volatility in the coming months, and years, as the world comes to terms with new political and economic realities.

One thing we do know is that the new era, which we believe started at the end of 2021 when central banks realised they had serious inflation issues, will bring new opportunities. A manager’s ability to harvest this increased volatility and avoid concentrated positions based on what worked in the past will be crucial to producing a good outcome for investors.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for informational purposes only and is not intended as investment advice. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Please note that the content is based on the author’s opinion at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available, this is not intended as investment advice.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

Registered Office: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 130.4.23