In last month’s market update, we highlighted the turbulent market conditions and how one week can bring positive gains only to be followed by broad market declines the next. This has been very much the case over recent months, and whilst not necessarily within the purview of this update, it is impossible to focus solely on market movements in July without considering those already experienced this month.

This is because July was a largely positive month for investors. Equity markets were very much “risk on”, and we saw most equity markets post positive returns. Developed market equities gained around 2%, whilst exposure to emerging market equities, particularly China, yielded investors a gain of 5% and 10%, respectively. Things were similarly positive in the fixed income space, with everything from gilts to corporates seeing a modest positive investor return.

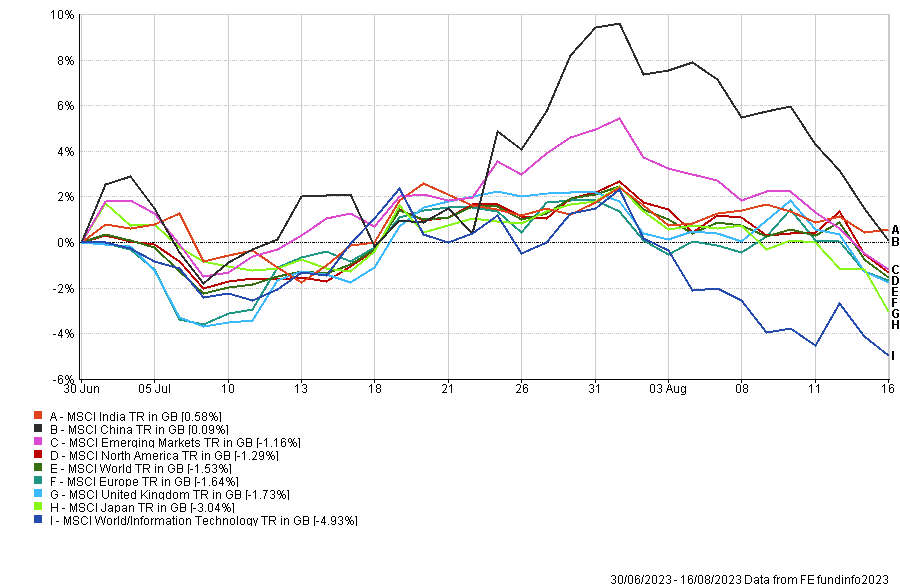

Fast forward to the first half of August, and things look markedly different. We have experienced broad market declines, with emerging markets suffering the brunt of underperformance, exceeded only by the difficulties faced by the technology companies that had previously performed so well. In the case of China, the moves have erased last month’s gains. However, it is worth noting that despite the volatility, an allocation to China has so far been a net positive against other developed markets (fig 1) and the region is still up 15% since its low in November of last year.

Global Equity performance – 30/06/2023 – 16/08/2023 (fig 1)*

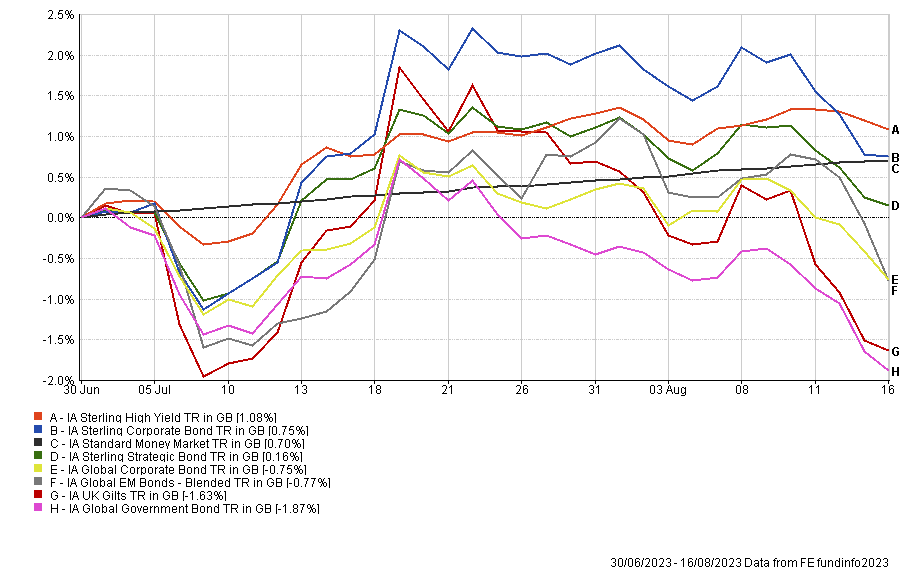

Things look similar in Bond World. So far, the marginally positive returns of July have been erased through the start of August (fig 2).

Fixed Income performance – 30/06/2023 – 16/08/2023 (fig 2)*

The catalysts for the market downturn are many and varied, and pinning the market response to a single event amidst the noise is incredibly difficult. We saw an unexpected downgrade of the US’ debt by Fitch, which drew focus to the sharp rise in the US budget deficit. We’ve seen some earnings on large tech companies and whilst these have so far been positive, given the sharp run-up in these stocks this year, this was arguably the minimum required to justify the gains.

Last week, the primary focus for investors was inflation. Developed markets saw no big surprises, but the Chinese data sparked a wave of headlines proclaiming a slide into deflation. In reality, the numbers were somewhat less worrying. Pork prices were a significant factor behind the 0.3% drop in consumer prices versus a year earlier, and core inflation rose in July to 0.8% and remains in the 0.5-1% range of the past year.

While the strength of the post-covid economic rebound has undoubtedly disappointed, Chinese growth still looks set to be around 5% this year, compared with no more than 2% in the US and an anaemic 0.5-1% in the Eurozone and UK. Importantly, high youth unemployment and the absence of inflation mean the authorities should continue introducing further piecemeal stimulus measures. We remain positive on Chinese equities as valuations are low and seem to be pricing in too gloomy an economic outlook. We also like emerging markets more generally. Valuations are cheap, particularly relative to the US, and interest rates look set to be cut sooner and faster than in the developed world.

In Summary, July was a positive month for investors and investor sentiment. However, a raft of uncertainty has challenged that sentiment in August. We believe that this level of volatility is likely to continue, and whilst it may be concerning for investors over the shorter term, it will undoubtedly present opportunities for longer-term investors. These opportunities may very well be found in areas that have been less popular over recent years, therefore, diversification is critical to reducing short-term volatility yet remaining open to longer-term opportunities.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 235.8.23