Given the falls we saw in equities and bonds last year, alternative assets are playing an increasingly important role in ensuring a client’s portfolio remains thoroughly diversified during challenging market conditions.

Two optimal alternative investments are property (land and the structures on it) and infrastructure (physical networks/systems that allow businesses/households to function. This includes industries such as transportation, communication, and utilities).

Property and infrastructure funds are also considered an asset class that offers protection against inflation, a topic we have all become familiar with over the past 12 months. The tangible nature of such assets also leads to them being considered as more of a “real” asset.

When constructing the IBOSS portfolios, both asset classes offer diversification benefits, as well as acting as a source of capital preservation and appreciation, which is obviously an important goal for most investors.

Commercial Property

There remain obvious headwinds for property, including commercial property, which was once the dependable parent of the investment world, bringing regular income and delivering reliable capital growth with little volatility. However, it has been a perfect storm for the sector.

E-commerce had been denting high street rents for several years; Brexit then caused further wobbles before the pandemic saw off the office market as everyone decamped to their spare bedrooms. Businesses are still trying to get their heads around how much office space they actually need, and flexibility within employees’ contracts in regard to their working location has become increasingly important to most individuals during the post-pandemic era.

A lot of commercial property remains below the waterline. It is hard to see people going back to department stores and malls as they did before, or flooding back in numbers to an office environment, instead preferring the safety and comfort of online shopping, a trend that had already begun well before the pandemic, and enjoying the work-life balance a home office and no commute can bring.

Direct Property Funds

UK direct property funds have been in the press numerous times and largely for the wrong reasons. With the continual conflict between the daily dealt open-ended structure of these funds and the illiquid nature of the underlying (often chunky) holdings, it is not difficult to see why.

We sold out of our last direct property holding in August 2016. A time when it seemed to us that there was a seismic shift in sentiment towards physical property assets. As with many investments, if enough investors, the media and, most importantly, the regulators believe there to be an issue, then there is an issue.

With the recent rise in interest rates, clients now have several different options to generate yield/income without having to look at more illiquid physical property options. It will, however, be interesting to see whether the uptake of LTAF vehicles has an impact on direct property and how/if it changes sentiment for investors.

Infrastructure

Most of the property sector has seen its mantle seized by infrastructure, which showed its resilience in 2020. In contrast to commercial property, its income generation, often being government-backed and inflation-adjusted returns, has been relatively steady, and capital values have remained stable.

Infrastructure remains one of the few areas that still have cross-party government support, and most countries accept their infrastructure needs a refurb, not least the US.

Last June, the White House announced plans to raise $200 billion for solar projects in Angola, an undersea telecommunications cable linking the Far East with France via Egypt, and nuclear power production in Romania as part of a huge $600 billion G7 infrastructure plan designed to compete with China’s massive Belt and Road Initiative.

Here in the UK, the government has identified how important infrastructure is to levelling-up and tackling the cost-of-living crisis longer-term through the delivery of new domestic energy generation capacity, as well as transport improvement projects such as Crossrail and the first new nuclear plant to open in the country in more than 20 years, Hinkley Point C.

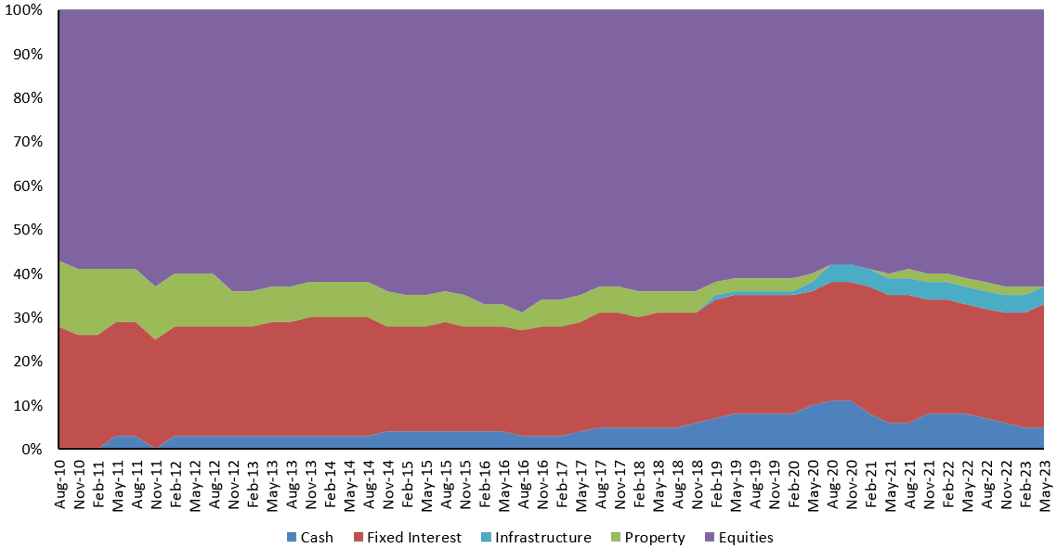

IBOSS Portfolio Allocation

As we stand today, the model portfolios currently have a combined weighting of approximately 6% in property and infrastructure, which has helped us diversify our clients’ investments over the last 12-18 months. It is our view that inflation will continue to make real assets (precious metals, commodities, real estate, land, equipment, and natural resources) good sources of diversification from bonds and stocks in the current market environment.

However, the upcoming portfolio fund changes for Q2 2023 will see us remove our property holdings entirely. This is because, in the round, the risk-return profile of the property sector continues to deteriorate, and we see better opportunities elsewhere.

We have consistently held property as part of our asset allocation since November 2008, except for a brief period between May 2020 to February 2021 where we held no allocation to the asset class. In the chart below, you can see a visual of our asset allocation over a 13-year period, whereby the property sector has slowly decreased, and infrastructure has increased in recent years.

We currently hold the Lazard Global Listed Infrastructure Equity, M&G Global Listed Infrastructure and L&G Global Infrastructure Index funds within the infrastructure sector. It is important to note that there is a considerable difference in the make-up of the underlying funds in their respective peer groups, so this is not just a case of buying the index.

We will be further discussing the prospects for investing in infrastructure during our webinar in May, where the IBOSS investment team will be joined by the manager of the M&G Global Listed Infrastructure fund, Alex Araujo, who will be providing expert insight into the sector.

You can register for the upcoming webinar by clicking here.

This communication is designed for informational purposes only and is not intended as investment advice. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Please note that the content is based on the author’s opinion at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available, this is not intended as investment advice.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

Registered Office: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 139.4.23