Macro & Markets

The Ultimate Key Date

This update covers the period up to July 9th. This update primarily covers the first half of 2025, but we have extended it back to November 5, 2024, to encompass the entirety of Trump’s second presidency. As usual, we used the basic asset classes as a proxy for the broader markets (Fig. 1). Those more familiar with IBOSS will have often heard us talk of ‘key dates’ which signify market, geographic or sector inflexion points. Approximately three weeks after his election win, it became clear that the tariff situation would be much messier, more complex, and less conclusive than many investors had hoped for. It has since been argued that it also definitively ended the period of peak globalisation.

Asset Class Performance – 05/11/2024-30/06/2025 (fig.1)

Disadvantage America?

Whatever Trump thought about the economic world before his second term began, to many observers, America was far from being the victim of other countries’ economic policies; it was actually the principal benefactor. Perhaps the most obvious advantage the US had over others was known as the “exorbitant privilege”, which was the term given to the US dollar being the world’s reserve currency. This has enabled the US to maintain low borrowing costs and exert considerable influence over trade deals and financial markets.

For now, the US retains the reserve currency, but there has never been more effort by more countries to break free from dollar (and treasury) dependency. This subject has been discussed and hypothesised about for years. What is new, however, is the endless tirade of disdain and contempt from Trump towards other countries and their leaders. This is creating a fundamental breakdown in trust, reframing the rules of engagement and giving a new impetus to de-dollarise. In the Trumpian world, countries can go from hero to zero, as seen with Elon Musk.

Duplicity for Dummies

We think many countries and companies alike will have a game plan with two distinct elements. The first will be to say the things the current US administration needs and wants to hear on trade deals, procurement and whatever else is necessary to keep them out of the firing line. At the same time, however, those same countries and companies will be trying to minimise the chances of being threatened, sanctioned or having to make further concessions with a metaphorical gun at their head. This means forging new relationships and probably revisiting their old ones.

Working out the latest winners and losers is particularly difficult at times when the global economic tectonic plates are shifting. As new markets emerge, trade deals are reimagined, and national and economic security come back to the fore, the safest and most pragmatic approach is to have a truly diversified portfolio of investments.

The Demise of the Dollar

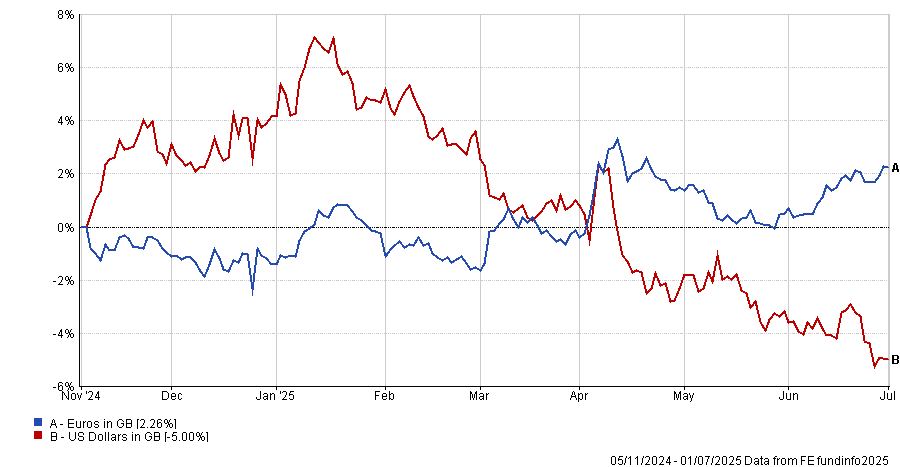

The last time the dollar dropped by the amount it has so far in 2025 was over fifty years ago, in 1973, during the Nixon era. The Current administration wants a weaker dollar; that much it has said, and so we can take it that they will do their level best to achieve this outcome.

They view it as a means to boost exports and encourage US manufacturing. Still, it’s never easy controlling the magnitude or trajectory of a currency move once it starts, and market forces take hold. It certainly doesn’t help UK or European investors when our currencies are rapidly rising against the dollar. The question we need the answer to is: how weak is too weak for the dollar according to Trump and Bessant?

US Dollar vs Euro – 05/11/2024-01/07/2025

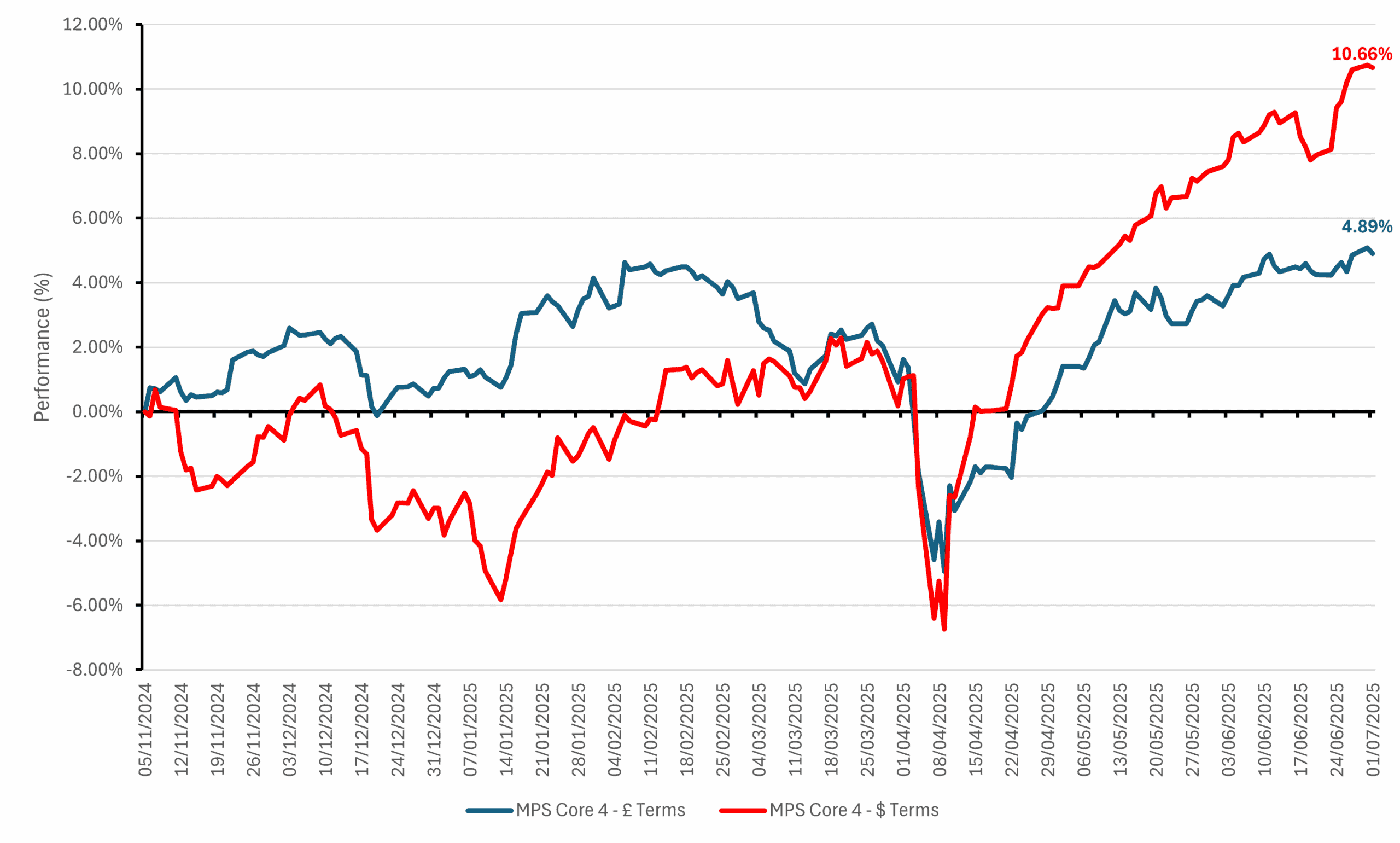

IBOSS Portfolio 4 performance- Sterling vs Dollar- 05/11/2024-01/07/2025

What’s Working In The Second Trump Presidency?

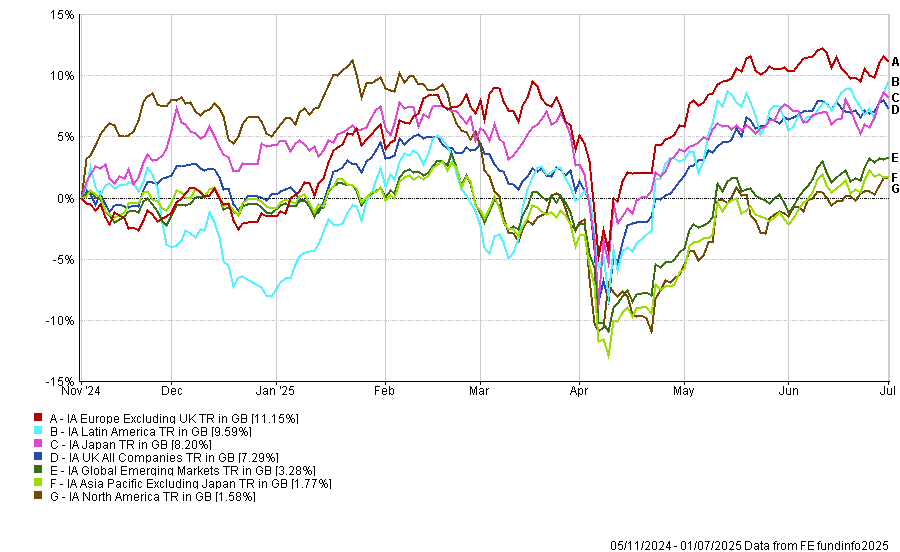

In the Equity space, it’s been the European renaissance that has been grabbing the headlines, but Latin America’s resurgence is perhaps a surprise to many. Given the attacks Trump has made, particularly on Mexico, it may seem intuitive that Latin America would be a potential victim of reimagined US policy.

However, the Mexican President, Claudia Sheinbaum, has already demonstrated she is not going to be pushed around by anybody. Brazil and Mexico are just one of many partnerships that are being actively and urgently pursued in light of the US economic policy to build much stronger ties. Even Europe and the UK are playing nicely and seem to be moving the relationship to a more pragmatic footing.

MCSI Selected Indices- 05/11/2024-01/07/2025

New horizons for Fixed Income

As new opportunities emerge in equities, fixed income also has plenty of scope to add value to a diversified portfolio.

One area we have been increasing our allocation to is Emerging Market debt, as the dollar structurally weakens, bringing an end to a cycle that arguably started after the GFC. The potential for an increasing flow of assets to emerging markets, either via repatriation or re-allocation, depending on the source, is virtually unprecedented.

Where we perceive a heightened risk is that the dollar’s decline is accelerating. This could be due to the US economy slowing down, but it’s more likely that the change in Fed Chair will usher in an era of increased political risk to economic decisions, in other words, someone who cuts rates because that’s what Trump has put them into doing. With a starting 10-year Treasury yield still north of 4%, the backdrop for active management in fixed income has rarely been brighter.

Performance & Positioning

The IBOSS portfolios have reacted comparatively well to the new world of asset volatility, drawdowns and general uncertainty. Investors continue to receive compensation for each unit of risk they take on, and we have maintained our relatively efficient frontier. June was a continuation of May, where BTD and FOMO investors, especially in the US, piled back into assets that had rewarded them previously. This now leaves us with many US assets that are even more expensive than they were before April, when expected earnings are taken into account. Despite this market dynamic, other assets are receiving positive flows and are being perceived differently, none more so than European equities. While many US assets had been priced to perfection at the start of 2025, European ones were priced for no good news ever to come.

It often takes some time before the behaviour of investors changes, and the longer the previous trends lasted, the harder it is for people to realise the world might have moved on.

Three years ago, many asset managers highlighted their sustainable characteristics, although much of this was often window dressing. Now we have managers championing their diversification characteristics, but so far, we are seeing only limited changes to many portfolios. With our upcoming changes, our portfolios will be more diversified than ever and positioned on the investing world as it is following the ultimate key date, the re-emergence of Donald Trump as US president.

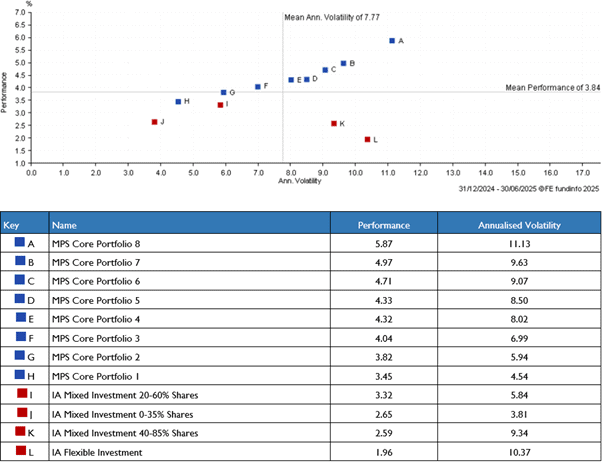

IBOSS Core MPS Portfolios & IA Benchmarks Performance Against Volatility – 31/12/2024-30/06/2025

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 187.7.24