At the end of 2022, it was tough to find an optimistic economist regarding the outlook for 2023. So far, in 2023, the markets, except for India, have looked through all the pessimistic forecasts. In fact, miraculously, they have had one of their strongest starts to a year for decades.

Furthermore, we have reverted to tech outperforming growth and both outperforming value by a considerable margin.

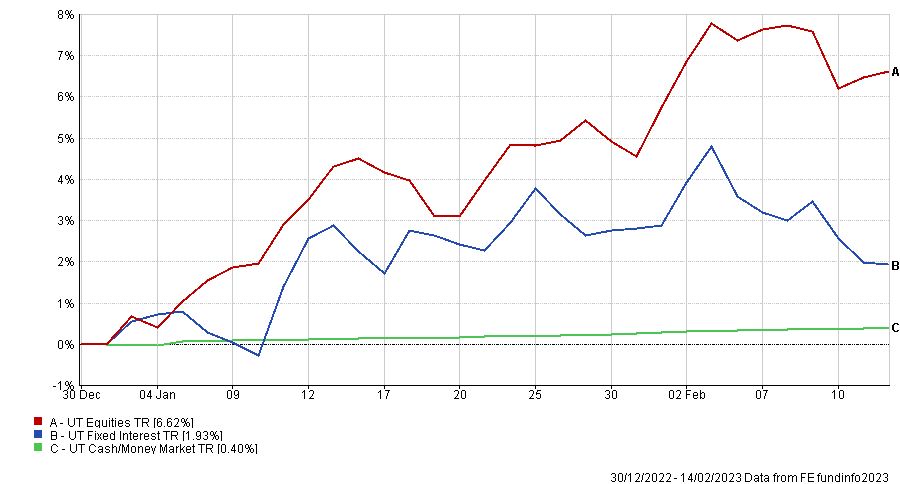

With reasonable justification, many commentators and managers alike were predicting bonds would outperform equities in 2023. It is still very early in the year, but so far, equities have not received that memo. At the time of writing (15th February), global equities are up circa 7% in contrast with fixed income, which is up in the region of 2%.

Asset Class Performance to 14/02/2023*

Given the economic data output so far in 2023, it’s somewhat puzzling to see how many equity markets have performed. Inflation, whilst potentially having peaked, remains stubbornly high. Central banks, especially the Fed and ECB, have been at pains to reiterate their determination to quash inflation and keep raising interest rates, leaving them higher for longer.

In simple terms, the question is this: how come the assets that did so well in the ‘lower for longer’ era are now surging in the ‘higher for longer’ era?

There appears to be only one plausible answer: the equity markets don’t believe the economy is as strong as some data suggests, and the central banks will therefore pivot quicker than some in the markets believe likely.

It remains our opinion that inflation will stay elevated, and way above the central bank’s 2% target, therefore, the pivot is wishful thinking rather than a likely outcome based on the available evidence.

We take the super positive current market movements, especially those in non-profitable tech, to be the result of highly speculative trading practices as opposed to people investing with a longer-term horizon. Recent market moves look to us to be a classic bear market rally. These usually carry with them a feel-good factor which is nice while it lasts, but eventually, a somewhat more sober reality will set in.

All that being said, we are not unduly pessimistic about risk assets overall. We still favour emerging markets, Asia and UK assets, and more value-oriented US stocks. Infrastructure continues to offer growth opportunities and diversification benefits, and we remain bullish longer term on the outlook for energy (of all forms) and commodities more broadly. There are still considerable opportunities within fixed income, particularly in the corporate bond space. Unlike some geographical areas within equities, bonds undoubtedly capitulated in 2022 and have attractive starting valuation levels.

*Information displayed is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 77.2.23