Inevitably, we have been asked more questions than at any time since the Global Financial Crisis regarding whether advisers and/or at least some of their clients should remain invested. The outcomes from an investment perspective are wide ranging and almost limitless in number. The points we make here are not recommendations but rather, for many advisers, just a reconfirmation of what we all already know.

Stop the Pigeon

We have, to some degree, covered this ground before but on the strength of adviser feedback we thought it worthwhile to cover it again. As human beings we often feel it is necessary to act in periods of crisis. In fact, doing almost anything feels as though we regain a semblance of control in situations that feel, at best, uncomfortable but can be just plain frightening. The words of the legendary pigeon catcher Dick Dastardly “Mutley, do something!” were used in times of crisis, but he never told his long suffering and medal bereft sidekick what to do, just ‘something’.

The Plan

All investments in the IBOSS range have come through advisers. So, we can assume that each client will have been through a thorough fact-finding review and that goals and investment objectives will have been ascertained. Furthermore, timescales and risk tolerances will also have been discussed. On the basis that the value of a client’s investment may have fallen, let us say 15%, what has materially changed for a client investing on a five year plus basis? What has not changed is that any of us has developed a new skill for short term market timing. It’s relatively easy to move out of risk assets in a selloff, but the really tricky part is when, if ever, you go back in and at what risk level.

What we sort of know and what we definitely do not

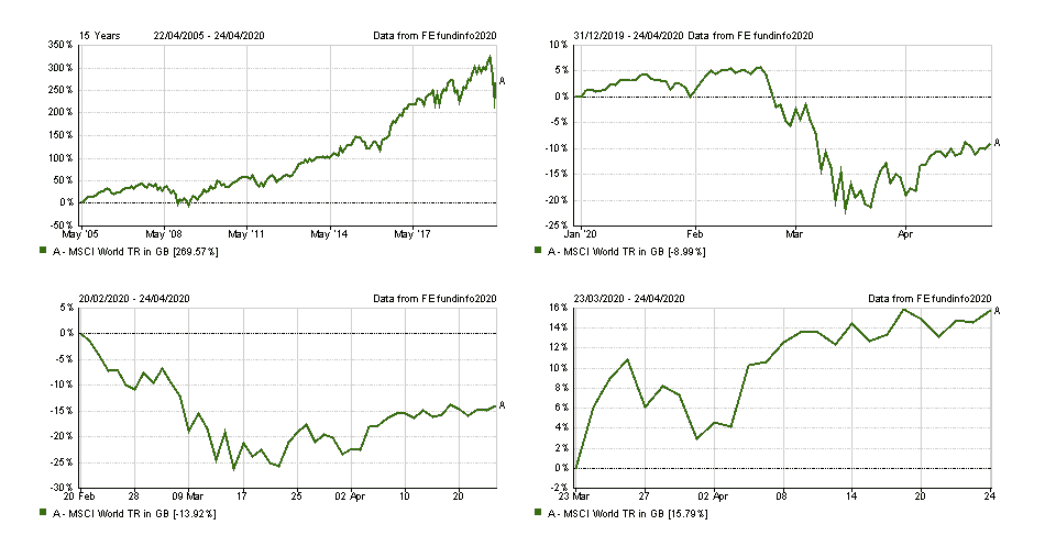

Some people will undoubtedly feel more nervous and even more cautious because they have experienced a paper loss. As an example, for anybody who held the MSCI World Equity basket of stocks and who moved to cash at the bottom of the recent drop, they have missed an almost 16% upswing which takes the loss for the year to circa 9%. Unfortunately, we have no idea where we are in terms of the next short-term market moves but it will highly likely be driven by the trifecta of Central Bank (monetary) policy, Government (fiscal) policy and the news regarding the impact of the virus on the world’s economy.

Behind the headlines

It is understandable then that some clients feel the need to reappraise their investment situation after market falls, a situation that is compounded by media reports of, for example, “X billion wiped off pensions”. It is worth considering that these same media outlets will not be quite as clear at indicating any market recoveries. A quick google search for “billions wiped of pensions” will end in an innumerable amount of results whilst the “billions added to pensions” results are virtually non-existent. As an adviser your last conversation with a client could have been weeks, months or even a year ago. This contrasts with salacious headlines which are very much in the here and now. A situation that is compounded by those clients that see the FTSE100 or Dow Jones as being the most important part of their investments – despite careful advice to the contrary. It is certainly not the client’s fault, after all, when was the last time the benefits of a fully diversified multi-asset portfolio in an equity market drawdown were discussed on the six o’clock news?

So, do nothing then?

“To do nothing at all is the most difficult thing in the world, the most difficult and the most intellectual.” These are the often-quoted words of Oscar Wilde, who was certainly no stranger to difficult situations. Just because ‘to do nothing’ is difficult doesn’t mean its necessarily the right course of action, however. What it might mean is that when advisers receive phone calls from their concerned clients they are able to reappraise the client’s situation in light of market movements. As an example, if a client had a tolerance for loss of X% and that tolerance has now been or is close to being reached, then this is potentially a material change for the client. This contrasts with a client who maintains the same risk tolerance, has the same investment time horizon but who feels they can suddenly time the market or expect their adviser to time it for them. In summary, it is up to the clients and adviser to jointly reappraise the situation and to reconfirm capacity for loss and ongoing suitability of investment. This is not the same as versions of the often-asked question “should I move to cash and wait until the situation is clearer”? When the situation is clearer, it will be in the price before most people can move. What is even harder is markets will often buy the rumour and sell the fact, so it is possible to be right about an individual outcome and still lose money.

Dick Dastardly was right to shout to Mutley “do something!” but regarding client investments that should potentially be to reappraise the original answers to the fact-finding questions rather than knee-jerk reactions to run to/from cash.

As for Mr Wilde, again its really all about the situation, if you find yourself in a burning building then doing nothing looks like one of the least sensible options. The difference between the burning building scenario and investing in risk assets, even in these unprecedented times, is the degree of certainty in an outcome and an obvious timeline. There will be, to one degree or another, continuous medical breakthroughs relating to Covid-19. If someone is out of the market when a vaccine or game changing development happens it might make re-entry into the markets particularly hazardous, if not impossible. We know from experience that it will not stop some clients asking if now is a good time to do it, but we must keep moving people back to their long-term investment horizons. This is one of the key benefits of the adviser and the concept of KYC, and one of the reasons why we see such positive adviser feedback from their clients.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested.

Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.