The Outlook

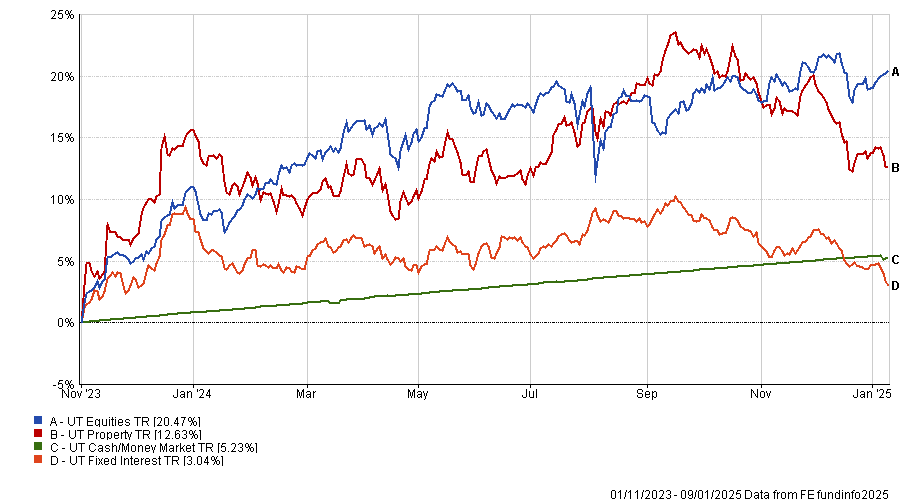

This update covers the period up to January 9th. As usual, we have taken the basic asset class chart (fig.1) back to the end of October 2023, the latest full Powell pivot, where he signalled victory over inflation and strongly suggested rate cuts were coming in 2024.

Asset Class Performance – 01/11/2023 – 12/11/2024

Macro & Markets

The macro backdrop looks positive overall, with global growth expected to slow down only a little coming into 2025. Lacklustre growth in the UK and Europe is likely offset by continued strength from the US. Indeed, Friday’s US employment numbers surprised on the upside, confirming its current strength. As for China, growth should be supported by further stimulus measures.

Inflation is expected to remain subdued in the US, Eurozone and UK. Still, it looks more likely to settle at closer to 3%, rather than the 2% level desired by central banks, due to upward pressure from de-globalisation, an ageing workforce and the tariff plans of President-elect Trump.

That said, inflation should remain low enough to allow interest rates to be cut further, if not by as much as expected when the US Fed first started relaxing policy in September. Rates could be lowered over the coming year by 0.25% – 0.5% in the US and UK and more in the Eurozone, where inflationary pressures and the economy are weaker.

Therefore, this year, continued economic growth and falling interest rates could create a benign backdrop for equity markets. However, nothing is ever quite so simple, and there are a few not-so-insubstantial caveats to this broadly positive picture that are worth mentioning.

Tariffs

First, there is the uncertainty surrounding Trump’s tariff plans. Most likely, his bark will prove worse than his bite. And although tariffs will be hiked, the increases are likely to be significantly smaller than the alarmist numbers touted by Trump. If so, it should be possible to avoid a major trade war, which would undoubtedly be damaging across global markets.

Valuations

Second, global equity valuations are high following the substantial market increases of the last couple of years. High valuations limit the scope for further gains and increase the risk of a significant sell-off up on receipt of any bad news. That said, the overvaluation is confined to the US, with valuations in most other regions still on the low side.

Concentration conundrum

Third, there is the risk posed by the increasing concentration of stocks in global and US equities. The Magnificent Seven now account for as much as 33.5% of the S&P and 21% of the global market. While there is no debate that these companies are “good companies,” investors should be aware that concentration of this magnitude has never been seen before and could pose a significant risk to clients’ portfolios.

Geopolitics

As ever (and particularly with a Trump Presidency), there remains a significant geopolitical risk, and though the uncertainty is currently centred on the Middle East and Ukraine, it is worth highlighting Taiwan and even Greenland and Canada as areas that could heighten geopolitical uncertainty. Whatever happens, it is generally good practice for investors to focus on the factors that have a manageable impact on a client’s investment, which is rarely short-term geopolitical noise.

Performance & Positioning

Most of the IBOSS Core and Passive portfolios outperformed last year, with returns between 5.4% and 11.3% across the various ranges. The outperformance has been most notable in the lower-risk portfolios where fixed-income more acutely affects the performance.

The average fixed-income fund in 2024 (including the first few days in January 2025) netted a negative return of circa -3.5%, but this does not show the whole picture. Throughout 2024, many areas of the fixed-income market remained positive and consolidated some of the gains seen at the end of 2023.

For example, the IBOSS fixed-income allocations netted a positive return of 3% for Core and 2% for Passives. Though these returns admittedly look pretty poor compared to even cash (4.5%), the chart below demonstrates that the fixed-income element of the IBOSS portfolio has delivered strong returns since Powell signalled the potential for future interest rate cuts.

IBOSS Fixed-Income Performance 01.11.2023 – 31.12.2024

Fixed-income aside, it has been equities that contributed most meaningfully to IBOSS portfolios in 2024. So much so that the higher a portfolio’s equity content, the more likely that portfolio is to have outperformed.

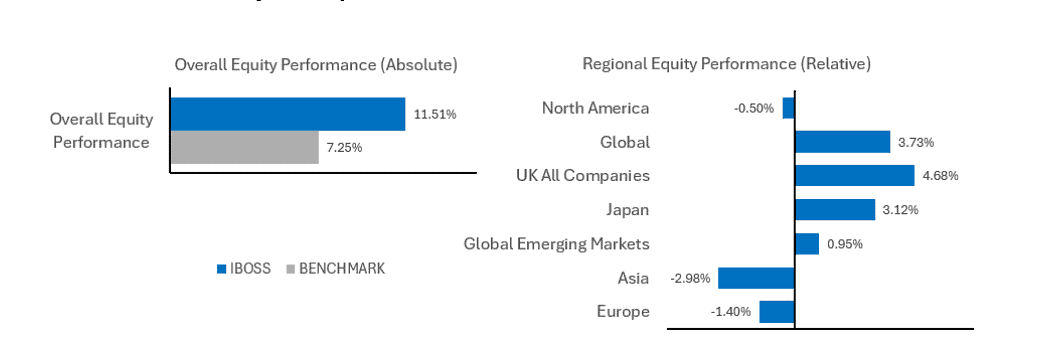

The chart below highlights that the equity portion of Core 4 has outperformed the average equity fund (UT Equities) and each region’s relative outperformance/ underperformance compared to the IA sector, i.e., whether fund selection has contributed or detracted from returns through 2024.

2024 Attribution Analysis – Equities – Core 4

In summary, though US equities led returns last year following the “Trump bump” of early November, the IBOSS portfolios performed well through strong fixed-income returns and positive fund selection across the various equity regions. Where there was some underperformance for IBOSS portfolios, this primarily reflects the net equity allocation rather than any regional/ asset positioning. As always, for more information, please get in touch with a member of the IBOSS team.

Outlook

More than ever, we believe a well-diversified portfolio is crucial. As with our outlook in 2024, there seem to be plenty of areas of opportunity across the world going into 2025. Whilst equities have, understandably, been the focus for many investors, an allocation to areas like commodities, property, infrastructure, cash and fixed-income can provide real returns for clients and offset some of the potentially more risky areas of global equity markets.

Equities

Trump’s victory leaves the US market looking better placed than before; however, the aforementioned concentration of the market could indicate disappointing long-term US returns from here and even the potential for poorer shorter-term returns should there be any sign of disappointment.

Conversely, the lower valuations of other markets mean that it shouldn’t take much good news to see some measure of outperformance. A good example is the 30% bounce we saw in Chinese equities last autumn. Our favoured regions outside the US remain the UK and emerging markets.

The main attraction of the UK is its valuation. The UK has a price-earnings ratio of only 11.2x. This is nearly 20% below the long-term average and way below the US P/E ratio of 22.5x. Although the latest sell-off in gilts is unhelpful, it should not, in our opinion, derail the ongoing, if lacklustre, UK economic recovery. Our other favoured area, emerging markets, comprises of a diverse range of countries. However, as with UK equities, they look relatively cheap and/or have strong growth prospects (as with the US).

Fixed-Income

The latest rise in bond yields has led to renewed capital losses. However, it is worth stressing that bond volatility presents opportunities for managers to make capital returns and to purchase assets generating higher yields than we have seen for many years.

UK gilts and US Treasuries now yield around 4.8%, while UK corporate bonds yield 5.9%. While this doesn’t instantly look super attractive with the UK base rate still at 4.75%, the point is that rate cuts are likely to leave cash returning not much more than 4% or so in a year.

The UK Gilt Market

The latest sell-off in the UK gilt market has led to 10 and 30-year yields touching their highest level since 2008 and 1998, respectively, inevitably prompting some talk of another Liz Truss moment. In reality, this time, it really is quite different in several respects. The recent rise in yields has been more gradual and driven much more by the US than domestic developments, with the gap between UK and US yields having changed little since autumn. Also, while the pound has weakened to $1.22, this is a far cry from the sharp decline to $1.07 seen in September 2022.

All said and done, the backdrop for equities and fixed-income looks reasonably positive. The various risks highlighted above are more likely to create volatility along the way – rather than a sustained sell-off. Even so, to minimise the dangers, a well-diversified portfolio looks more important than ever.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 16.1.24