Complacency is Back

This update covers the period up to September 13th 2024. As usual, we have taken the basic asset class chart (fig.1) back to the end of October last year, the latest full Powell pivot where he signalled victory over inflation and strongly suggested rate cuts were coming, and probably quite a few of them in 2024.

However, markets decided not to bother waiting for any announcements and, at the time of writing, have pretty much priced in a minimum of 25 with a possibility of a 50 basis point cut. This front running has spurred the usual recipients of falling rates, such as small caps, falling bond yields and yet another record high in gold.

UPDATE | We now know that the Fed has cut rates by 50 basis points since this was written, and we will address any potential market fallout from this decision in our Investment Update next month, once the markets have stabilised.

Asset Class Performance Since the Last Powell Pivot > 01/11/2023 – 13/09/2024 (fig.1)*

Macro & Markets

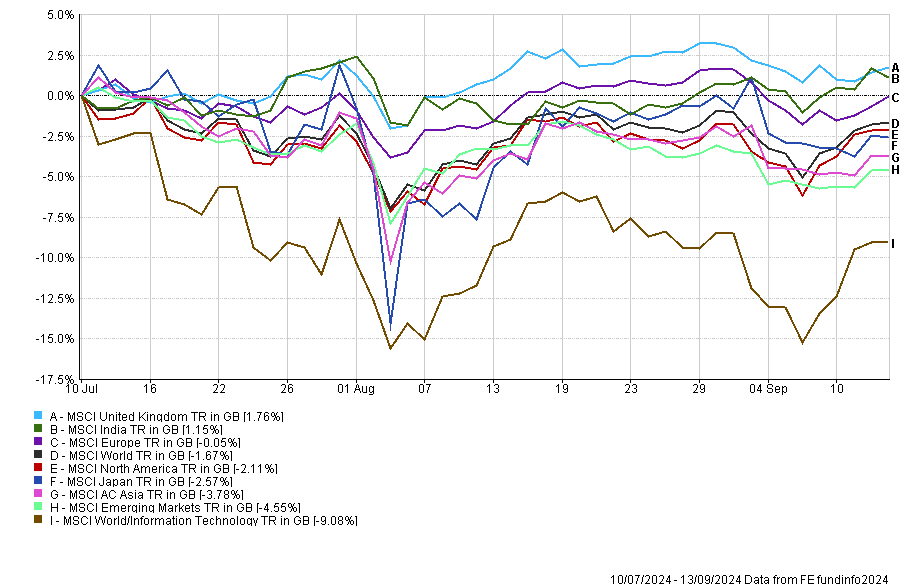

We have seen some rotation away from the tech sector, but the perennial dip buyers have already returned to close the gap with much of the equity world since early September. It is hard to gauge the best conditions for tech to outperform everything else. Pre-pandemic, pandemic, post-pandemic, 0% interest rates, and anticipation of falling rates were all supportive; the only thing that changed was the narrative behind the bullishness. The one undeniably negative factor for tech was the unprecedented rapid-fire rate increases after Powell’s inflation epiphany at the end of 2021. We can safely assume that won’t be repeated, so in theory, everything should be good for tech from here.

There are, however, sizable flies in the ointment. Firstly, valuations remain very high, especially following the AI euphoria, and secondly, those valuations are based on taking most of the positive factors into account while ignoring the potentially negative ones. For example, some potential headwinds include a general economic slowdown, antitrust legislation, and disruptions in the market. No moat is genuinely impregnable, especially in the super-innovative tech sector. We have seen all the Magnificent Seven wobble at some point this year, and on some days, most of them have. The poster child for boundless optimism remains Nvidia. Still, even this stock has seen several significant drawdowns in 2024, and we would suggest that it has yet to face a proper test of its lofty valuation.

Select Geographical Performance Since the Tech Rotation > 10/07/2024 – 13/09/2024 (fig.2)*

Performance & Positioning

Getting paid for Diversification

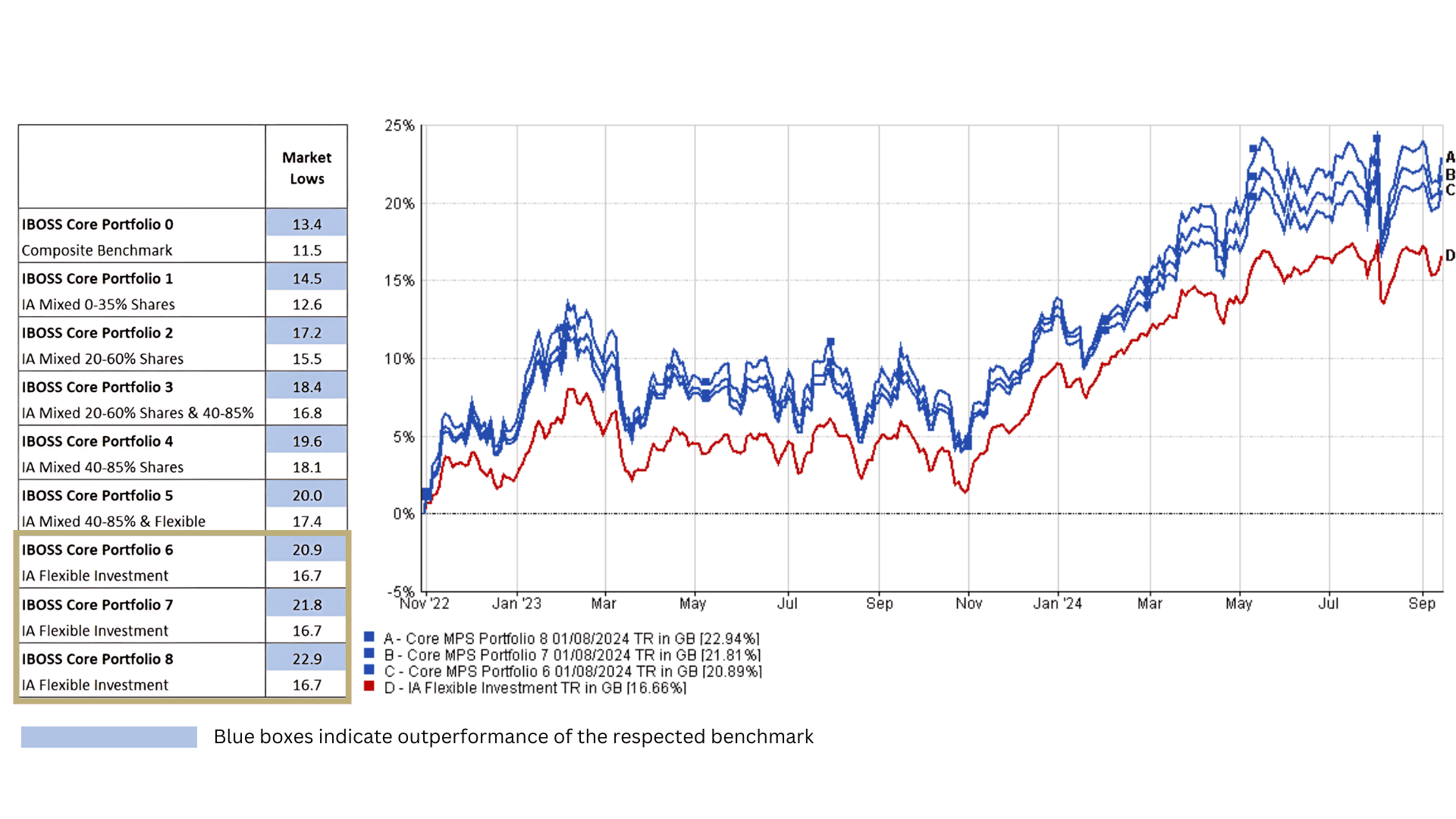

As the chart (fig.1) shows, all the major asset classes remain in ascendance, which is one of the key differences compared to 2022, when bonds and property were getting crushed. The best assets to hold that year were gold and cash, but few investors had significant exposure to either asset class after three solid years for equities.

Investors generally want more of what has worked over recent history or, even better, more of what is working right now. Our job is to overweight assets with the best risk-return profile (whether through active or passive funds) and underweight those expensive areas where the investment case is not based on fundamentals, but rather on hype or the flawed notion that there is no alternative (TINA).

Fortunately, since the market lows of October 2022, we have been in a period where investors have been rewarded for higher levels of diversification. While this is welcome news for an asset management team that speaks ad nauseam about diversification, our investors are the real beneficiaries, as they are not taking excessive concentration risk to achieve returns. This is particularly true for our higher-risk portfolios, where the last 20 months have been our best period of outperformance for portfolios 6, 7, and 8 since 2017. These portfolios have a much broader geographical spread of assets compared to many peers who cluster around a 50% US large-cap equity weighting. Interestingly, the highest-risk benchmark (IA Flexible) underperformed all IBOSS portfolios across all ranges through August.

Strong Returns Since the Market Lows | IBOSS Core Portfolios > 31/10/2022 – 13/09/2024 (fig.3)*

Outlook

Overall, we remain positive on all the major asset classes. However, it must be acknowledged that prices in equities remain high, particularly in the US. Additionally, bonds, property, and gold have considerably re-rated to the upside.

In the coming months, we will have the UK budget, and despite the soothing words from Labour ahead of the general election, there is genuine concern that tax changes could be introduced that would be detrimental to a wide variety of businesses and, consequently, investors.

It has not escaped anyone’s notice that we also have a US election on the horizon. No one on either side seems willing to address the uncomfortable issues of spiraling debt, although these should be at the forefront of discussions on spending rather than endless soundbites aimed at easy wins with voters. We do not rule out a “Truss moment” for the US, where the bond markets say “enough is enough,” prompting the necessary debate about what is truly affordable.

The day of reckoning for debt burdens on either side of the pond is uncertain, but other countries will closely watch the UK budget outcome to see how it impacts the bond market. Just as in 1997, when then Chancellor Gordon Brown effectively raided pension schemes by abolishing advanced corporation tax relief in his first year, it may again make political sense to maximise tax revenue in a first-year budget. It is not our role to comment on the fairness of government actions, but it is reasonable to note that more advisers are expressing concerns about this budget than any previous one in our nearly 16-year history.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 186.9.24