Following the worst year in history for bonds and a challenging environment for many stocks and shares, investors saw some much-needed relief in the final quarter of last year. Globally, bonds and equities, on average, rallied from their October lows by 12% and 6%, respectively and investors were finally rewarded for holding a more diverse range of assets.

Cooling Inflation Expectations

Throughout 2022, the inflation outlook and central bank reaction function remained the key factors driving asset prices. Inflation reflects the rate cost of goods and services rise, and ever-higher inflation expectations weighed heavily on markets throughout the majority of 2022. However, these expectations began to cool in September of last year, and market participants reacted positively to the news that the top may well be in and, therefore, potential interest rate rises may be lessened from here.

Though this is undoubtedly good news, it is worth noting that lower-than-expected inflation does not mean that the prices of goods and services will collapse, but instead, they will rise less aggressively than they have more recently. This means that the previous price rises remain in the system, which will likely keep concerns elevated as companies, governments, and individuals get to grips with the new reality.

American Exceptionalism and Currency

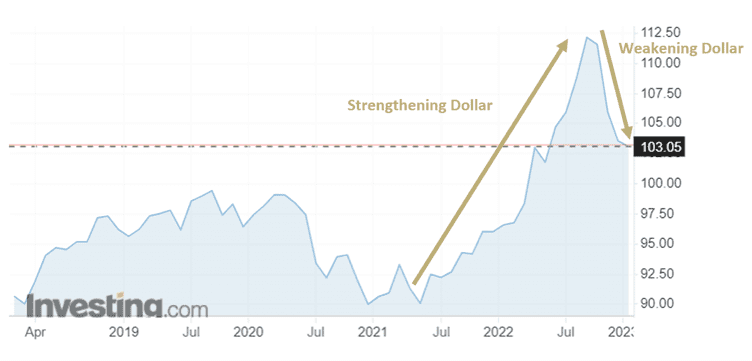

In previous market summaries, we discussed the cushioning effects of a weaker pound on investors’ portfolios and how a strong dollar had offset the underperformance of American stocks last year. However, we have seen a reversal of this trend since September, as the dollar began to weaken against a basket of other currencies (figure 1). The weakening dollar has significantly affected US returns for UK investors like ourselves. For example, US stocks (MSCI North America) have risen by 10.57% since October, but a sterling investor would have seen a return of only 1.97% due to the weakening dollar. Though this has been negative for investments in the US, it has been positive for a broader range of equity markets. For example, an allocation to Europe, the UK, Emerging Markets and Chinese equities have contributed more positively to performance.

At inflection points like these, diversification within your portfolio is essential. A diverse range of geographical assets mitigates risk and helps maintain the opportunity set, as no market conditions persist indefinitely. The rear-view mirror remains one of the most significant risks for investors and any geography or investment style can go through prolonged periods of underperformance just as they can experience prolonged periods of outperformance.

Figure 1: US Dollar Index – 5 Years

China Reopening

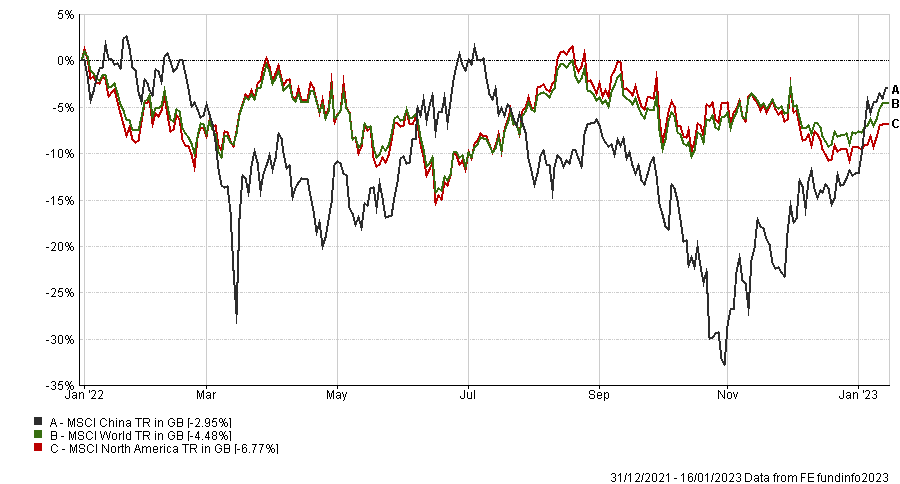

One area that has seen perhaps the most significant change in fortunes is Chinese equities which seemed to reach their nadir at the end of October last year (down 33% at worst). Since then, and alongside the weakening dollar, the Chinese Government have indicated that the end of their zero-covid policy has arrived. Markets responded favourably to this news, and in a couple of months, we saw Chinese shares bounce 43%, erasing much of the losses of last year in spectacularly short order. In fact, Chinese equities (at the time of writing) have performed better than US equities and Global equities from the start of last year (figure 2).

Figure 2: Equity Performance – 31.12.2021 – 16.01.2022*

Fixed Income

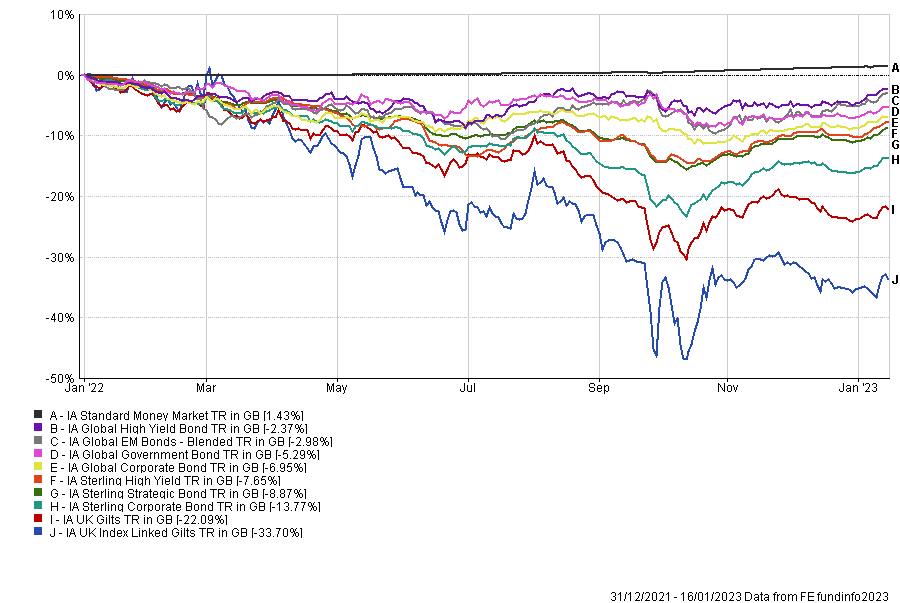

Last year we looked to keep our bond position relatively defensive. We held short-dated bonds (which have less interest rate sensitivity) and more cash. This helped protect the portfolios in a year where the most significant risk to client valuations was being overly exposed to bonds with high-interest rate sensitivity.

Figure 3: Fixed Income Performance – 31.12.2021 – 16.01.2022*

However, the situation is different now than at the start of 2022. Fixed income assets are trading at much higher yields and more attractive valuations than they have for several years. We have seen a rebound since October (figure 3), with index-linked gilts and gilts up circa 25% and 12%, respectively, but we would expect continued volatility and uncertainty from here. As such, we aim to be relatively defensively positioned whilst leveraging the expertise of managers’ with a more flexible remit. We have therefore broadened the regional exposure to more global bonds and increased our duration (interest-rate sensitivity) at the back end of last year and into this year. We will not, however, be looking to take on more exposure to high- yield (junk credit) at this stage as we expect default rates could pick up from here.

It is worth noting that last year’s market difficulties will present opportunities for investors despite the ongoing period of asset price readjustment we find ourselves in. Therefore, we feel it is more important than ever to remain calm, diversified and open to opportunities wherever they may present themselves, whether in bond markets, equity markets, commodities or infrastructure.

Final Thought: Inefficient frontiers and confusing outcomes

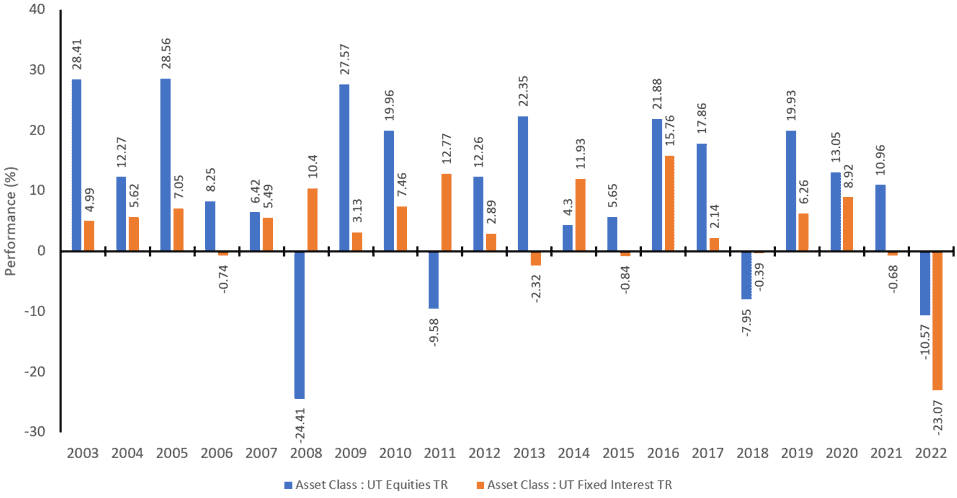

In various market updates, we have highlighted the difficulties lower-risk portfolios had last year as bonds sold off almost twice as much as equities (figure 4).

Figure 4: Discrete Calendar Year – Bond and Equity Performance

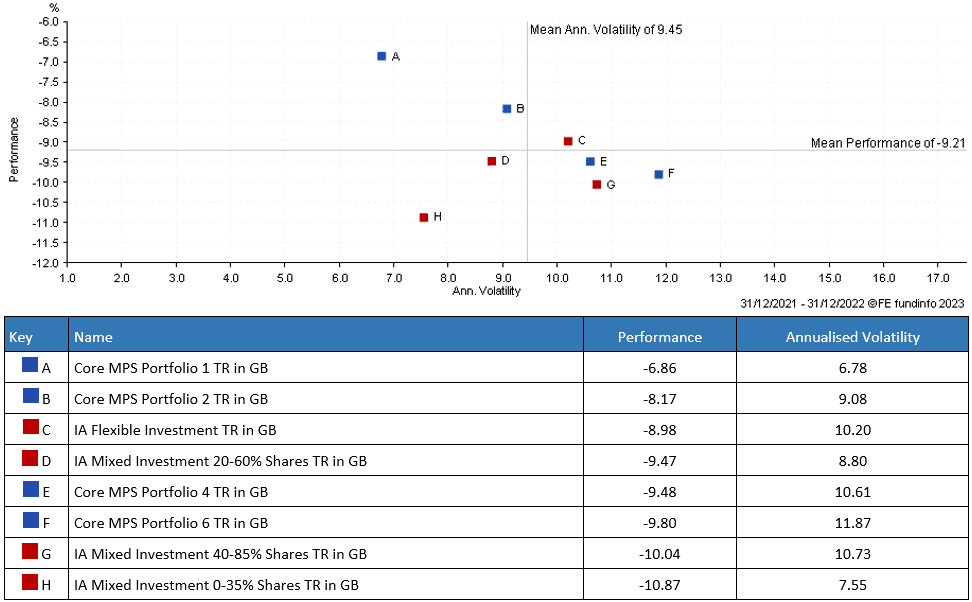

In this environment, we saw the benchmark, and many of our peers’ lower-risk products fall further than their respective high-risk portfolios into a falling market. Fortunately, our portfolios have maintained the credentials you would expect – i.e. the low-risk portfolios have lost the least, and the higher-risk portfolios have lost the most (figure 5). Interestingly, and since the dollar has rallied, some of the peer group has exhibited similarly confusing outcomes in the market bounce. We have seen their low-risk portfolios participate more into a rising market than their high-risk portfolios. Mainly due to their concentrated dollar/ US positioning. On the other hand, our portfolios have performed as expected whereby our higher-risk portfolios have rallied further than our lower-risk portfolios in a rising market.

Figure 5: 1 Year Scatter – MPS Core Portfolios*

*Information displayed is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 24.1.23