Since mid-July this year, the property sector has experienced one of its strongest recoveries since the pandemic, delivering a notable upswing just as global equity markets faced a sell-off. This rebound has underscored the diversification benefits that property can bring to a portfolio, providing stability during periods of equity market volatility. IBOSS was significantly underweight in property throughout 2022 and 2023, but February 2024 marked what we identified as an attractive entry point.

Our decision earlier in the year has made us well-placed to benefit from the recent rally but what are the driving factors behind this resurgence, and with interest in the sector returning will property’s renewed strength continue to add value as part of a balanced investment strategy?

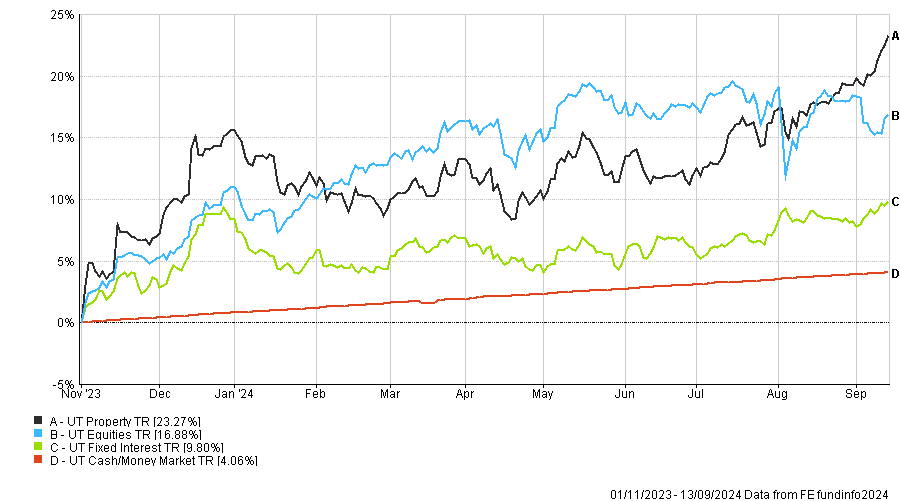

Asset Class Performance > 01/11/2023 – 13/09/2024

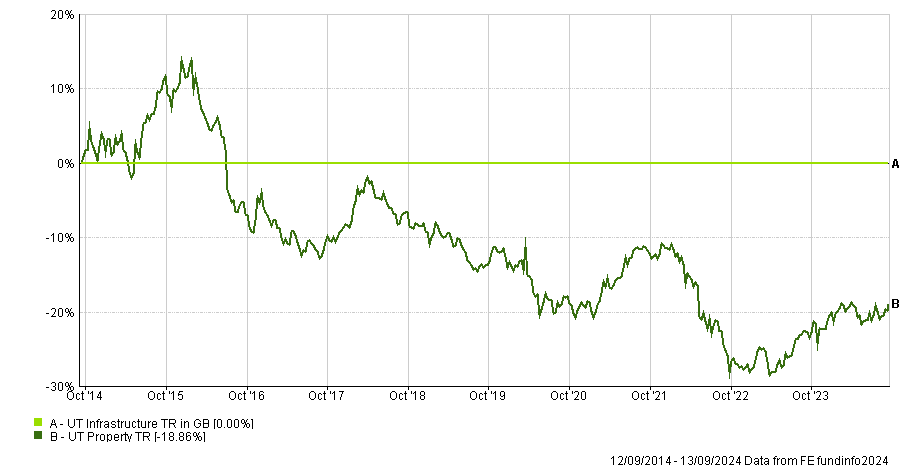

Comparing Infrastructure and Property

From September 2015 to October 2022, the infrastructure sector consistently outperformed the property sector. For most of that period, our exposure to infrastructure was through broader sectors such as the IA Global category.

UT Infrastructure versus UT Property – Relative Performance Line Chart

However, in early 2020, we made a rare adjustment to our core asset allocation, redefining ‘property’ to include dedicated infrastructure funds. This was in addition to the existing allocation through broader funds.

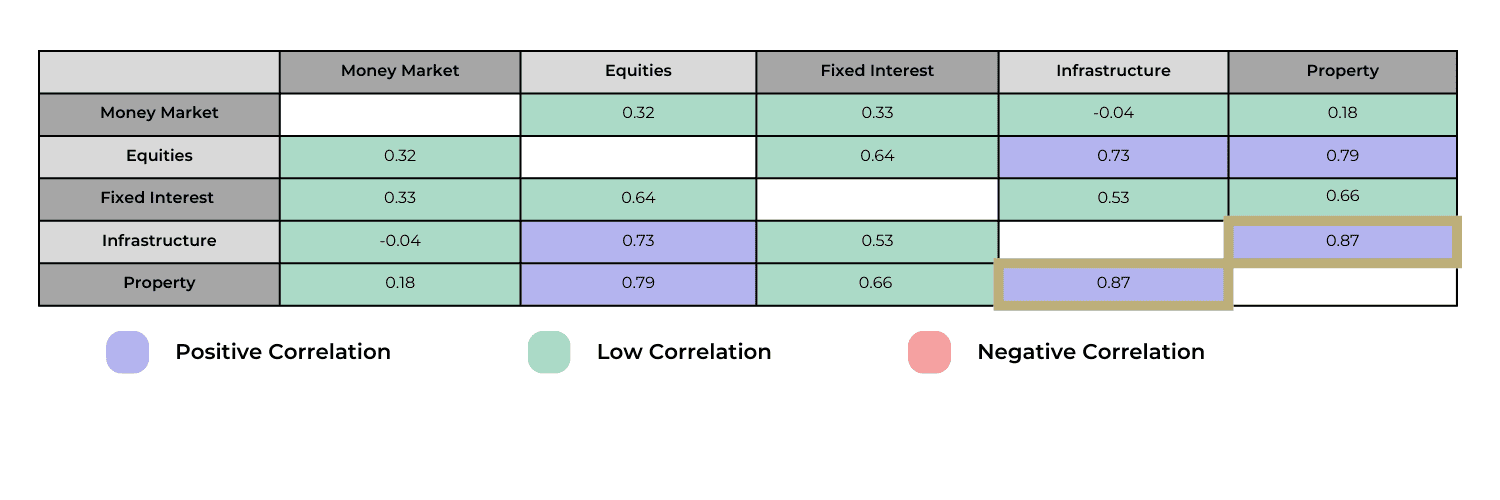

Over various periods, these two sectors generally move in tandem, but they can diverge significantly, especially in the short term. The three-year correlation between them stands at 0.87, which is higher than any other asset class correlation.

3-Year Correlation Table > 31/08/2021 to 31/08/2024

Shifting View on the Property Sector

Our view on the property sector has shifted due to several factors. Property values have suffered significantly from the negative post-pandemic landscape, compounded by the fastest and steepest rise in interest rates in a generation. Almost every factor was a headwind for property during this time. Even before the pandemic, retail had been under pressure for years, with online shopping continuing to gain an increasing share of the market.

Every asset class eventually reaches a point where almost all the bad news is priced in. While market timing is notoriously difficult, we’ve often found that assets with a sound structural risk/return profile can be rewarding with patience. However, patience is rare in today’s markets, where investors typically chase whatever is performing well. The longer an asset performs strongly, the more investors are inclined to buy more of it. Currently, large US growth stocks remain the preferred asset class, with significant allocations from retail investors and asset managers alike, many seemingly indifferent to price. In contrast, property has been in the opposite position, underperforming and continuing in a selling cycle until recently.

Interest Rates: A Key Headwind for Property

The primary headwind for the property sector has been the rapid and steep rise in global interest rates. Central banks misjudged inflation throughout 2021 and spent the following two years playing catch-up, eventually admitting they didn’t fully understand how inflation manifests. Despite this reluctant and somewhat unnerving mea culpa, the world and his dog still hang on every word from the central banks. Most recently, the Fed cut rates by 50 basis points—a move that had been the subject of much debate. However, it’s not the individual rate cut that matters, but rather the broader direction of interest rates and any significant shifts in economic data trends.

Cautious but Opportunistic Approach

We remain acutely aware of the ongoing risks to both the property and infrastructure sectors. Our decision to increase allocations is not based on a strong bullish view, but rather reflects an improved risk/return profile, leaving us less bearish. One reason for our continued caution on assets benefiting from lower interest rates is our concern that inflation could return, possibly as early as the second half of 2025.

In terms of how we are positioning within the property sector, the IBOSS Core medium risk portfolio now has a 6% allocation to property, and we expect to increase that to 7% in the coming months. We’ve also recently shifted towards using more active funds; almost two thirds (63%) of active global property managers have beaten their benchmarks over the past five years, and there are not many sectors where you can say that.

Specifically, the active funds we currently use are Schroder Global Cities and CT Global Real Estate Securities. These funds have different geographical focuses, and current conditions should favour talented active management. We chose Schroders’ due to their extensive resources, experience and pedigree in property, as well as the fund’s consistently strong track record. Meanwhile, CT Global Real Estate Securities has a reasonable allocation to Asian markets, whereas many property funds focus solely on developed markets. The Asia portion of the fund is managed passively, whereas the European and North American segments are actively managed by the experienced Marcus Phayre-Mudge. Combining passive and active approaches within one fund provides broad and diverse market coverage in a sector where maintaining sufficiently diversified assets can be more challenging.

Inflection points like the one we are experiencing often present opportunities to search out alpha, but as always, we will closely monitor performance in this competitive environment. Given the current market dynamics and the historical resilience of property, we see continued growth potential in the property sector and are optimistic about its role in a diversified investment strategy going forwards, especially in times of market uncertainty.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 188.9.24