- Global growth has held up better than expected in the face of Trump’s large tariff hikes and should continue to be supported this coming year by declining interest rates and fiscal stimulus.

- Interest rates are likely to be lowered another 0.5% or so in both the US and UK next year as monetary policy is returned to a neutral setting. Sticky inflation is likely to prevent more aggressive easing.

- The broadly positive macro backdrop means equities should see further gains over the coming year with the greatest upside outside the US where valuations are not excessively high.

- Bonds continue to look quite attractive although capital values may be volatile due to background fiscal worries and uncertainty over the extent of forthcoming rate cuts.

The Year Past:

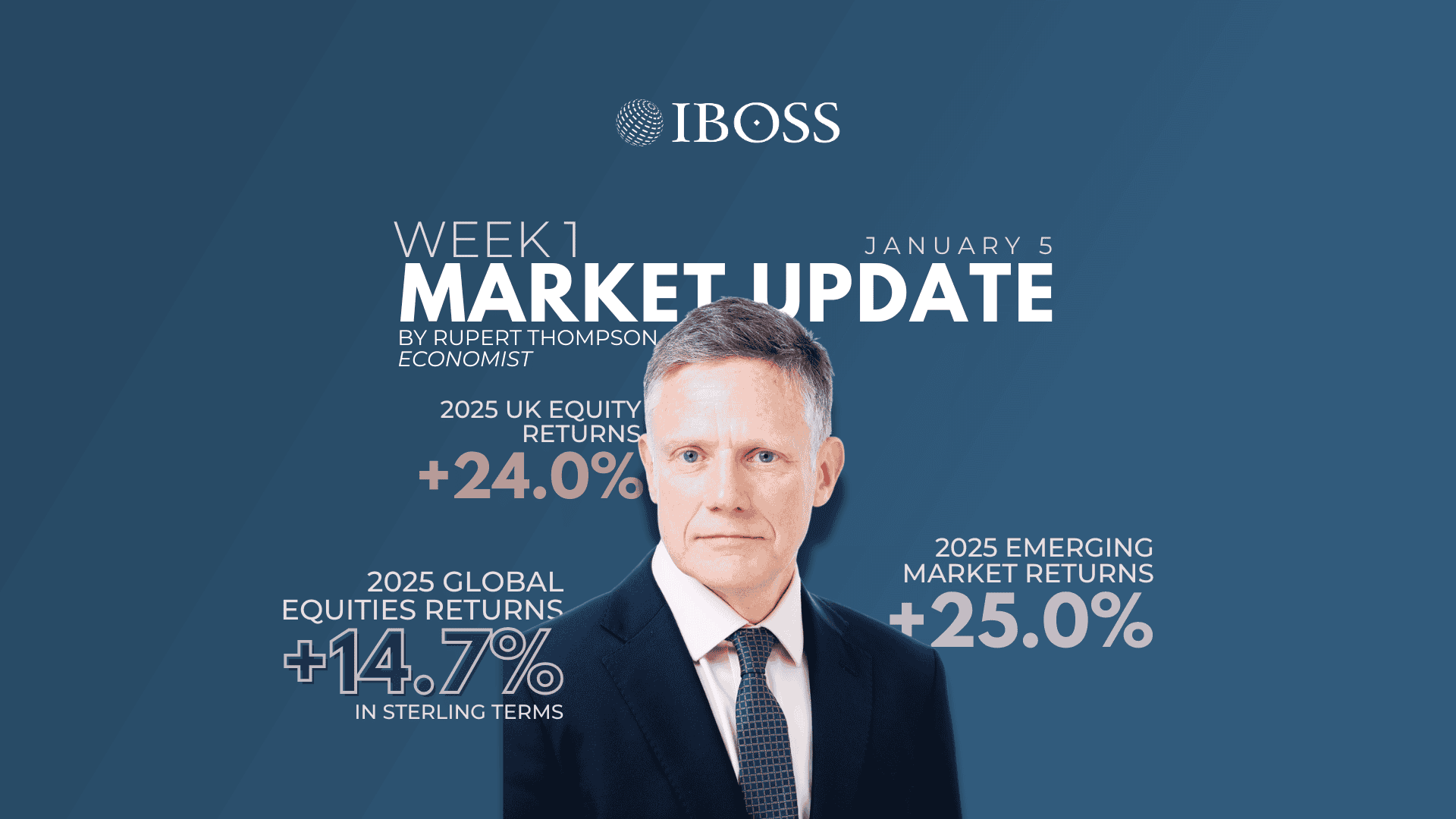

2025 saw global equities perform strongly, returning around 20% in local currency terms for the third year running. In sterling terms, the return was a somewhat smaller 14.7% as the pound strengthened 7.4% against a weak dollar.

The year, however, was far from smooth sailing. A combination of worries related to the DeepSeek news in January and the massive tariff hikes announced by Trump on Liberation Day meant global markets in April were down as much as 15-20% from their February high.

But this was followed by a swift rebound. Trump backed down from his wilder tariff threats – the infamous TACO trade – and the US economy held up considerably better than expected in the face of the policy turmoil. The Magnificent Seven, led by Nvidia, also continued to produce stellar results although later in the year worries emerged of an AI-related bubble. Last and far from least, the US Fed started lowering interest rates again in September.

US equities underperformed considerably, particularly in sterling terms with the US returning only 9.1% versus 23.5% for the rest of the world. US performance suffered from the fall in the dollar resulting from the policy chaos in Washington. Investors also grew wary of the risks posed by the ever larger proportion of the US market accounted for by the Magnificent Seven, which ended up returning 12.2% over the year in sterling terms.

Other markets also benefited from having considerably cheaper valuations than the US. The UK, Europe and Emerging markets all saw very strong returns of 24.0%, 27.9% and 25.0% respectively in sterling terms. Japan lagged a little with a return of 17.4%.

Fixed income also had a reasonably good year in most cases. US Treasuries returned 6.3% on the back of hopes of renewed Fed easing. UK gilts also ended up returning a decent 5.0% despite the outbreak of fiscal worries along the way. Elsewhere, returns varied substantially with Emerging market bonds returning as much as 15% while German and Japanese government bonds saw negative returns. Meanwhile, UK and US corporate bonds both saw returns of around 7.5%.

As for commodities, gold was the stellar performer for the second year running. It returned 53% in sterling terms on the back of continued heavy buying by central banks as they sought to diversify their foreign exchange reserves away from the dollar. Bitcoin by contrast, despite the US Administration’s best efforts, ended the year down 15%.

The Year Ahead:

After three consecutive years of strong returns, equity valuations are not surprisingly now on the high side and return prospects somewhat constrained as a result. The current price-earnings ratio for global equities of 19.1x is some 20% above the long-term average.

Even so, global markets still look quite well placed to see another double digit return this coming year as the economic backdrop remains positive. Growth looks set to continue at a respectable level, supported by continued policy stimulus, setting the scene for gains in corporate earnings to drive further market increases.

Interest rates will continue to be reduced in the US, particularly with the Federal Reserve set to be led by a new Trump-appointed Chair from May. Even if inflation remains significantly above target as we expect, the Fed looks set to put more weight on the recent rise in unemployment and lower rates in line with Trump’s wishes.

Falling US rates have historically provided a favourable backdrop for equity markets. Indeed, the large gains seen since the Fed started cutting rates in September 2024 are bang in line with what history would have predicted.

UK rates are also likely to be cut another 0.5% or so by the summer as inflation pressures recede. These moves will take US and UK rates down close to a neutral level which is where Eurozone rates already are and why the European Central Bank is now on hold.

Fiscal policy should also support global growth. Trump’s big beautiful bill will provide a boost to the US in the first half of the year and the German and Chinese economies should also see some fiscal stimulus. The exception here is the UK where policy is being tightened and growth should remain relatively weak as a result.

While the positive macro backdrop is the main reason we don’t see the current high valuations preventing further market gains, the other reason is that the valuation excess is only acute in the US. Valuations here are some 35% above their long-term average versus 15% or so for both Europe and Emerging markets and only 5-10% for the UK.

This valuation gap is a key reason why we believe other markets have more potential upside than the US and any equity exposure should be well diversified across regions. The other big factor here is the danger posed by the dominance of the Magnificent Seven which now account for as much as one-third of the total market capitalisation of the main US equity index.

This brings us onto the burning question of whether we are in the midst of an AI-related bubble now in danger of bursting. Our view is that it is simply too early to know whether the massive spending on data centres will prove justified, to what extent AI will bring about a sizeable productivity boost and be adopted by companies more generally, and who will be the ultimate winners in the AI-race.

The experience of previous technological revolutions, along with current high valuation levels, the circularity of recent AI-related deals and the massive capex spend, are definitely flashing some warning signs. However, the lesson of the past is that bubbles can continue to inflate for some time and it can be dangerous to bail out too early. The more prudent course of action to our mind is to retain some exposure to this area but keep it significantly less than the excessive exposure now obtained by a passive global equity tracker.

Diversification away from the Magnificent Seven is a big argument for having a sizeable allocation outside the US. Strong gains recently in Korea, Taiwan and China have been led by their tech sectors and highlight that the Magnificent Seven are not the only way of playing the AI-boom.

The last factor arguing for favouring other markets over the US is the dollar. We expect it to decline further over the coming year, dragged down by US rate cuts, its overvaluation and the continuing desire by investors to reduce their exposure to the whims of the Trump Administration.

Although our base case is that equities see another year of good returns, there are undoubtedly significant risks to this relatively rosy outlook. An early end to the AI boom is clearly one such risk. Another is that inflation fails to head back towards target, making the forthcoming monetary and fiscal stimulus inappropriate and causing market angst. Finally, there is the all too obvious geopolitical risk. This has only been increased by Trump’s escapade over the weekend in Venezuela with its possible implications for further interventions of this kind by the US, China and Russia.

These risks mean a well-diversified portfolio looks more essential than ever. And diversification means not just diversifying within equities but also having some exposure to other asset classes.

UK Gilts and US Treasuries are overall currently yielding a respectable 4.7% and 4.4% respectively and look likely to deliver returns of 4.5-5% over the coming year. The tailwind coming from further rate cuts should offset any upward pressure from renewed worries on the fiscal front.

Investment grade corporate bonds, meanwhile, yield close to 1% more than government bonds. Although this additional yield is low by historical standards and does not offer that much compensation for the increased risk, there is no obvious reason given the favourable macro backdrop for it to widen significantly, undermining returns in the process.

Fixed income offers not just a respectable yield, particularly now cash is yielding rather less, but also a potential offset to the risk of a fall in equity markets as long as it were not caused by an upturn in inflation worries.

Finally, there is gold. An allocation to gold or gold miners has more than proven its worth over the last year. And with central banks very likely to continue their drive to reduce their exposure to the dollar, it looks well placed to see further gains over the medium term. Gold’s low correlation to equities remains a key attraction.

In short, we believe equities look reasonably well placed to have another good year. But there are significant risks and just as a well-diversified portfolio paid off handsomely last year – both reducing risk and boosting returns – we expect it to do the same this coming year.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 10.1.26