Once again the US/Iran war continued to dominate the front pages, and the thoughts of investors, with any hope of a quick end to the war fading as both sides continued to escalate their attacks on infrastructure: Iran struck the Ras Laffan gas complex in Quatar, President Trump responded by threatening to blow up Iran’s South Pars gas field if it attacked Quatar again.

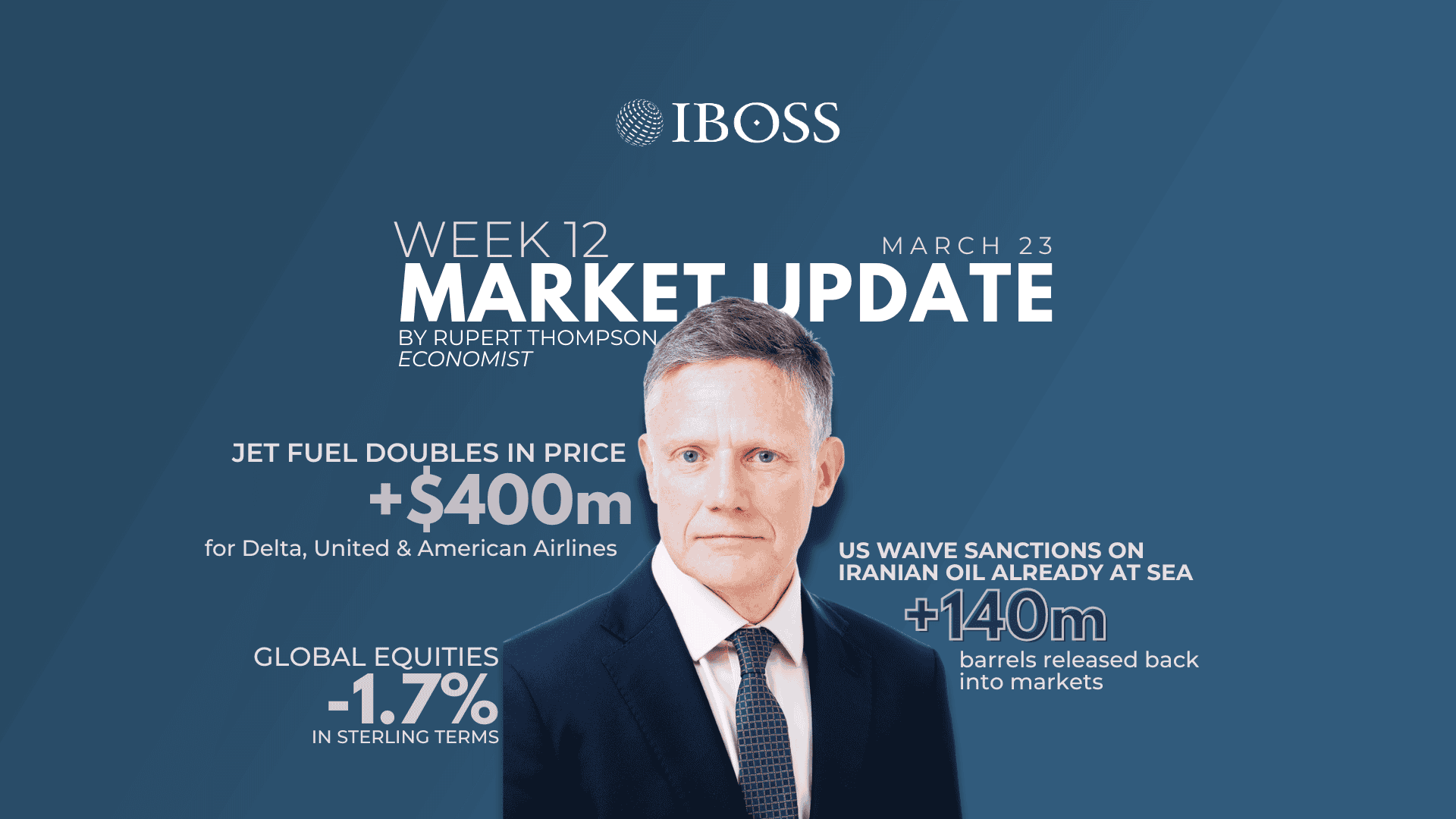

The Strait of Hormuz also remained in focus, with Nato allies holding out on sending ships to provide cover for safe passage. The US administration waived sanctions on the purchase of Iranian oil that is already at sea. This should release around 140 million barrels back into the market – one and a half days of global supply. However, global liquid natural gas supplies from the middle east are set to halt within 10 days as those ships already at sea dock. On Sunday Donald Trump issued a 48 hour ultimatum to open the Strait – this has not been accepted.

Perhaps surprisingly, despite the amount of airspace that is closed, jet fuel has doubled in price since the start of the war – adding $400 million to the costs of the largest three US operators – Delta, United and American Airlines.

Against this backdrop, both global equities and bonds traded down. Global markets fell by 1.7% in local currency and in sterling. In the UK gilt markets also fell back with the ten-year now offering a yield of 5.1% and the US equivalent sliding to 4.44%.

It was a busy week for central banks with meetings for the Bank of England (BOE), the US Federal Reserve (FED), Bank of Japan (BOJ) and the European Central Bank (ECB). As expected, all held rates at their current levels. Whilst the ECB had in all likelihood reached its’ terminal rate (as low as it was likely to go based on the current economic backdrop) the BOE and the FED were both expected to continue to cut rates as recently as February this year.

Whilst there remains an expectation that the FED have at least one more cut penciled in for this year, closer to home the BOE are now seen as more likely to raise rates multiple times rather than cut, the direction of travel for Japan is also up, although this is from the relatively low 0.75%

The primary driver to the change of direction remains inflation. Having seen significant falls post the exit of Covid restrictions, the sharp increase in oil and gas prices will place significant upward pressure on inflation. The question for central banks will be whether to focus on growth, which is trending down or inflation which is trending up.

In good news employment numbers in the US came in better than expected as did the Philadelphia Manufacturing Index – a closely watched bellwether. However, new home sales in the US continued to weaken.

The one surprise of the week was the uncharacteristically weak performance of gold. Typically one would expect the yellow metal to perform well in times of heightened geopolitical tension, although not this week. It is likely that short-term issues such as the ability to transport and the fact that performance was so strong leading up to the war along with the expectation of an increase in interest rates have combined to give traders reason to pause for the time being.

Whilst we usually focus on the previous week it would seem odd not to comment on the market moves this morning considering they are more significant than we would normally see. Having woken up to significant falls in markets across Asia, followed by the UK and Europe at the open, post the ultimatum from the White House, any immediate action has now been postponed with talks held for a “complete and total resolution of hostilities”. For the time being, a salutary reminder that significant swings in markets should not encourage a swift change of view.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 93.3.26