Considering the tax year end, recent market volatility, and following our Ask the Managers webinar (Watch on Demand), Investment Analysts Kate Townsend and Jack Roberts discuss the key talking points, answering your questions on portfolios, markets, and outlook.

What would a prolonged conflict mean for markets and prospective returns for clients?

A prolonged conflict and equity markets re-rating to the downside would ultimately create longer term return opportunities, as most assets besides oil could become cheaper, improving entry points for both new and existing investors. Active managers can take advantage of oversold areas, while dynamically managed passive portfolios could also benefit from lower starting valuations. Remaining invested can ensure that clients participate in these opportunities. There is always the temptation of moving to cash especially for more nervous investors. While moving to cash can bring immediate peace of mind of investors in the very short term, the much harder thing to do is time your re-entry into risk assets.

Following on from that question, have any of the events surrounding the Iran conflict affected your long term thinking for portfolio construction and how the components fit together?

No – our long term views remain the same, including expectations for a weakening dollar, higher commodity prices, and the continued importance of greater geographical diversification. The conflict reinforces the importance of existing themes such as energy security, diversified supply chains and broader global opportunities beyond the US. It also provides a valuable stress test for ensuring each fund continues to behave as expected and can a shine a light on any unintended concentration risks.

Higher oil prices suggest fewer rate cuts and more persistent inflation, does that change your views on Real Estate and Infrastructure?

Not meaningfully. They may add short term pressure, but the long term opportunity in infrastructure and real assets remains strong given years of underinvestment and structural tailwinds. The risk return profile at current entry points compared to many other investment areas overcomes the rising interest rate scenario. The key is maintaining diversification within these sectors rather than relying on a single theme or policy outcome to dictate portfolio construction.

Since the beginning of the market falls, the dollar has acted as a safe haven, have recent events changed your views on the outlook for the dollar?

No, in fact the opposite is the case. Our overall expectation is still for a weaker dollar over time. Although the dollar has historically often behaved as a safe haven during geo-political shocks, its recent moves have been modest and global uncertainty around US policy has already led to a significant amount of hedging in response. The dollar remains the worlds reserve currency, but the key takeaway from recent events is no single diversifying asset works consistently in every environment, you need a range of diversifying assets within a portfolio.

The “Magnificent 7” seem less talked about recently, what’s changed?

The Mag 7 stocks performance has reversed this year and after years of strong returns, most of them underperformed the broader US market in 2025, and this year all seven have lagged again, with the group collectively down almost double digits. This shift highlights the risks of concentrated exposures, particularly for investors holding broad US or global trackers dominated by these names.

It would seem remiss of us to not revisit one of investing’s perennial questions, is now the time for active management to outperform?

The Core MPS portfolios have increased their allocation to active funds as active managers have been outperforming since the return of Donald Trump to the Whitehouse. Although passive funds have held up slightly better since the Middle East conflict began, our team has no style bias while noting that many passive indices remain incredibly concentrated. With active and passive funds results oscillating wildly in recent years and each style having periods of outperformance, many advisers have opted for our Blended MPS solution as a more balanced middle ground.

How is fixed income looking? We’ve seen gilts in particular sell off, should lower risk investors be concerned, as in 2022?

Fixed income has broadly behaved as expected in the recent drawdown, holding up better than equities, but less so than cash.

While gilts have come under pressure and yields have risen, this has been relatively orderly in comparison to the infamous UK mini-budget, when markets faced a systemic shock and necessary intervention from the Bank of England. That said the IBOSS portfolios have remained underweight gilts relative to their respective benchmarks for some time.

Yields are now meaningfully higher, which improves income and longer-term return prospects. However, we remain selective, favouring flexible, strategic bond managers and maintaining caution in higher-yielding areas where risks may not be fully priced and are watchful of Private Credit issues bleeding across into the more liquid, traditional areas of the credit market.

There seemed to be a looming fear around Private Credit markets until the Iran story started taking all the headlines. We have however, seen some funds gate, do IBOSS have exposure to these types of fund?

IBOSS do not have explicit exposure to private credit funds and do not currently intend to allocate to this area. Our approach prioritises more liquid asset classes, and we do not believe any additional yield sufficiently compensates for the associated liquidity risks.

While recent headlines have shifted focus, concerns in private credit have not disappeared, particularly given some funds restricting redemptions. We continue to monitor the area closely, as stress in less liquid parts of the market can, at times, spill over into broader bond and equity markets.

What changes are you making to portfolios in response to the recent market pullback?

At the beginning of February, all IBOSS portfolios were rebalanced back to target allocations following a strong start to 2026. This ensured that no positions had drifted too high and allowed us to lock in gains in an orderly way. This rebalance was particularly beneficial for our gold mining fund which had experienced stellar returns. We also introduced an allocation to short-dated bonds to help manage interest rate sensitivity and enhance portfolio resilience to the falling interest rate narrative proving incorrect.

Looking ahead to our May rebalance, the focus is less on major allocation changes and more on ensuring we have the right combination of funds working effectively together in the current environment, particularly given ongoing market volatility.

Should clients be delaying investments in the current environment?

In short, no, delaying investment on grounds of obtaining a better entry point is not a strategy we would endorse. However, the specific client situation and the outcomes of conversations with their adviser should be the driving factors dictating an investment strategy. Periods of market volatility can often create more attractive entry points, as asset prices adjust and valuations improve relative to recent history.

For clients with a medium to long-term horizon (5 -10 years or more), market fluctuations will be a normal part of investing. Trying to time entry points can be difficult, and staying invested is often more important than waiting for the “right” moment. You can read more in our latest update on market volatility and investment horizons here.

For new clients, how can they invest more safely, for example using pound-cost averaging?

For new clients, staying invested over the long term remains the most effective approach, but we recognise that market volatility can feel unsettling.

One option to help manage this is pound-cost averaging. In simple terms, this involves gradually investing into the market in regular tranches rather than all at once. This approach removes the need to “time the market” perfectly and, over time, averages out the prices at which assets are purchased, helping to reduce the impact of short-term swings.

So, we have an uneasy peace currently in the Iran conflict, potential trouble brewing private markets, worries over AI and whether its going to be a repeat of the .com crash and/or take all our jobs and collapse the economy and the midterms in November. What is it that keeps you awake most at night right now?

It’s true – there are plenty of reasons to feel uneasy right now, from geopolitical tensions to market uncertainties and technological disruption. That said, our focus remains on robust portfolio construction, rather than trying to predict the outcomes-based headlines, Tweets, ‘Truths’ or short-term shocks.

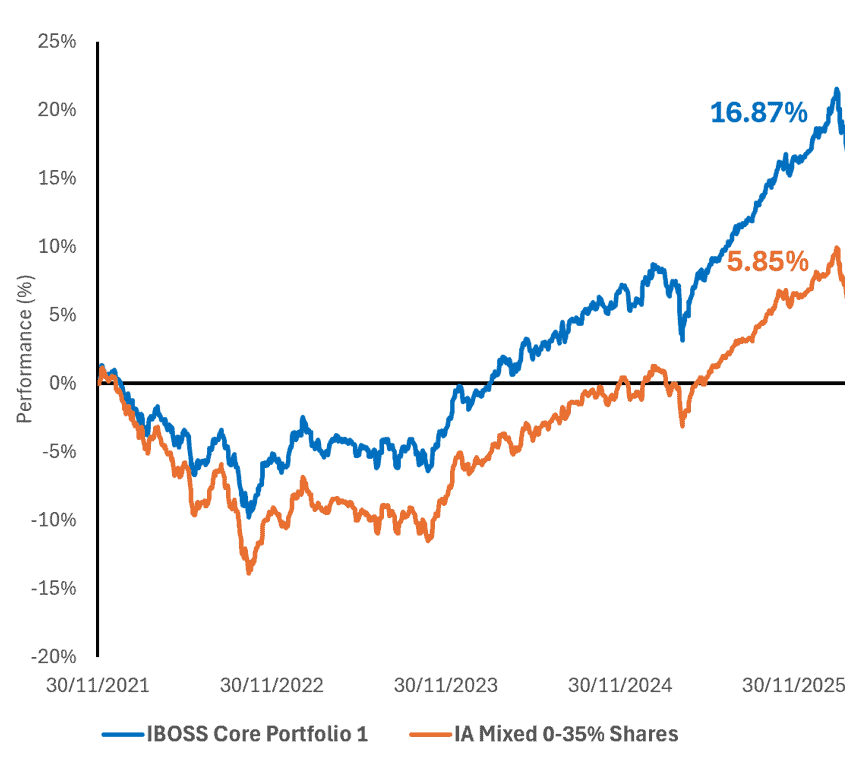

History gives us reassurance here. A clear example is the IBOSS Core MPS 1 fixed income positioning in 2022, the year of the UK mini budget. At that time we did not predict the budgetary outcome but we did underweight sovereign bonds based on their risk/return profile. It seemed that this was a picking up pennies in front of the steamroller like scenario. So, despite a large-scale gilt sell-off alongside an equity sell-off, the portfolio had a lower initial drawdown and has outperformed its benchmark by nearly three times since then. This is a demonstration of how a diversified and actively managed approach can help weather periods of market volatility and uncertainty.

Total Return Performance Line Chart – 30/11/2021-24/03/2026

Source: FE Fundinfo

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends. Investors should consider longer-term performance data and other relevant factors before making investment decisions.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 95.3.26