Markets last week were once again dominated by the war with Iran. The difference from recent weeks was that they cheered up, buoyed early on by suggestions from both sides that a ceasefire deal might be possible and the war brought to an early end.

However, as has been the case right from the start, the prospects for an early end to the war changed almost by the day. And we start this week with the two sides seemingly still far away from a deal and Trump threatening to destroy Iran’s bridges and power plants – and take Iran back to the stone ages – if Iran has not re-opened the Strait of Hormuz by 8pm this evening US Eastern Time.

What happens now – to state the obvious – remains far from clear given the ever-changing narrative coming out of the US and Trump’s propensity to announce deadlines and then extend them. But markets are rather less concerned than they were ten days ago.

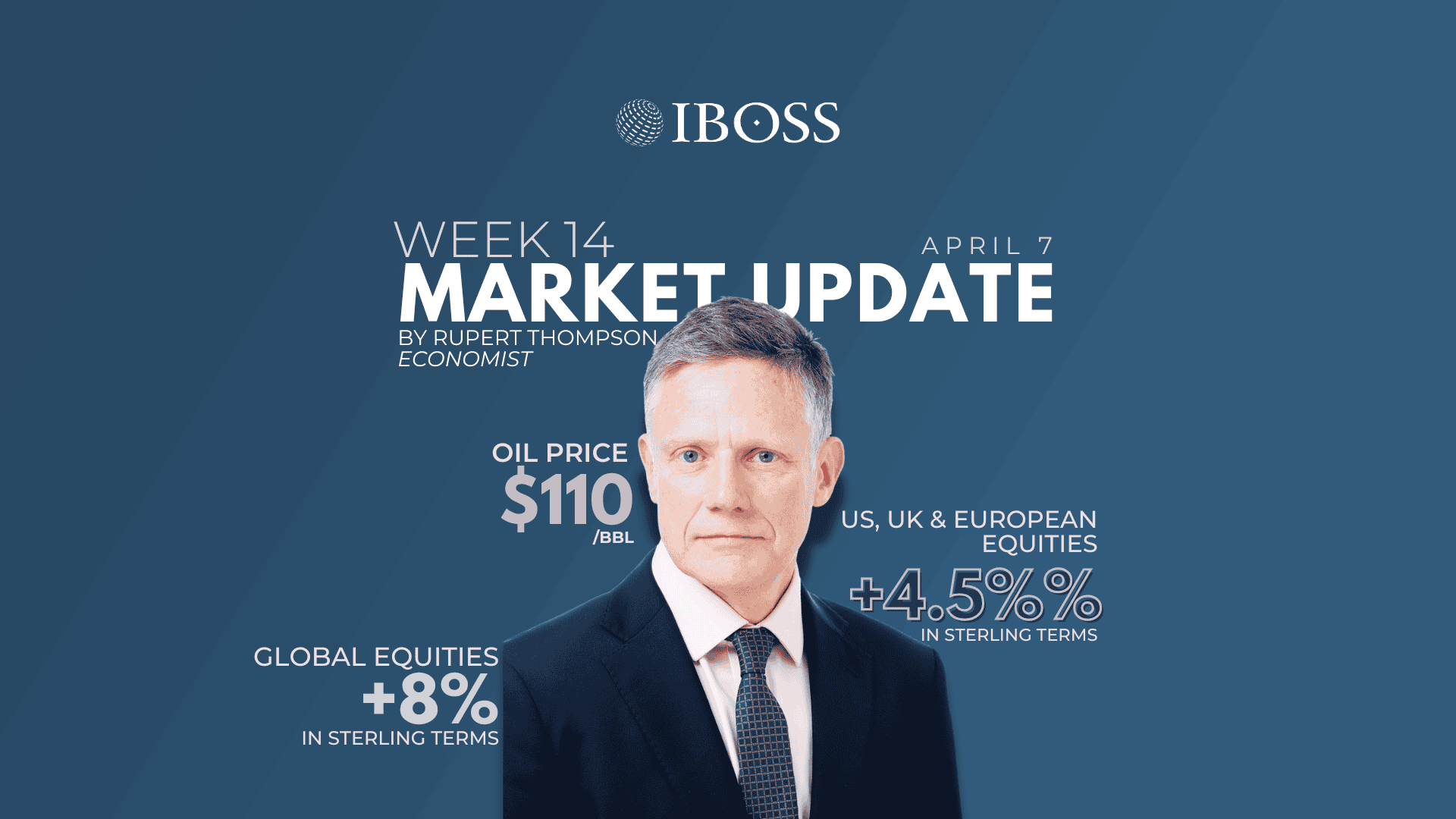

Since Friday 27 March, global equities have gained 3.7% in sterling term, reducing their loss since the war started to 3.7%. The US, UK and Europe led last week’s increases with all three regions up around 4.5%. Japan and Asia, which is most exposed to the disruption in oil supplies, were up a more modest 1.5% and 0.7% respectively.

Bonds also recovered somewhat last week with UK gilts and US Treasuries up 1.2% and 0.6%, reducing their war-related losses to 3.0% and 1.5% respectively. Fears that the forthcoming rise in inflation will trigger several rate hikes here in the UK were eased following comments from BOE governor Bailey that the markets had got ahead of themselves on this front. Even so, the market continues to price in two rate hikes later this year.

Fed Chair Powell also eased concerns that US rates could be increased, stating that the Fed was in a good place to wait and see how events in the Middle East turn out. The market believes him and expects US rates to be kept unchanged over the remainder of the year.

Meanwhile, oil – the lynch pin in all this – had another rollercoaster week. The Brent crude price dipped to $100 per barrel at one point but is back now close to $110 where it started the week.

Oil is being driven first and foremost by the state of play regarding a ceasefire and potential reopening of the Strait of Hormuz. But at the margin, there was the positive news that Iran is now allowing Iraqi tankers to pass through the Strait, potentially restoring 3mbd of the 20mbd supply halted by its closure. Furthermore, Saudi Arabia has re-routed to a pipeline to the Red Sea around two thirds of the 5mbd or so of its oil exports previously transported through the Strait.

Last week also saw comforting news on the health of the US economy. Payrolls in March unexpectedly posted their largest gain in 15 months. While recent data have been very volatile and too much should not be read into this increase, the numbers do reinforce the picture of a stable rather than deteriorating labour market. Manufacturing confidence also withstood the surge in oil prices, improving slightly last month.

This coming week, particularly the next 12 hours, will be crucial in determining which of the two scenarios outlined in last week’s commentary we are headed down. Macro releases will remain very much of second order importance for the markets. That said, US inflation data for March on Thursday will still garner some attention with the surge in oil prices expected to lead to headline inflation jumping from 2.4% to 3.3%.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 107.4.26