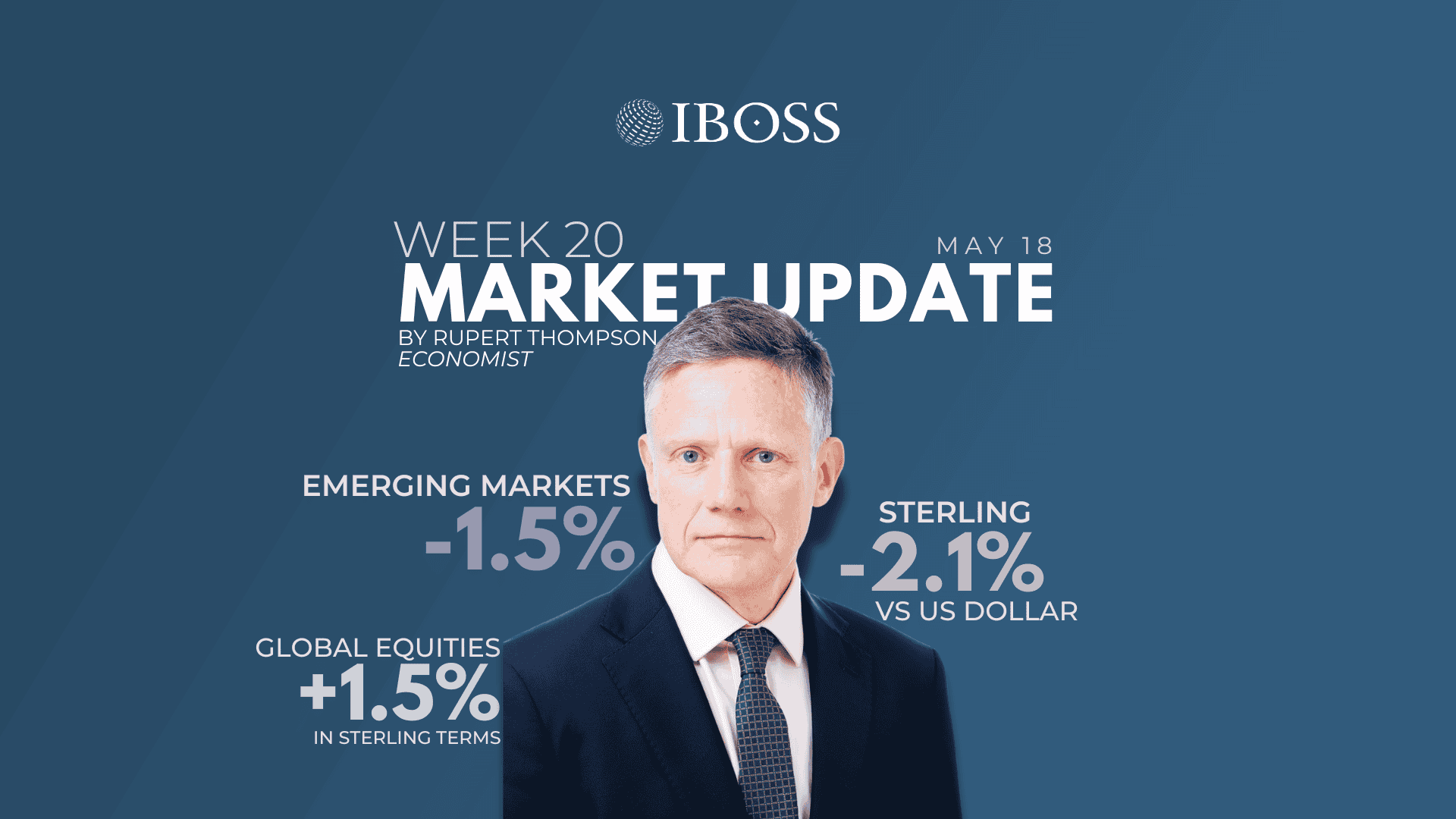

The upbeat mood of equity markets seemingly continued last week, at least as far as UK investors were concerned, with global equities up 1.5% in sterling terms. However, the picture beneath the surface was rather more nuanced.

The gains were only a result of a weakening in the pound which fell 2.1% against the dollar to $1.3350 and global equities were little changed in local currency terms. The drop partly reflected the political shenanigans in the UK but also a stronger dollar.

Most regions ended the week down slightly in local currency terms after a sell-off on Friday, except for Japan which managed a small gain and emerging markets which were down 1.5%. Given the speed and size of their recent rebound, equities could now well see a pause or unwind some of their recovery if there continues to be no progress in unblocking the Strait of Hormuz.

But it was bonds rather than stocks which were centre stage last week as they saw a marked increase in yields. UK gilts led the sell-off and were down 1.7% over the week with 10-year yields rising 0.27% to 5.18%. While events at home – more on that later – were partly to blame, yields rose across the world with 10-year US Treasury yields up 0.23% to 4.59%, their highest level in a year.

Inflation worries were to blame and were fanned by the latest US numbers which came in higher than expected and highlighted the impact of the war. Headline consumer price inflation rose to a three-year high of 3.8% in April from 3.3% and the core rate (which excludes both food and energy prices) increased to 2.8%.

Adding to the concerns was news that producer price inflation hit 6.0%, signalling the further upward pressure on consumer prices still to come. Even with Trump’s appointee Kevin Warsh taking over as Fed Chair last week, the market now believes US rates later this year will either be kept unchanged or raised slightly.

Inflation worries were exacerbated by the lack of progress in resolving the current stand-off in the Strait of Hormuz. Trump proclaimed the ceasefire to be on life-support and the US and Iran both seemingly remain miles apart in their demands and unwilling as yet to make significant concessions. Meanwhile, the latest report from the International Energy Agency confirmed oil stocks, which have so far cushioned the economic impact, were run down at a record rate in April.

Oil prices as a result continued their recent move higher and are back up to $110 per barrel. Just as significantly, markets are now assuming that oil prices will still be as high as $90 by year-end.

There had also been some hope that the long-awaited meeting of Presidents Trump and Xi might lead to China putting pressure on Iran to resolve the crisis. But this didn’t seem to happen. Indeed, while the visit was long on pomp and ceremony, it was short on concrete outcomes. Rather, it just maintained the status quo on key issues – most importantly the ambiguous US stance towards Taiwan and the one-year US China trade truce which still has six months to run.

Back here, all this rather took a back seat to events at Westminster which gave the chaos often seen in Washington these days a run for its money. Keir Starmer now looks pretty unlikely to remain as PM which will probably entail some shift to the left in government policy but the extent of the change will very much depend on his successor – which looks set to take months to sort out.

If Andy Burnham were to win the upcoming by-election in a month’s time – which is far from sure given Reform’s strong presence in the constituency and Streeting’s latest unhelpful pledge to rejoin the EU – he looks likely to become the new leader. This prospect has unnerved the gilt market given Burnham is the most left wing of the likely candidates (except for Angela Rayner) and his unfortunate comment a while back that one needed to get beyond being in hock to the bond market – although he has now pledged to stick with the fiscal rules.

The bottom line is that political uncertainty looks set to keep the gilt market on tenterhooks over coming months. Gilts will very likely remain volatile and yields could yet rise further, leading to price losses in the short term.

Even so, longer term investors should not forget that gilt yields are now looking quite attractive. The 5.2% yield on the 10-year gilt is well above the prospective return on cash – even if rates are raised 0.5% over coming months from their current level of 3.75%. Just as important, their yield in real terms (after adjusting for inflation) should be the highest for twenty years – assuming the forthcoming rise in inflation is quite short-lived.

Continuing in the positive vein, the first quarter UK GDP numbers provided a pleasant surprise. Activity unexpectedly rose rather than contracted in March, leaving it up a strong 0.6% over the quarter. These numbers undoubtedly exaggerate the strength of the economy – the last two years have both seen temporary post-budget bounces and activity may also have been brought forward by the war – but still leave it looking rather less of a basket case than had been feared.

This coming week, Wednesday sees the release of the minutes of the last Fed meeting, which will be more of a focus than normal given the dissent within the Fed at the moment, and Nvidia’s first quarter results. Then on Thursday, we have the May business confidence numbers for the US, EU and UK which will give the most up-to-date reading on how economies are withstanding the impact of the war. Finally, there are UK labour market and inflation numbers out on Tuesday and Wednesday respectively.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.