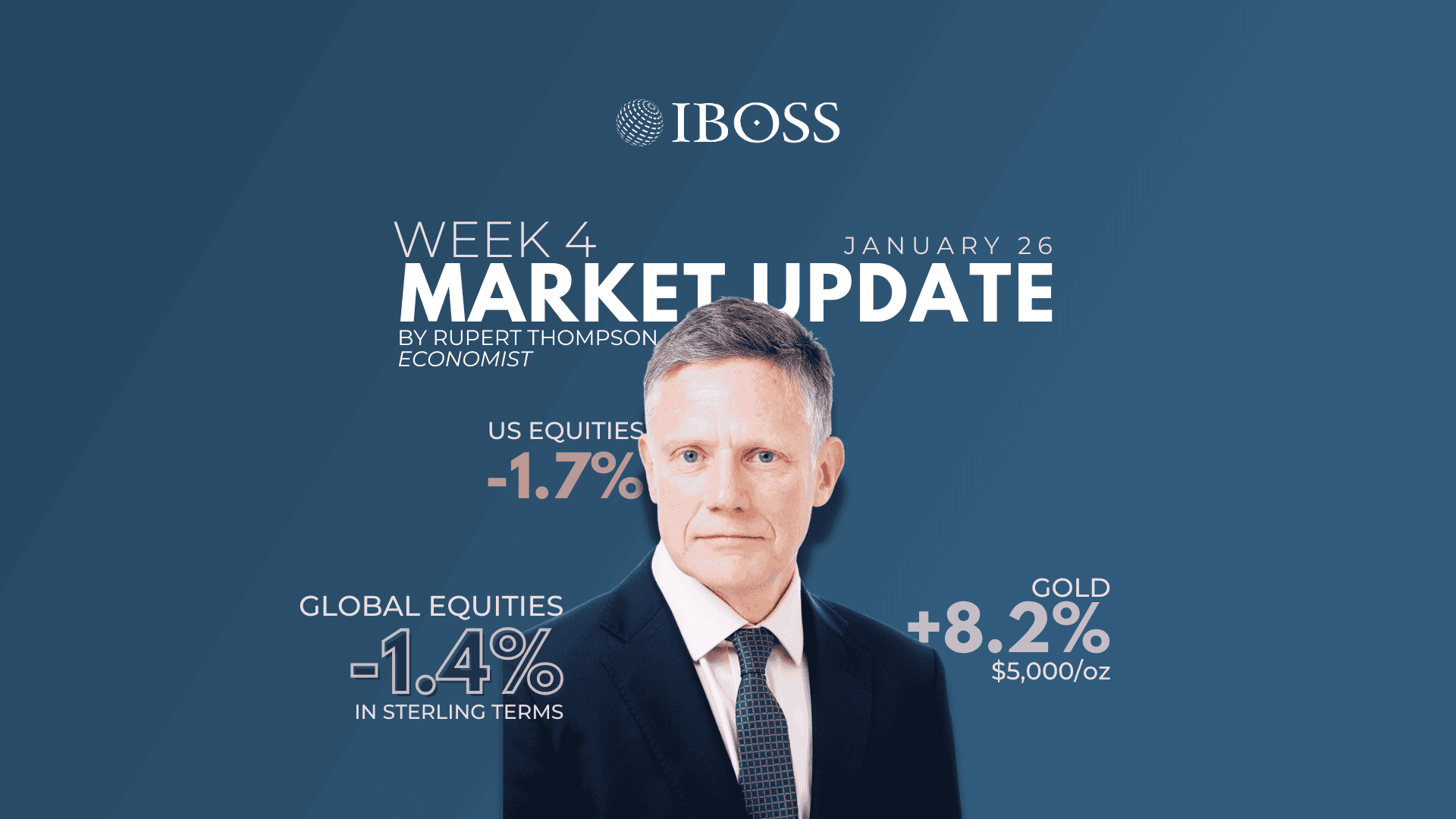

Global equities ended the week down a modest 0.4% in local currency terms. But they fell a somewhat larger 1.4% in sterling terms due to a rise in the pound against a weaker dollar to $1.36. Losses of around 2% early in the week caused by the consternation surrounding Trump’s threats over Greenland were largely recovered when he backed down.

Following some sweet-talking by NATO Secretary General Mark Rutte and signs that the EU were prepared to retaliate more forcefully than in the past, Trump said he would not take Greenland by force or impose tariffs on the UK and some EU countries from 1 February as previously threatened.

US and Japanese equities underperformed, losing 1.7% and 2.1% in sterling terms respectively – in both cases dragged down by a fall in their currencies. UK equities overall were down 0.8% but small and mid-cap stocks managed small gains on the back of better news on the economy – more on that later.

While equities were soothed by the de-escalation of tensions, gold was much more focused on the fact that there has been a further fracturing of the NATO alliance and the damage done cannot easily be undone. It surged as much as 8.2% and has broken through $5000/oz this morning. The latest geopolitical ructions have once again focused investor minds on the desirability of limiting exposure to the vagaries of US policy. Gold was the prime beneficiary while the dollar was a casualty.

As for bitcoin, it once again disappointed its fans, falling 6.3% over the week. Bonds, meanwhile, had a quiet week outside of Japan with US Treasuries returning 0.1% and UK gilts losing 0.6%.

On the data front, there was little released in the US other than the November numbers for the Fed’s favoured inflation measure. These were broadly in line with expectations and showed headline and core inflation both running at 2.8%. The Fed meeting next Wednesday looks almost certain to leave rates unchanged with the next cut not now anticipated until April.

The UK, by contrast, saw a deluge of data. These reinforced the more positive picture on growth shown by last week’s GDP figures for November. Retail sales showed a surprise 0.4% gain in December and consumer confidence rose for the second month running in January, reaching its highest level since August 2024.

Most surprisingly, UK business confidence jumped this month to its highest rate since April 2024 and is now higher than in the US and Europe. These numbers are volatile and need to be taken with a hefty pinch of salt. Even so, they definitely seem to show the economy picking up somewhat as the gloom and uncertainty prevailing in the run-up to the Budget fade away – just as happened with the 2024 Budget.

On the inflation front, there were no major surprises. The headline rate in December came in a touch higher than expected at 3.4% while the core rate was in line at 3.2%.

The bigger picture is that UK inflation looks set to fall back close to the 2% target in the second quarter as energy costs come down and underlying inflation pressures continue to moderate on the back of the weakening in the labour market. Underlying private sector wage growth slowed further to 3.6% in November and payroll employment continued its recent slow decline.

All this leaves the Bank of England looking likely to cut rates in April by another 0.25% to 3.5% with a final 0.25% reduction over the summer.

Japan has also been the focus of some attention. Prime Minister Sanae Takaichi has called a snap election on 8 February in the hope that her Liberal Democratic Party will win a majority. However, this is not a done deal despite her popularity as the two main opposition parties have just united to form a single new party.

The latest developments have caused some volatility in both the yen and Japanese bonds because of Takaichi’s enthusiasm for further fiscal stimulus measures. Very long-dated bond yields temporarily surged above 4%, causing some concern that the sharp move could cause issues for Western bond markets.

Meanwhile, the marked weakening of the yen in recent months to close to 160¥/$ has also prompted some consternation, not least from the Japanese authorities. Signs that they were contemplating intervening in the foreign exchange markets to support the currency led to a sharp recovery to 156¥/$ late last week.

This coming week sees no major economic data releases other than Q4 Eurozone GDP on Friday. There is the Fed meeting on Wednesday, but this looks set to be a non-event. Still, the US earnings season continues with Microsoft and Meta reporting on Wednesday and Apple on Thursday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 27.1.26