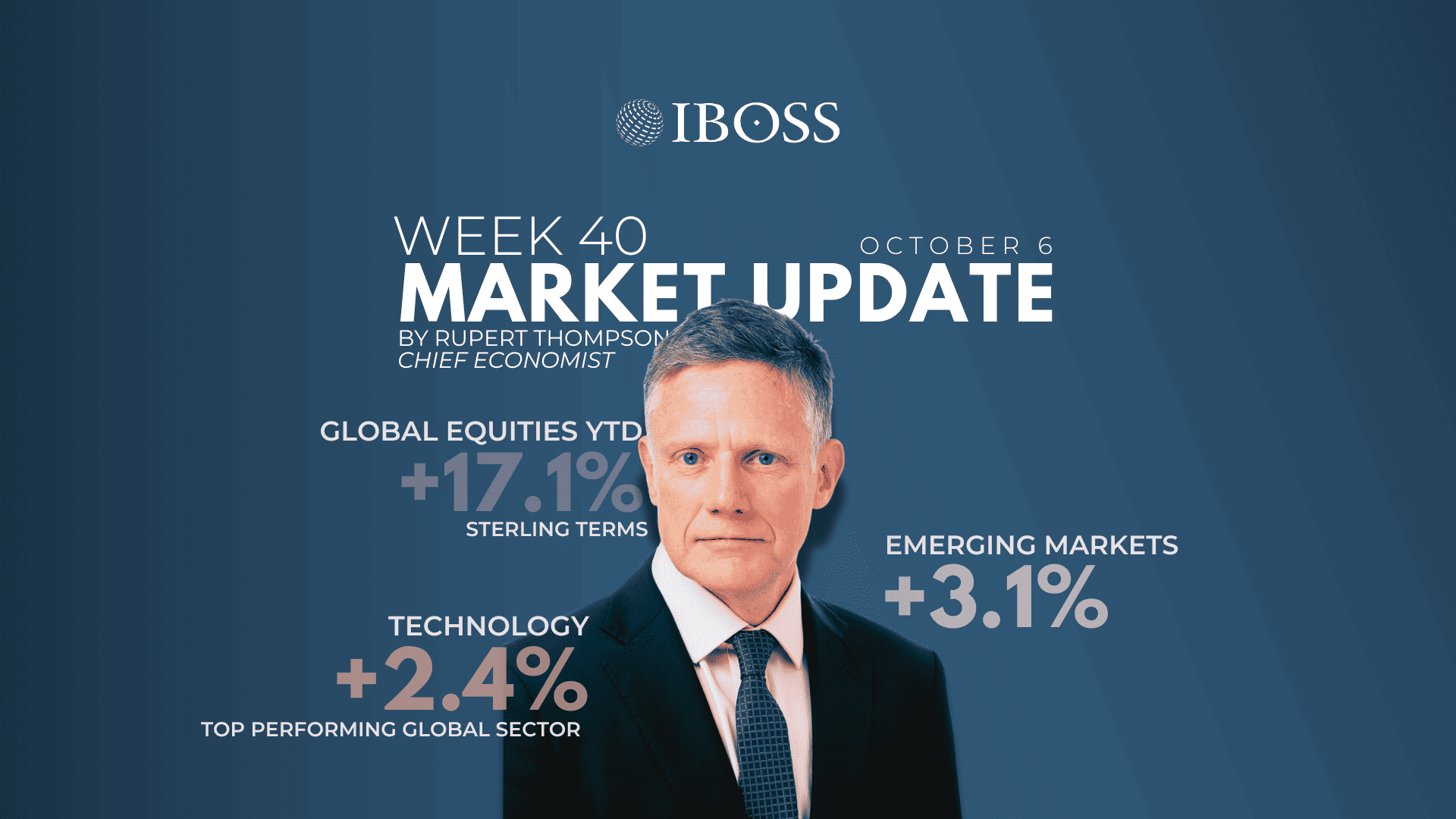

Global equities resumed their rally last week after a brief pause. They saw gains of 1.2% and 1.6% in sterling and local currency terms respectively, taking the year-to-date returns up to an impressive 11.7% and 17.1%.

US equities lagged with a rise of only 0.5% in sterling terms compared with increases of 2.3%, 2.9% and 3.1% for the UK, Europe and Emerging markets.

Strikingly, technology was one of the top performing global sectors, seeing a 2.4% gain even though the Magnificent Seven were flat on the week. This is part and parcel of a recent marked broadening out of the rally in tech stocks beyond just the US and is a major reason why emerging markets have been outperforming of late.

They are up 8.3% over the last month, partly down to growing confidence in the ability of China’s tech sector to flourish despite the best attempts of the US to ensure otherwise. The sector has surged 30% over the past month, swamping the 6% gain in the Magnificent Seven.

Korea and Taiwan are also benefiting from the AI merry-go-round. Korea’s two biggest chip-makers last week announced plans to supply OpenAI’s $500bn data-centre project. Coincidentally, OpenAI’s recent fundraising also valued the company at $500bn, making it the most valuable private company ever.

But it was healthcare stocks which were the stand-out winner last week, gaining 7%. This follows a period of poor performance and was fuelled by news of Pfizer securing a deal with the US Administration to avoid the new tariffs, along with their cheap valuations.

Japanese equities flatlined last week but sprung to life this morning following the selection of Sanae Takaichi as the new leader of the Liberal Democratic Party (LDP), which currently leads the minority coalition government. Takaichi will be the first female PM but more importantly for the markets, she favours renewed fiscal stimulus and efforts to shake up the corporate sector. The Japanese market duly closed 3.1% higher today although much of the gain was offset by a 2% fall in the yen.

France was also in the headlines this morning with the resignation of its Prime Minister, only hours after forming his cabinet and 27 days in office. French equities are down 1.5% on the news. But with five PMs in the last 21 months, this really just spells a continuation of the political paralysis, although it could trigger new parliamentary elections.

In the fixed income world, it was another quiet week. Bond yields edged lower, leading to UK gilts and US Treasuries both returning around 0.5%. Gold, however, continued its stellar run, rising 2.8% and breaking above $3900/oz this morning for the first time.

No real news has been behind gold’s latest gains. Rather, they appear to be down to FOMO (fear of missing out) which has attracted new investor inflows. While this clearly carries some risks, as does the sheer size of the recent price gains, the fundamentals behind gold remain strong – namely heavy central bank buying in the face of dysfunctional US policy, along with the prospect of sizeable US rate cuts and a further fall in the dollar.

We’re nearly done – yet without a single mention of any economic data! Macro news is normally front and centre of these commentaries but the shutdown of the US federal government on Wednesday meant no release of the US payroll numbers which would otherwise have been the week’s highlight. Instead, markets had to make do with an alternative and less reliable survey of US employment which painted a downbeat picture for September – as did the latest business confidence data.

Markets were largely unmoved by the government shutdown, as they have generally been in the past. Such shutdowns have usually been resolved within a matter of days or weeks. The last one was the longest and occurred during Trump’s first term in December 2018 and lasted for 35 days.

The shutdown is a result of Democrats and Republicans refusing to agree on the conditions to extend government funding. Some 750,000 employees are now furloughed and this will reduce GDP growth. But the hit should only be temporary unless Trump goes ahead with his threat to use this opportunity to make widespread permanent lay-offs.

This coming week, assuming the shutdown continues, the only macro event of any note will be the release of the Fed meeting minutes on Wednesday. The Fed and the markets will both be flying half-blind.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 283.10.25