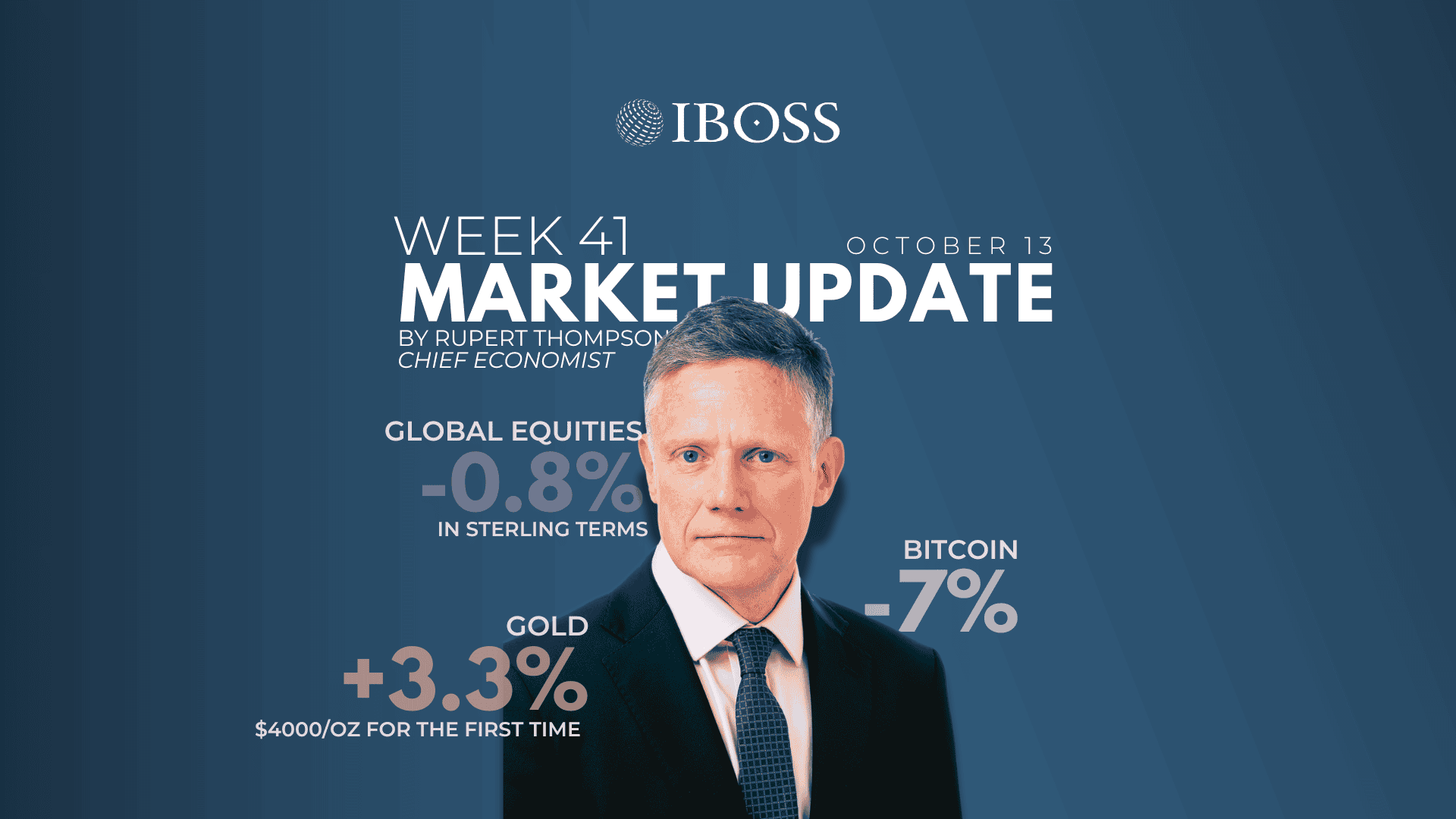

Last week was very much a week of two halves. Equities remained in bullish mode until Trump came along on Friday and threatened additional 100% tariffs on China from 1 November. Rather than trigger a sense of déjà vu and a feeling of here we go again, US equities took fright, falling 2.7% on the day. This in turn left global equities down 1.6% in local currency terms and 0.8% in sterling terms over the week.

The fall-out on other regions, however, has been limited. The announcement came too late to impact other markets on Friday but Asia is only down 1% or so this morning and Europe is actually up a little. The futures markets also point to US equities recovering a good part of their losses later today.

Bonds performed on Friday just as one would have hoped. US Treasury yields fell a little, returning 0.5% and providing an offset to some of the equity losses. Gold was down a little on the day but its modest decline can perhaps be forgiven given its spectacular rise this year. Indeed, despite its drop on Friday, gold still ended the week up 3.3%, breaking above the milestone of $4000/oz for the first time.

As for bitcoin, Friday saw further confirmation that whatever other merits it may or may not have, providing a source of protection in a market sell-off is not one of them. Bitcoin was down 7% on Friday.

Trump’s threat to hike US tariffs on China back up to 130%, close to the 145% level imposed briefly earlier in the year, brings back memories of the TACO (Trump always chickens out) trade. His move was a response to China’s action earlier in the week to slap on further restrictions on its rare earth exports which seemed a bid to get the US to ease controls on its high-tech exports.

The latest moves all seem part of the gamesmanship being played out by Presidents Xi and Trump ahead of their potential meeting later this month and the expiry of the second three-month extension of their trade truce on 10 November. Most likely, both sides will end up backing down from their latest threats and a further uneasy extension agreed – including some continued restrictions on their respective exports of rare earths and semiconductor chips.

Before Trump grabbed the limelight, markets had little macro data to pore over with the US government shutdown delaying publication of the most high-profile data releases. Instead, all it had to contend with were warnings from the IMF, Bank of England and the head of JPMorgan about the growing AI bubble, stretched equity valuations and the risk of a sharp correction.

Markets, however, were unphased by this doom-mongering. While we are also of the view that excessive optimism about AI and the high proportion of the equity markets accounted for by the tech giants increase the risks, we believe the appropriate response is to have a well-diversified portfolio, rather than sell up and head into cash. This is because the economic backdrop remains broadly positive with the Fed set to cut interest rates significantly and no recession in sight.

Equities are undoubtedly overdue a pause given the speed of the recent rebound. But further out, we expect growth in corporate earnings to fuel additional increases, particularly outside the US where valuations are less expensive. Even if this is an AI bubble, it could well inflate further. Diversification should allow one still to benefit from further gains while limiting the downside risk.

Returning to the here and now – and in another déjà vu moment – the French Prime Minister, who only resigned last Monday, was reappointed by President Macron on Friday. There is no sign that this latest shuffling of the deckchairs will be any more successful and full-scale parliamentary elections grow all the more likely the longer the current farce continues. Indeed, calls are growing for Macron to bring forward the Presidential election due to be held by May 2027.

Here in the UK, there was no economic data out and all the focus is still on the November Budget. It remains far from clear which tax hikes Reeves will end up setting upon to fill the hole in the public finances. But last week’s pledge by Kemi Badenoch to largely abolish stamp duty ups the ante. Calls by economists to use this opportunity to remove some of the worst inefficiencies in the tax system in an attempt to boost growth, rather than just boost revenues, also grow ever louder.

This week, the third quarter US earnings season kicks off on Tuesday with the big banks. As for economic data releases, they will be limited if the US government shutdown continues. UK labour market numbers are out on Tuesday and GDP numbers on Thursday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, incorporated in Guernsey (registered number: 42316).

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 302.10.25