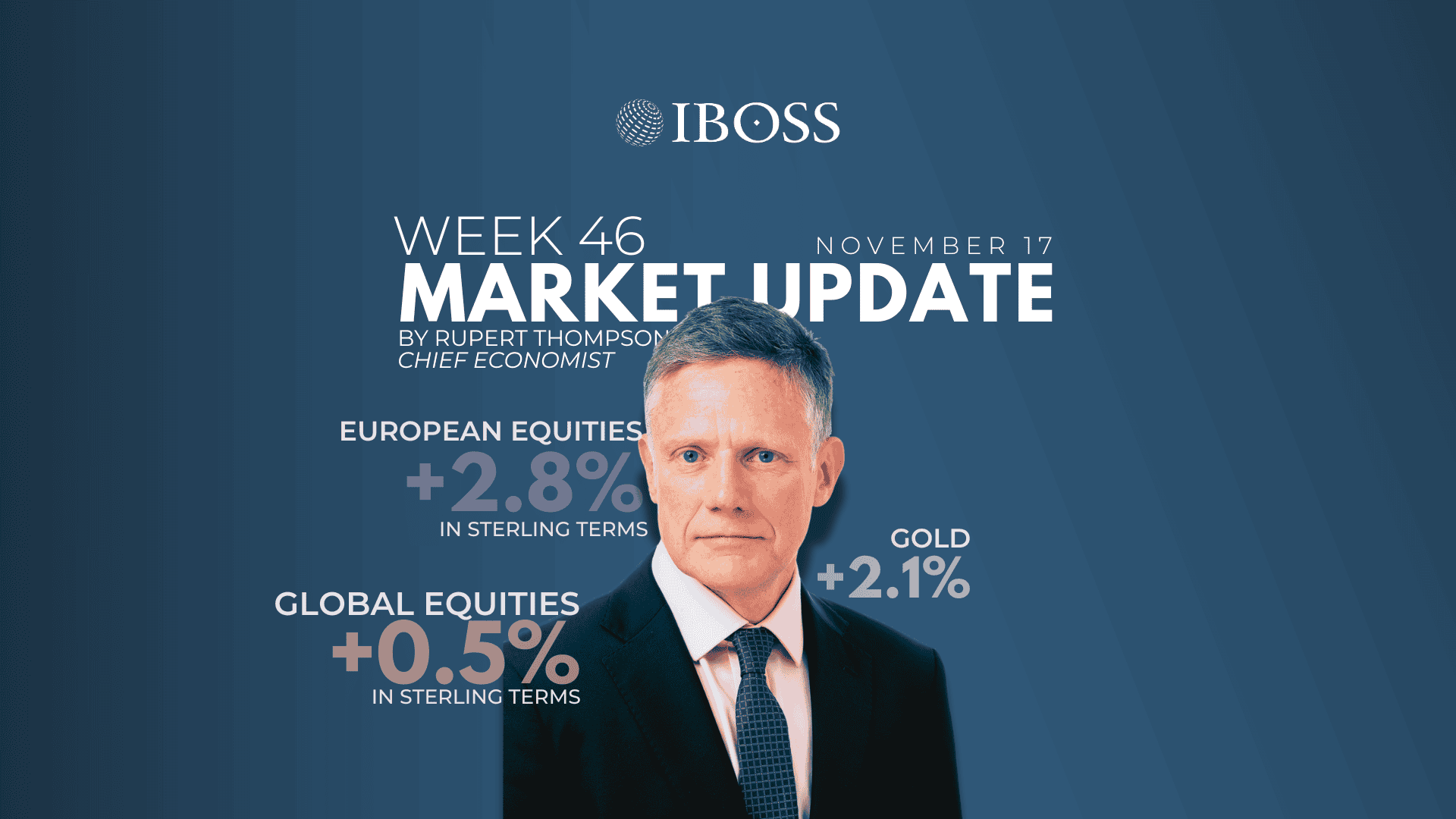

Last week saw some volatility with equity markets up as much as 1.5% on Monday, only then to fall a similar amount on Thursday. All this left global equities up an unremarkable 0.5% over the week in both local currency and sterling terms with European equities for a change the star performer, gaining 2.8%.

Bonds, meanwhile, had a negative week with UK gilts down 0.8% and US Treasuries losing 0.2%. Gold, by contrast, perked up with a 2.1% gain.

The week started well with markets enthused by a reopening of the US Federal Government, after the Democrats caved in, following the longest ever shutdown totalling 40 days. But this was then followed on Thursday by a burst of jitters, echoing the wobble seen the previous week, over the possible bubble in AI-related stocks.

This time, the nervousness was centred on the increasing amount of debt now being used – Oracle being the main culprit – to finance the massive expenditures on data centres. Until recently, the spend was largely being financed out of the enormous cashflows being generated by the tech giants which are a rather less problematic source of funds if things were to go wrong.

Various Fed officials also did their best to reinforce the seeds of doubt already sown by Chair Powell as to whether US rates will be reduced again in December. With the weakening labour market arguing for a cut but inflation of 3% arguing against, disagreement within the Fed appears almost as rife as in the UK government, although not half as acrimonious. The market believes the odds are now slightly against a December cut.

US data releases have been few and far between because of the government shutdown but will restart again this week with the delayed September payroll numbers on Thursday. The October numbers for several key releases, however, look unlikely ever to see the light of day as the necessary surveys were never conducted, making the Fed’s task all the harder.

Other than in the US, we have now had third quarter growth numbers released in most countries and overall they point to a continuation of sluggish growth. Eurozone GDP posted a moderate 0.2% gain over the quarter to be up 1.4% on a year earlier. Japanese GDP actually contracted 0.4% but the decline was down to US tariffs, should prove temporary and activity was still up 1.0% over the year.

Chinese data were released a few weeks ago and showed GDP up a firmish 1.1% on the quarter and 4.8% on the year. But the October numbers out on Friday painted a rather weaker picture with retail sales, industrial production and investment growth all slowing.

We also had GDP numbers out in the UK which were a bit weaker than expected. Activity grew a modest 0.1% after a 0.2% gain the previous quarter and was up 1.3% on a year earlier. The rather downbeat picture was reinforced by news that the unemployment rate rose from 4.8% to 5.0% in September, its highest level since the pandemic. Meanwhile, underlying wage growth continued to moderate slowly, easing to 4.6% from 4.7%.

The UK numbers of course were rather overshadowed by the chaos unfolding in Downing Street which left Starmer looking all the more like a lame duck by the end of the week. But it was the Chancellor’s U-turn which grabbed the market’s attention most. Having painstakingly laid the groundwork for a rise in income tax rates over the previous week or two, Friday saw news that Reeves had now ditched her plans to break this key manifesto pledge.

Apparently, this was down to the final estimates by the OBR of the black hole in the public finances being smaller than had been feared, allowing Reeves to fill it just with a hotch-potch of smaller tax increases along with extending the existing freeze of income tax thresholds from 2028 to 2030. The shortfall is now thought to be around £20bn, requiring tax increases/spending cuts of some £25bn if as expected the Chancellor increases her leeway in meeting the fiscal rules.

The short-termism of the government’s plans, and apparent absence of a strategic focus on boosting growth, duly took its toll on UK gilts with the 10-year yield rising 0.1% over the week to 4.6%. But this is far from another Lizz Truss moment. Yields remain 0.25% below their high at the start of the year and, far from plummeting, the pound was unchanged last week against the dollar.

This coming week, UK inflation numbers are out on Wednesday, US employment data on Thursday and business confidence numbers for the US, Eurozone and UK on Friday. Also, and almost as important, Nvidia’s earnings results will be released on Wednesday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 356.12.25