Last week’s market moves seem somewhat irrelevant given the dramatic developments over the weekend. But for what it’s worth, global equities were up 0.4% in local currency terms and 0.9% in sterling terms, while UK gilts and US Treasuries returned 0.9% and 0.7% respectively.

Much more important is the market reaction this morning to the attack by the US and Israel on Iran, the killing of its Supreme leader Ali Khamenei and the subsequent retaliation by Iran across the wider Middle East.

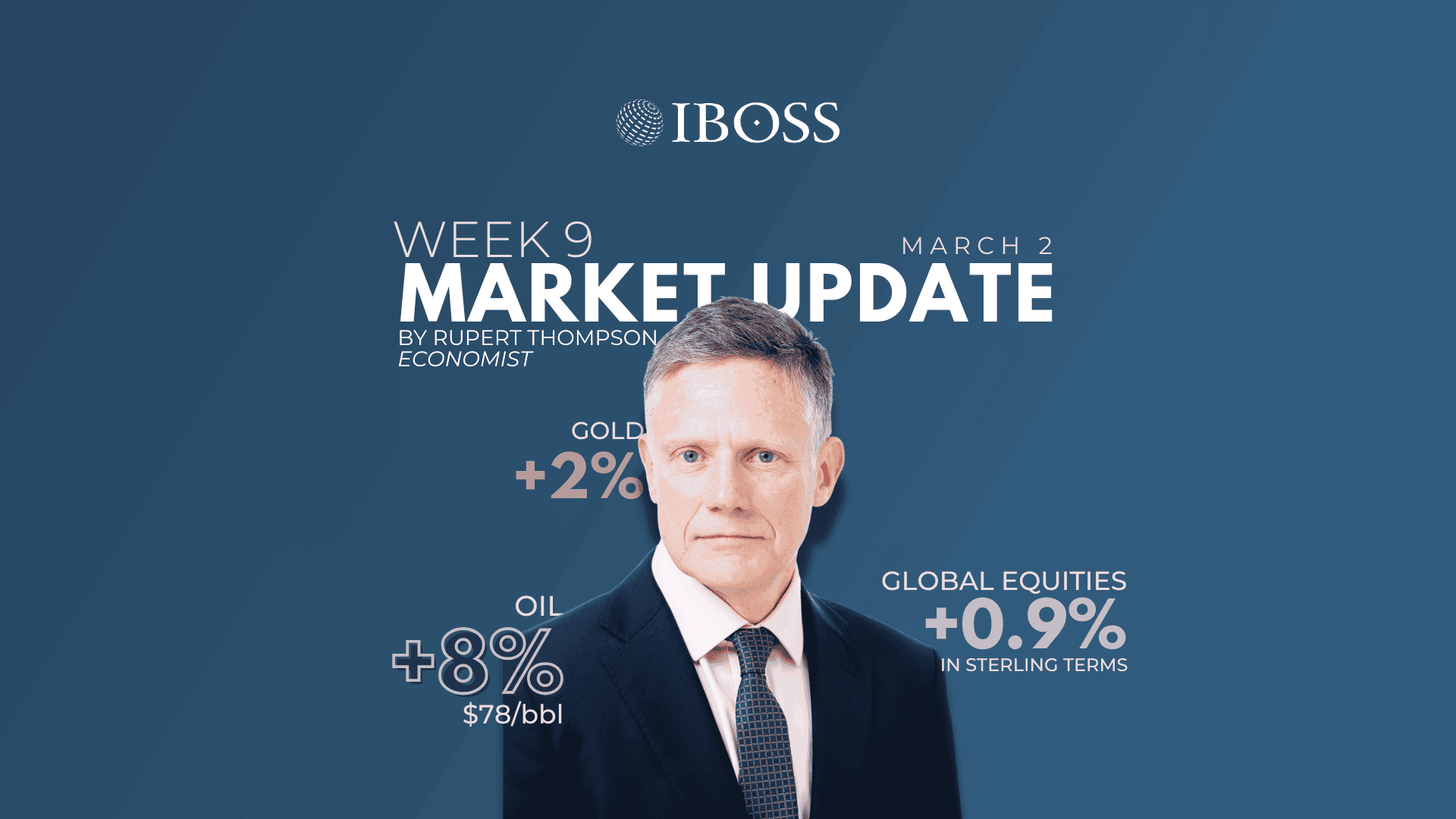

Market moves as yet have been quite limited and not a big surprise. The oil price has seen the biggest move and is up some 8% to around $78/bbl. European and Asian markets are both down 1-1.5%, as are Wall Street futures. Meanwhile, bonds and the dollar are both up a bit and gold has gained 2%.

The relatively sanguine response is down to several factors. First, the conflicts in the Middle East over the last couple of years have ended up having a surprisingly limited impact on markets – even when Iran was attacked last June which had previously been the big fear. Indeed, market resilience in the face of geo-political shocks is the lesson to be drawn from the experience of the last few decades, not just the last two years.

Second, the global economy is in a reasonably good shape to withstand the shock coming from the latest events. The most immediate risk comes from a further surge in the oil price. Shipping is already being deterred from using the Strait of Hormuz, through which some 20% of global oil supply is transported, and there is a danger it could be closed altogether – although this would curtail Iranian oil exports, limiting Iran’s incentive to do this. Oil infrastructure in the region could also be targeted.

Oil, however, is simply not as important to the world economy as it once was and global oil supply is also much less dependent on OPEC as a result of US shale oil. In addition, the market is currently in a state of excess supply with the oil price falling earlier this year to $60/bbl, the lowest level since 2021. Even after this morning’s jump, oil remains well below the high of $120-130 touched briefly following Russia’s invasion of Ukraine.

To be sure, the oil price could yet head up to $100 or higher. There is also the impact of the disruption being caused to shipping more generally and also to airline traffic because of the Iranian attacks on the airports of Dubai, Abu Dhabi, Kuwait and Bahrain.

Global growth will at the margin undoubtedly be reduced a little by this disruption to supply chains and inflation boosted a bit both by this and higher oil prices. But the key point is the damage should be limited. The big surprise over the last few years has been quite how resilient the global economy has proven to be both in the face of a major rise in interest rates and a substantial hike in US tariffs.

The macro backdrop going into this crisis is constructive, with global growth steady and interest rates falling. We do not expect the latest developments to derail this, even if the outlook does become a little less positive than before.

The uncertainty about both the extent and duration of the conflict and the longer-term outlook for Iran certainly means one shouldn’t be too complacent. But we do not believe this is a time to run to cash. Rather, it just reinforces our view that in this increasingly uncertain world, the appropriate investment response is to make sure one’s portfolio is well diversified – both at an asset class level and within equities, at the country and sector level.

Prior to the weekend, there were a couple of noteworthy events worth mentioning. First-off, we had Nvidia’s fourth quarter results which once again were stellar and beat market expectations. But far from jumping for joy, the share price ended the week down 7%.

Investor jitters about how the boom in AI plays out, which have hit software stocks hard in recent weeks, took their toll even on the golden child of AI. The mood of investors was not improved by a report from a little-known research agency which went viral – it predicted that AI would devastate the world as we know it.

There was also increased nervousness about the problems now facing private equity and credit markets. Some of the deals undertaken, when interest rates were super low and confidence super high, have hit problems now rates are much higher and sectors such as software are under pressure.

Worries over their exposure to this area led to the US banks falling 6% last week. Along with the drop in Nvidia, this led to the US underperforming significantly. Whereas the rest of the world, led by Japan and emerging markets, was up 2.2% in sterling terms, the US was flat. The over-exposure of the US to AI and the weakness of the dollar are no longer the only reasons to be wary of having too high an exposure to that market.

This week will be a busy one, not just because of Iran. February numbers for US business confidence on Tuesday and Thursday and payrolls on Friday will also be a focus. So too will developments in China, with important policy meetings starting on Wednesday which will see economic targets for the coming year released. DeepSeek, the Chinese AI company, is also due to release on Wednesday its first major model update since last January when it unnerved the markets with the performance of its low-cost AI model.

Last and of least importance, we have in the UK the chancellor’s Spring statement on Tuesday. The OBR will put out a new set of economic forecasts which should see the fiscal headroom little changed. With no real pressure this time – unlike in the last two budgets – to raise revenue, Rachel Reeves should stick to her longstanding intention of only one major budget a year and keep any policy changes to a minimum.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 67.2.26