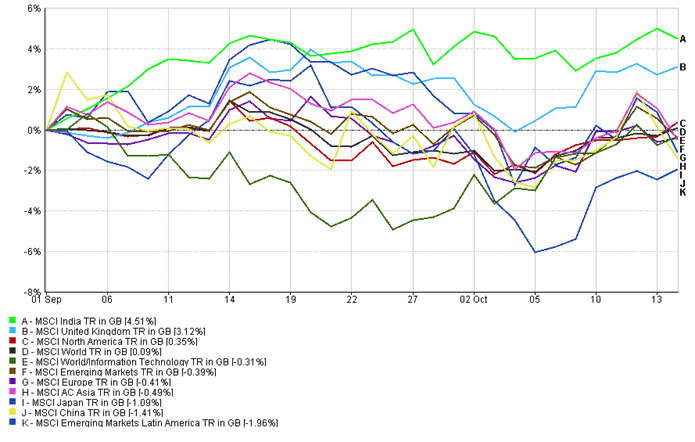

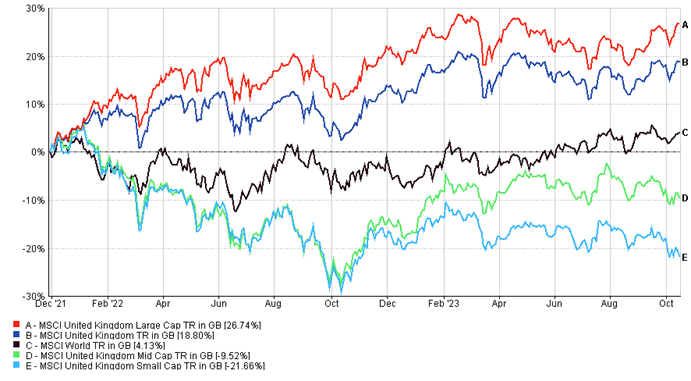

Once again, India and the UK have been leading the equity markets over recent weeks (fig.1), though for very different reasons. While India undoubtedly has its animal spirits in fine form with a strong showing across the cap spectrum, the UK, on the other hand, is very much a large cap story (fig.2).

The period since Fed Chair Powells’s epiphany back in November 2021, has been truly remarkable in many sectors and geographies but perhaps nowhere more so than in the UK. It could seem paradoxical that the Chair of a central bank from another country could be so influential, even if it is America. Unfortunately, the Fed seemed to convince Bailey of the BoE (and Lagarde of the ECB) that everywhere inflation was probably transitory. Rates were subsequently kept too low for too long, and the inflation genie duly escaped the bottle.

Ever since rates started rising, and appeared to be unanchored, smaller companies have been underperforming their large-cap peers. The BoE’s rate policy, combined with their inconsistent messaging, lambasted to the point where Bailey appeared on the front page of tabloid newspapers, making for difficult economic conditions, and this especially affects smaller companies.

Global Equity Performance – 01/09/2023 – 16/10/2023 (fig 1) *

UK Equity Performance – 01/12/2021 – 16/10/2023 (fig 2) *

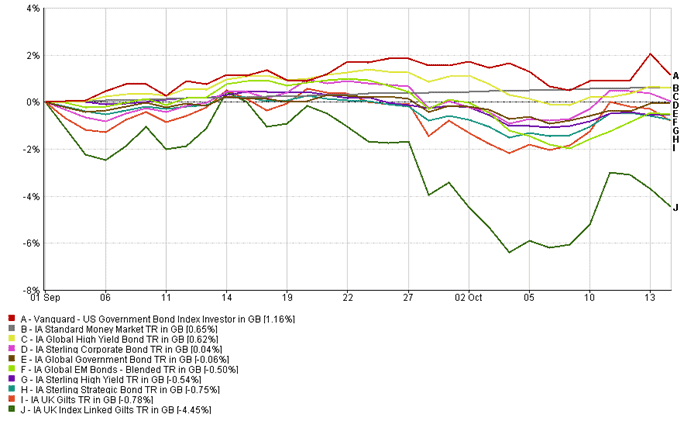

Overall, global equity markets were choppy and, in sum, rather directionless. The same can be said for global bond markets (fig 3), with the dishonourable exception of UK Index-Linked gilts, which have lagged most fixed income markets since the ‘transitory’ label was officially retired. In fact, ‘linkers have remained down 44% since the beginning of December 2021.

Fixed Income Markets – 01/09/2023 – 16/10/2023 (fig 3)*

The elephant in the room for any conversation with clients right now, is the healthy returns available on cash funds, whether tying their money up or even, in some cases, on an instant access basis. So prominent is this issue, that at the recent M&G Bond Vigilante forum, they did actually have a large (model) elephant in the auditorium.

Whilst current cash rates are undoubtedly appealing, there are more issues to consider than the here and now. Opportunity cost is certainly a consideration (The Dilemma: Clients, Cash and Timing the Market), and we would contend that the starting price for many equity and bond markets is more attractive now than it has been for many years.

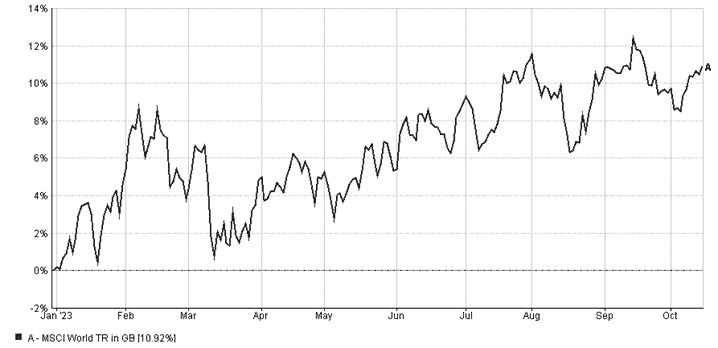

It is also worth highlighting, that a sterling investor has had a return of nearly 11% from the MSCI World Index so far in 2023. We all know the limitations of past performance, but it’s a statement of fact to say that circa 11% is better than any cash fund available in developed markets (fig. 4).

MSCI World – 01/01/2023 – 16/10/2023 (fig 4)*

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 287.10.23