This update covers the period, year-to-date, up to October 9th 2025 continues to be a strong one for the IBOSS Core range in both absolute and relative terms. As mentioned last month much that positivity is due to the changes, some might say chaos created by the Trump’s administration’s approach to pretty much everything.

Macro & Markets

The Trump Effect

President Trump effectively re-dealt the cards for global markets across the asset classes. At the same time companies and countries alike have been forced to reassess everything from supply chains to who might have their back in armed conflict situations. The fundamental impact for of Trump 2.0 policies has changed the world irrevocably and to a degree that few saw coming. While his approach to geopolitics is unconventional and sometimes challenging even for his most ardent supporters, he does force change things and make things happen. In the case of the various geopolitical conflicts that his administration is involved in, it is extremely hard to argue that previous administrations or other world leaders had viable plans in place for long term conflict resolution.

Market Impact of a New World Order

This has huge ramifications for global markets, and we can’t cover them all in depth but there are some key listable points. Firstly, its not in any company’s interest to go against Trump policies publicly, nobody wants the Zelensky treatment. That does not mean people necessarily agree with him, but it pushes much of the narrative behind the closed doors of the boardroom or the cabinet room. Secondly, new understanding of supply chains, enemies, frenemies, and trusted partners is a game everyone is having to learn on the job, and quickly. Big picture investment themes are obviously headed up by AI and the tech stocks but running alongside of equal if not greater importance is the energy and commodity complexes.

When Renewable Ideals Confront Resource Realities

Its an unfortunate reality that the world still needs fossil fuels, and it also needs a broad range of commodities that have to be mined. In the case of gold, because trust in anything created by man is rapidly waning and with things like rare earths, there is currently no alternative. We showed the chart below last month and it looked pretty crazy then, but things have only got more extreme since then. At the time of writing (09/10) we are going through another period in the ‘everything rally’. Intuitively when investors are buying pretty much anything they can, you wouldn’t expect gold and commodities to be shining. That tells us there are other factors are at work here. For now, though precious metals and AI appear to be unstoppable, and FOMO is a powerful emotional driver in an age more powered by retail investors than ever before.

JPM Natural Resources and Ninety One Global Gold 5 year performance from 8/10/2020 to 08/09/2025

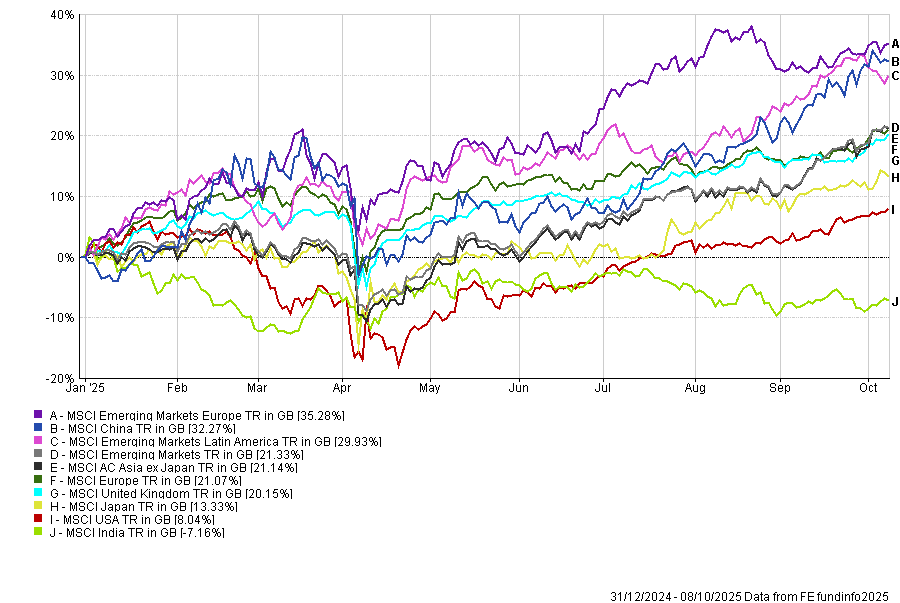

The Global Equity Winners of 2025 (So far)

While the US continues its climb back up from the ‘Liberation Day’ fallout, so does much of the global equity complex, and led by emerging markets. The AI and tech fuelled boom is a global phenomenon noy just a US one. That means whilst investors are benefiting from an AI bonanza in multiple geographies, the risks of a sector wide pullback are also global in nature. Correlations are important here but as ever with correlation, we need to sort out the directional wheat from the magnitudinal chaff. The tailwinds for the commodity rich Lat Am with their relatively cheap labour costs are semi-permanent tailwinds. In Asia as new relationships are formed and supply chains re-imagined there is considerable scope for strong relative and absolute performance.

Selected MCSI countries from 31/12/2024 to 08/10/2025

Positioning and Outlook

As ever, we remain firmly focused on diversification and it feels in many respects like the investing world has moved closer to our longer-term positioning. However, in simple terms as each asset goes up in value on an almost linear fashion, the risk/return profile becomes slightly more challenged.

Over the last few months we have dialled down the beta of the portfolios, increased the use of absolute return strategies and built more diversification into some of the individual sectors, for example hedging part of our Japanese exposure.

We continue to see opportunities across the asset classes, but we are increasingly mindful of starting valuations. We expect the final quarter of 2025 to be a continuation of the remaking of the world order and that will continue to produce new winners and losers at both a country and company level.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 293.10.25