Balancing Income, Growth & Capital Preservation

Over the past few weeks, we have been speaking with advisers about decumulation, what is working, what is not, and where the biggest risks and opportunities lie. These conversations highlighted several recurring themes. Below are six points that came up time and again.

Losses Matter for All Investors Irrespective of Time Horizon

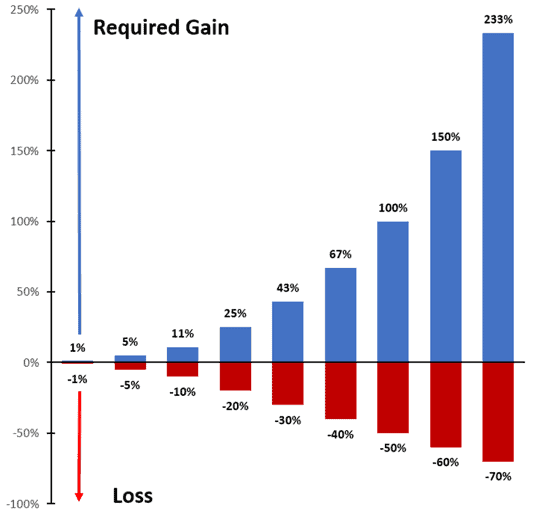

Losses affect both accumulation and decumulation portfolios. We put together the graphic below to show hard it can be to recover from a large portfolio loss. A 50 percent fall requires a 100 percent gain to recover.

The Outsized Impact of large losses

However, the impact of drawdowns can be magnified for clients in or approaching retirement. Not only do they not have the ability to wait out any prolonged market falls but selling assets to meet withdrawals in a market downturn can be particularly damaging. For example it took equities 10 years to beat cash following the .com bubble and more than 13 years to beat fixed income.

No Single Portfolio Fits Every Decumulation Client

- The FCA review highlighted that a single “retirement portfolio” is unlikely to suit all clients.

- Clients ultimately have different objectives for retirement however their capacity for loss and tolerance to risk cannot be overlooked.

- It is standard practice for accumulation clients to differentiate between higher and lower risk clients. It seems sensible that the same approach is appropriate for decumulation clients. After all, a client’s needs at 60 are likely to differ to one approaching 90.

- It was also clear that clients in decumulation can see sudden changes in their circumstances which can meaningfully impact their plans for withdrawals. Advisers are clearly best placed to react but the investment portfolio should be tailored for any changes. Regular reviews are essential to keep on top of these changes.

The Defining Characteristic of Any Decumulation Investment

Ultimately clients in retirement will want to withdraw capital. This can be done in any number of ways and for any number of reasons. Some approaches we heard throughout the week included:

- A natural income for luxury spending

- A monthly defined income for essentials

- A lump sum for a one-off purchase

- Yearly withdrawals to fund a cash bucket

Whatever the approach, the defining characteristic for any investment used within a retirement portfolio is to be able to withstand withdrawals.

We think these 3 attributes below are excellent places to start:

Low Drawdowns to match with a clients capacity for loss and reduce the time taken to recover from losses.

Lower volatility to reduce the impact of sequencing risk during withdrawals

An element of Income rather than relying solely on growth

Why Income is only one slice of the total return pie

- Income can be a powerful tool. When growth slows or disappears, yield can help support withdrawals and maintain returns.

- However, over reaching for yield can increase the concentration in your portfolio and destroy the essential defensive characteristics mentioned previously. For example in 2020, UK equities were the only asset providing attractive yields. Investors craving income flocked to these assets and saw their values plunge to the tune of -30% in the COVID sell off as dividends were written to 0.. .not ideal for decumulation clients.

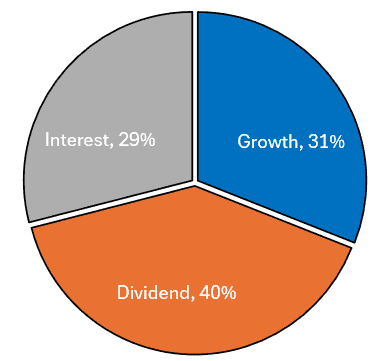

- Ultimately, as one adviser put it, income is only one slice of the total return pie. The chart below shows the breakdown of returns for IBOSS Decumulation Portfolio 4. As you can see if growth were to stall, there would be other drivers of return.

Return Breakdown – IBOSS DECUMULATION PORTFOLIO 4

Why Growth Remains Important

- Growth continues to play a vital role in retirement. It helps protect against inflation, prolongs portfolio life, and supports sustainable withdrawals.

- Relying on income alone risks eroding capital if yields fall or spending needs rise.

- However, relying on growth alone leaves your portfolio vulnerable in the event of a prolonged bear market. In these environments Income is essential.

Why Balancing Income, Growth and Capital Preservation is Vital

| If… | Then… |

| Growth is limited | Income can support withdrawals |

| Yield falls | Growth can drive returns |

| Markets decline | Focus shifts to limiting drawdowns and preserving capital |

The objective is simple. To support withdrawals as effectively and consistently as possible, whether clients take natural income, monthly payments, or periodic cash top-ups.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 309.11.25