Markets don’t care about the calendar

The first few weeks of 2026 have been a mirror image of 2025, and the reason is simply that the same factors are dominating the markets. While traders’ bonuses might depend on what they achieve in a quarter or over the year as a whole, markets operate on their own dynamics, and those haven’t really changed. The chaos around Trump’s economic policy continues to cost the US in terms of confidence and trust. The latest example came this week, when the president said the US wanted a weaker dollar, and then within a few hours Scott Bessent, the so-called “adult in the room,” contradicted him, saying they wanted a strong dollar.

Our two cents, is that this administration does want a weaker dollar, and we are positioned for that outcome, but Bessent knows it needs to be controlled. Economics by soundbite helps nobody. The “quiet quitting” a reference to companies and countries at the margin moving toward less US dependency has to remain as far under the radar as possible, as nobody wants the Oval Office Zelensky treatment.

The Art of (everybody else’s) Deal

Some of the second and third-order effects of Trumpian economics will not be fully realised for years, but you only have to look at how many deals excluding the US are getting done. Take the EU–India deal, which had been dragging on forever and has now, all of a sudden, crossed the line. The Mercosur deal between Latin America and the EU is also receiving the EU “should get on with it” treatment, as urged by German Chancellor Merz.

The UK had already concluded a deal with India, has progressed on agreements with China and South Korea, and we would expect renewed cooperation between the UK and an EU that is looking to make friends and strike deals. We don’t think it is too much to say that a new age of pragmatism is sweeping much of the globe. Trump’s attempts to bully the Europeans, Canadians, and the British for the umpteenth time may just have revealed the current limits of his tactics of relentless threats.

The debacle over Greenland, along with the speeches at Davos by Trump himself, as well as Macron and Carney, will be remembered for some time. To return to the “Zelensky treatment,” these events and speeches seem to be redefining the terms of engagement with friends and foes alike.

Diversification remains the name of the game

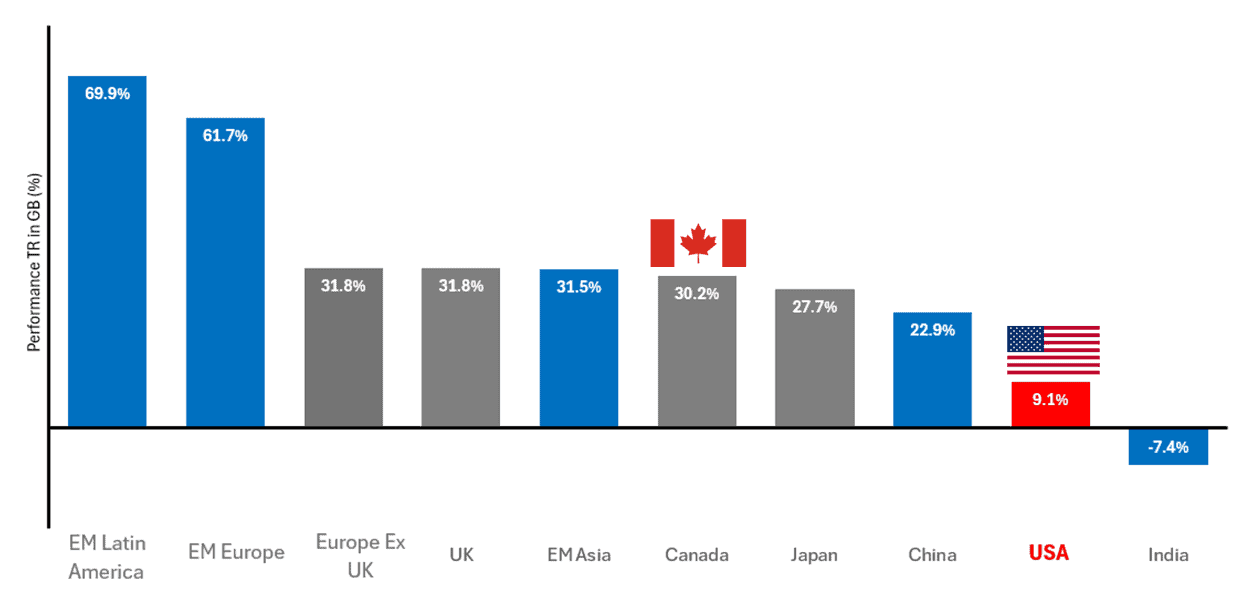

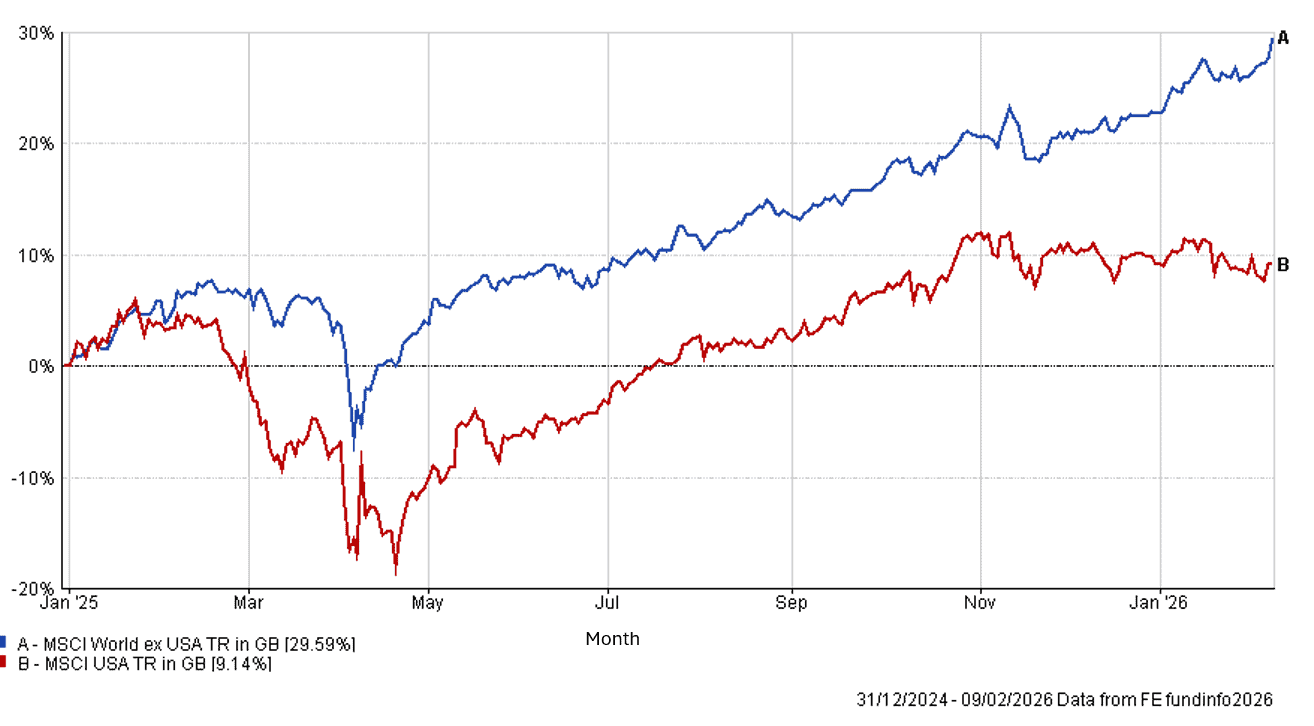

The two charts below highlight the performance of equity markets this year. It remains the case that the US continues to lag a broader basket of regions, as investors increasingly look toward future areas of potential opportunity. In fact, at the time of writing, 2026 has seen the US index fall by 0.4%, while the rest of the world has risen by 6.4%. Last year, much of the difference could be attributed to the weakness of the dollar, and while the dollar has fallen year to date, it has been the relative strength, or lack thereof, of US stocks that has driven the divide.

We have kept these charts inclusive of 2025, to demonstrate the actual effect of Trumps second term on the various markets.

MSCI Selected Country Indices 01/01/2025 > 09/02/2026 (Fig.1)

Source: FE Fundinfo

MSCI World Ex USA Vs. USA 31/12/2024 > 09/02/2026 (Fig.2)

Source: FE Fundinfo

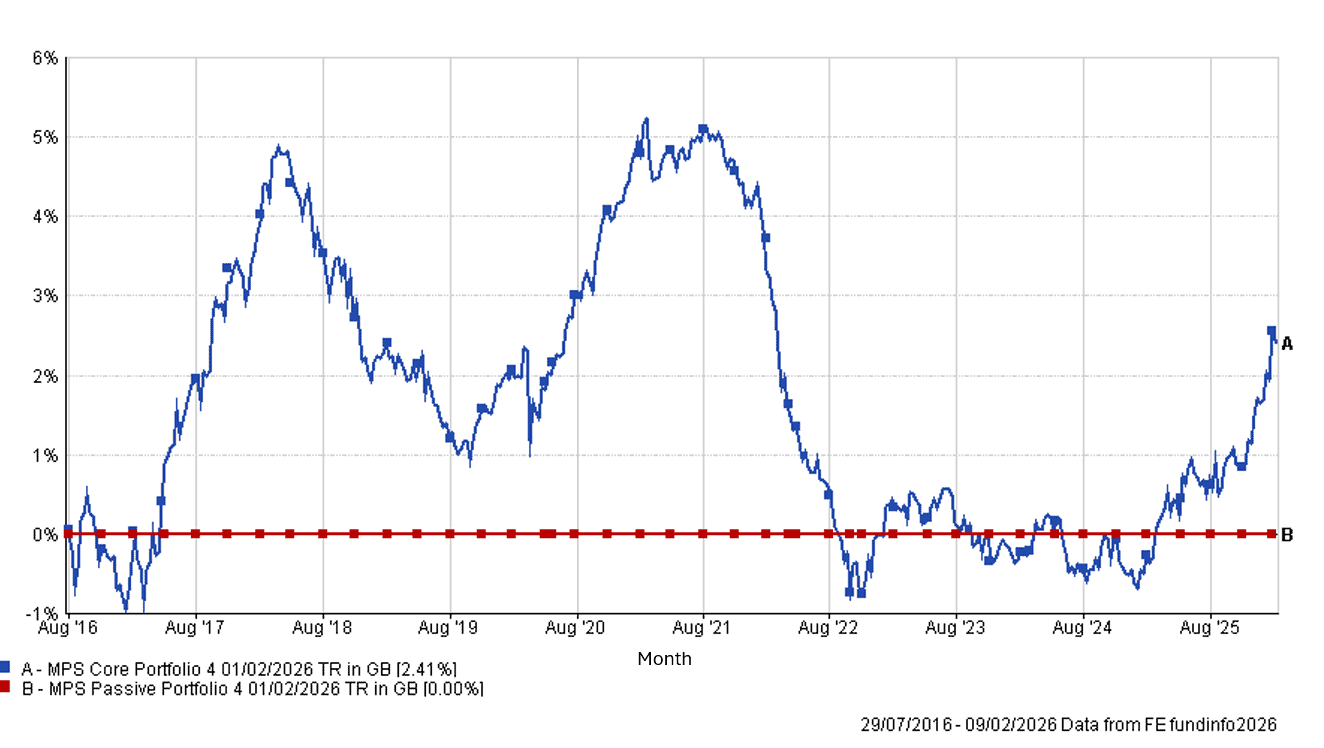

Passive & Active Returns

We showed the chart comparing our Core and Passive ranges last month (Fig 3), and we thought it was worth updating it for you here. This is now the third time that the Core range has outpaced our Passive range, taking into account that the strategic allocations are the same and much of the tactical positioning is as well. The biggest difference is simply the stock and bond selection versus the respective indices. We love all our children equally, but in our view, the Core range remains well positioned given current market conditions; however future performance cannot be guaranteed, given our view of the world and the shifting tectonic plates across styles and sectors.

It is worth highlighting that we expect markets to remain volatile across both equities and fixed income, and in this environment, we believe that flexibility is key to making the most of the various opportunities.

Core Vs Passive Portfolio 4s – Start of Data > 09/02/2026 (Fig.3)

Source: FE Fundinfo

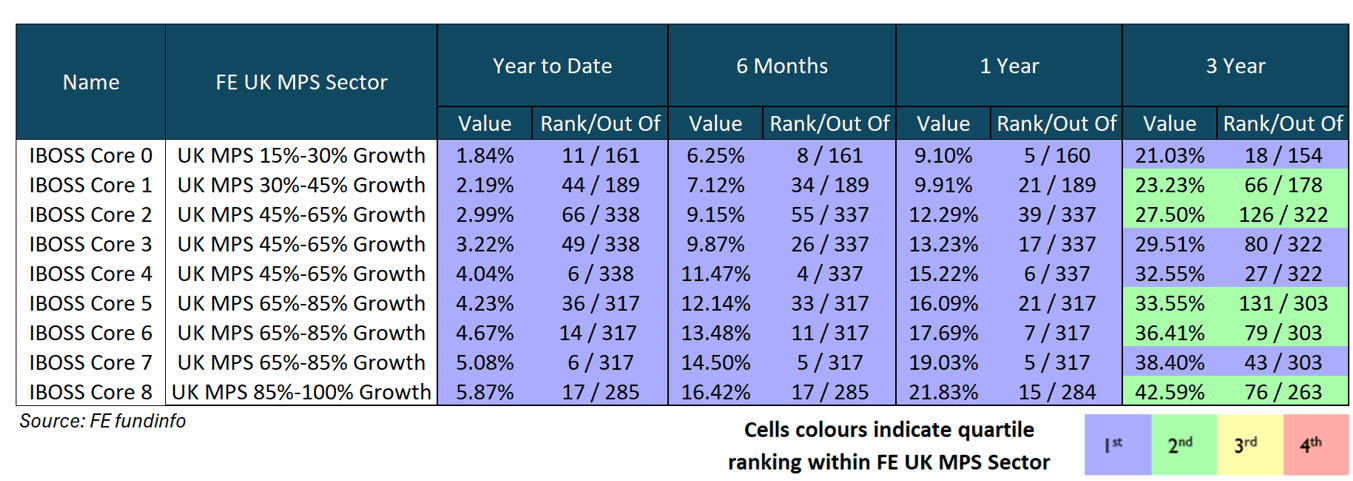

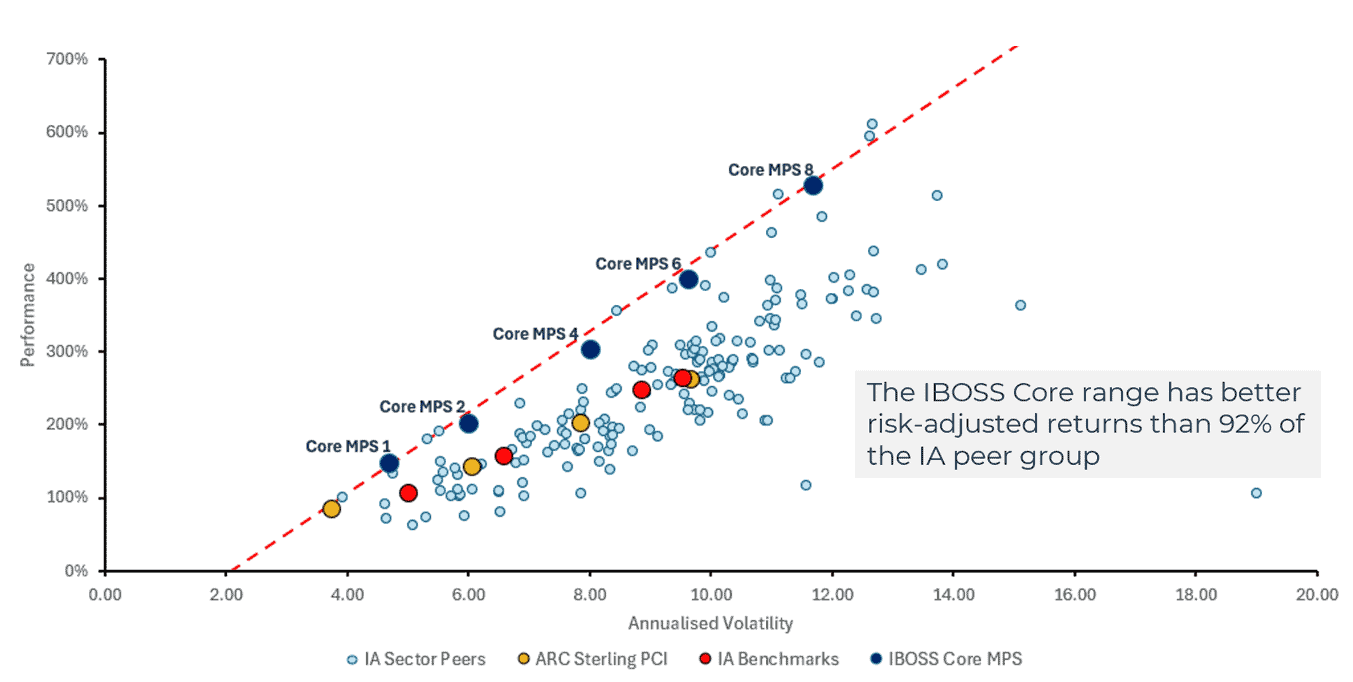

IBOSS Performance Review

Markets have moved quickly this year but have continued to reward broad diversification, with the rest of the world outperforming US equities by around 6% year to date. As we remain underweight relative to many peers, this has meant that a majority of IBOSS portfolios have outperformed, over the stated period, their respective benchmarks through January, and now across most cumulative time periods.

In addition, the portfolios have performed well relative to other multi-asset peers, as demonstrated by the chart below, which uses the FE MPS tool and ranks the IBOSS MPS portfolios against strategies with similar equity content.

Cumulative Performance & FE MPS Sector Ranking (Data to 10/02/2026)

In fact, the IBOSS Core portfolios now show outperformance across cumulative yearly periods up to and including 17 years. This is particularly meaningful to us, as clients begin their investment journey at different points in time, and it is encouraging to see that long-term discipline has been rewarded across the broadest possible range of entry points.

CORE MPS Risk & Return 01/11/2008 to 31/01/2026

Source: FE Fundinfo

Equally important has been the level of risk taken to achieve these returns. The portfolios continue to exhibit lower volatility and shallower drawdowns relative to the peer group, alongside strong long-term risk-adjusted outcomes.

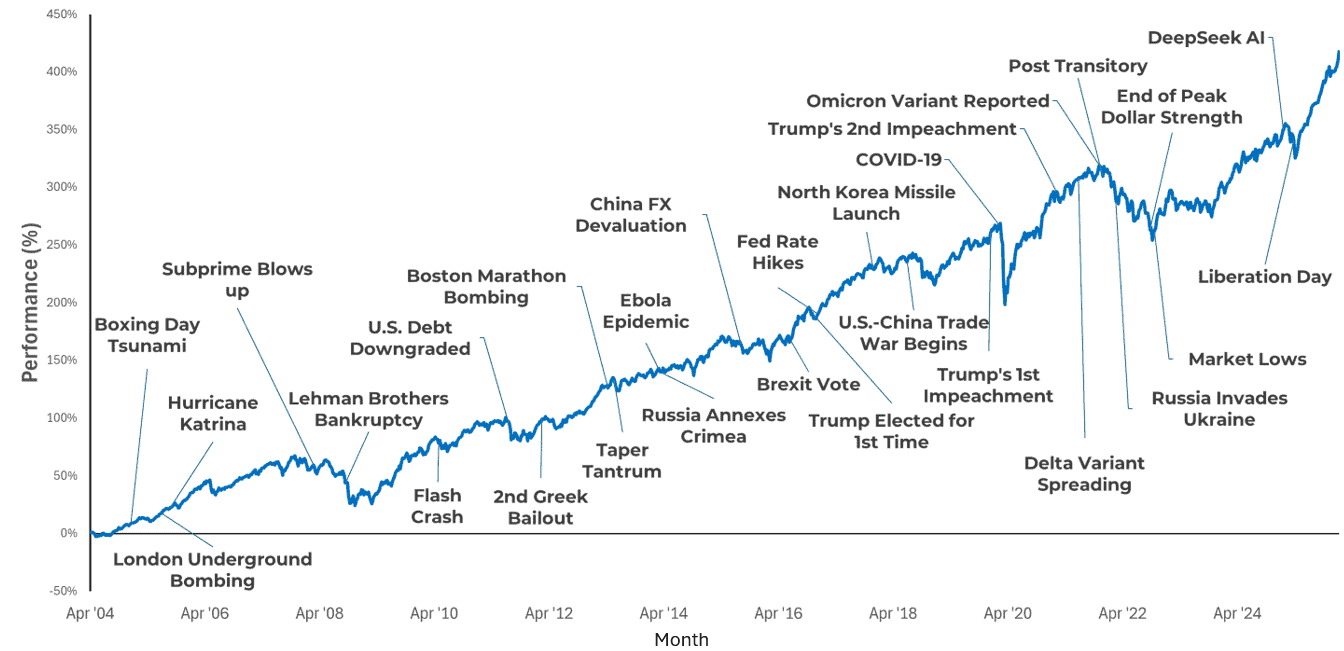

Why stay invested?

In recent months, more advisers have asked whether markets can continue at such a pace and whether a correction is overdue. Of course, we have no insight into short-term timing. Market corrections occur in most calendar years and are a normal part of investing. As last year demonstrated, periods of market weakness may create attractive opportunities for long-term investors.

The chart below, taken from our “Why Stay Invested” pack, illustrates that while markets are never short of concerns, patient investors have historically been rewarded over time.

IBOSS Core Portfolio 4 (01/04/2004 to 15/01/2026)

Source: FE Analytics

Performance Review

Whilst we have focused on the Core range for the purpose of this performance update, you can find the performance characteristics for the other ranges on our website. As we aim to run each range in a broadly similar manner, with a flexible approach to asset allocation and a strong focus on diversification, many of the ranges have exhibited comparable characteristics relative to their peers.

Key takeaways include outperformance year to date (09.02.2026) across all ranges against their respective peer groups, as well as outperformance from the Core, Passive, Blend, and Decumulation ranges versus the IA peer groups over 1, 3, and 5 years.

If you’d like a bespoke update from us, get in touch with your local BDM.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 53.2.26