We have experienced years in which markets have hung on every word from central banks, with clear evidence of coordination in policy direction across major financial centres. However, markets are constantly evolving, and as central banks become increasingly focused on addressing their own regional and national objectives, the natural consequence seems to be a weakening of global policy synchronisation.

There is, of course, little doubt that interest rate decisions will continue to exert a significant influence on markets, and that the Federal Reserve’s actions will remain the most impactful. Yet the combination of diverging global policy paths and rising political sovereignty highlights that market dynamics are now far more nuanced than the simplistic “Fed rate cut equals good” narrative.

In this environment, we would expect the range of potential market outcomes to broaden. While this may initially sound unsettling, it could (as last year perhaps demonstrated) expand the opportunity set available to investors.

In this month’s blog we highlight a few areas of the market that seem to be moving away from investor obscurity to areas of potential interest.

Japan: No Longer Standing Apart

For decades, Japan stood apart from other developed economies, characterised by persistent low inflation and ultra-accommodative monetary policy. However things are shifting, Inflation has re-emerged for the first time in a generation, prompting the Bank of Japan to cautiously adjust its long-standing policy stance. In addition, we have seen some big shifts politically with a new, well supported, prime minister.

While rate increases in Japan remain relatively modest by global standards, their significance lies in the regime change they represent. Japanese bond yields, currency dynamics, and domestic equity leadership are all being reassessed by investors who had long viewed Japan as structurally different and, at times, easy to overlook.

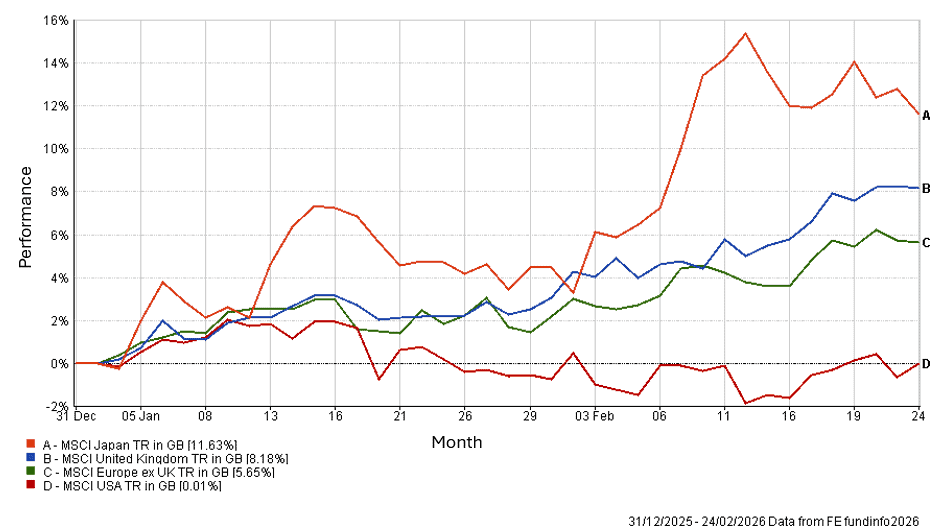

The chart below shows how quickly the situation can reflect in markets, and this year Japan has been one of the best performing developed regions, despite making up less than 6% of the global benchmark. A lot of change yes, but opportunity too.

Year-to-Date Returns: Japan vs Developed Markets

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends.

Dollar Weakness: Tailwind to Headwind

For investors outside the United States, dollar weakness can act as a headwind to returns. Even when underlying asset performance is positive, currency effects can erode gains. This has been especially relevant for UK-based investors with substantial US equity exposure over recent years.

The move also challenges a widely embedded assumption of the past decade namely, that dollar strength would persist alongside US market leadership. This has begun to be reassessed, and we have seen the start of a reallocation of investor capital to a broader collection of regions/ currencies.

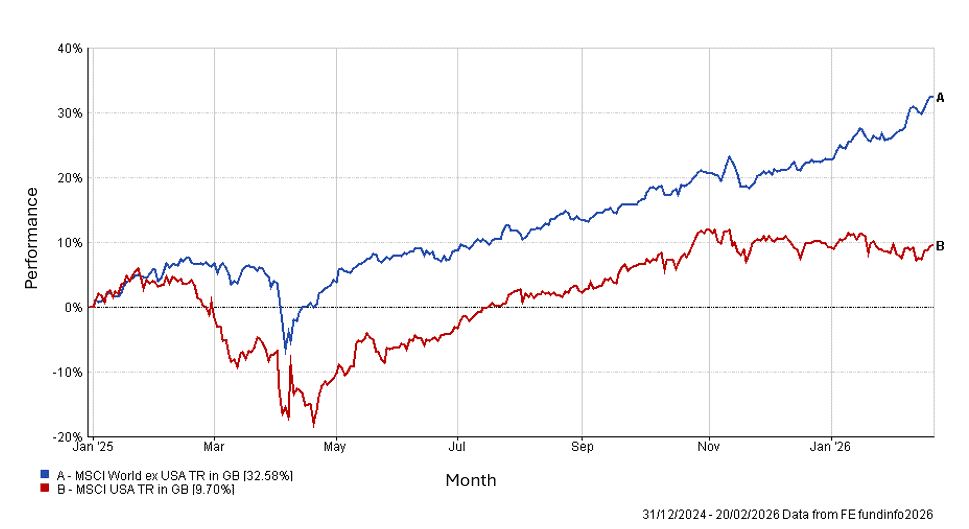

As such we have seen the US underperform a broad basket of global equities in sterling terms. This has been particularly prominent from 2025 to date where the US has underperformed the rest of the world by circa 23%. Something which seemed to many to be implausible only a couple of years ago.

US vs the Rest of the World

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends.

Real Assets: Commodities Rare Earths & Emerging Markets

In the years following COVID, investor enthusiasm gravitated heavily toward digital assets, software companies, and asset-light business models (think the Mag 7). Meanwhile, traditional real assets like commodities, energy producers, and materials, often received comparatively little attention.

However, with the rapid expansion of AI capabilities and the infrastructure required to support them, has sharpened focus on the physical foundations of the digital and real world economy. Commodities are once again being recognised as strategically important, not only economically but geopolitically. Regions like Asia and Emerging markets are once again in the spotlight. Interestingly, many of the asset-light business models have turned into much more capital-intensive businesses due to their need for rare earth resources.

Recent tensions involving resource-rich regions have reinforced how critical energy security and raw material supply chains have become. Many nations are now prioritising the resilience of their energy and resource bases.

We won’t go into it in any detail here but Gold provides a notable example. After an extended period of muted performance, it has delivered strong returns as investors seek diversification, inflation protection, and non-correlated returns in an environment where uncertainty has undoubtedly increased.

Property & Infrastructure: Signs of Recovery

These assets are inherently sensitive to interest rates given their income-oriented characteristics and really came under fire in the sharp rise in yields during 2022. That combined with the bleak outlook for parts of the real estate market during COVID, has weighed heavily on valuations for several years.

As a result, however many areas of the listed property and infrastructure market look inexpensive relative to history and whilst rate cuts may be less synchronised globally, they are likely to be positive for the sector.

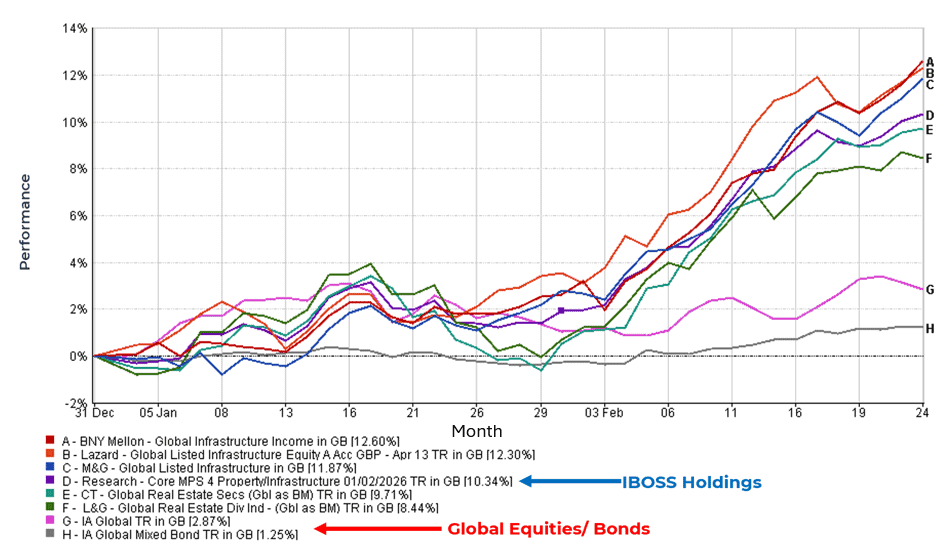

As with other assets mentioned in this blog these once-ignored assets have the potential to move quickly. A point evidence in the chart below where many infrastructure and real estate funds saw close to double digit gains in February this year.

Listed Property and infrastructure 2026

Source: FE Fundinfo

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends.

Closing Thoughts

Ultimately things are changing and whether we are talking about Central bank policy decisions, Geopolitics or investment portfolios we feel that the range of potential outcomes are broader than they have been for quite some time. While this increased dispersion can feel unsettling, it is not inherently negative, and periods of uncertainty often create new opportunities alongside new risks.

That said, in this environment we favour diversification and active decision making, irrespective of your flavour of investment, whether it be Active, Passive, or even sustainable. We believe that flexibility is key and those that rely too heavily on a single story or theme may well come unstuck. The examples above hopefully illustrate just how quickly conditions can change.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 66.2.26