Over recent months, we’ve looked to outline a handful of exciting investment opportunities for investors. We began our journey by looking into the prospects for emerging markets and China before diving into the less headline-grabbing, but no less compelling, world of fixed income.

We aim to conclude the trilogy this month with a closer look at the more familiar but equally exciting region: UK equities. The UK was recently dubbed as “the next Silicon Valley”, and while many investors initially reacted to the suggestion with scepticism and, in many cases, outright disbelief, there are plenty of reasons to be optimistic about the prospects of old blighty.

The Great British Back Off

Over the years since the Brexit referendum, UK equities have had their fair share of ups and downs, reflecting the fluctuating economic conditions, geopolitical developments, and unique make-up of the UK’s largest firms. Whilst the drivers of change have varied over the years, they have all contributed to the same thing – increased uncertainty. Uncertainty can be particularly damaging as companies and investors cannot plan or forecast with any clarity; therefore, the perceived risks of future investments increase.

One bout of uncertainty occurred when the UK looked to back away from the perceived centralised power of Europe and Brussels, as many considered that the French and German power bases directed the decision-making. Since then, we have witnessed further political divergence as many European countries have some elements of the far-right on their ballot papers that look to champion a nation-first agenda.

Ironically, when the UK voted to leave the EU, there was much talk about a new wave of nationalistic and protectionist policies that could be introduced into UK politics. These elements of populism continue to cause uncertainty for Europe, including the Netherlands, France, Germany, and Italy, who all find themselves under more significant pressure from factions and sectors within the respective countries to put their own interests above those of others.

As an example of how this is being perceived, Bloomberg ran the headline this week – “Popularism Is Scaring Away Big Businesses in The Netherlands”.

However, with our referendum retreating in the rearview mirror, the UK is heading in the general direction of a ‘soft-left’ government and increasingly seen as more benign. This is in stark contrast to the era when there was potential for a Jeremy Corbyn led labour government and the perceived negative impact of less business-friendly policies caused genuine concern at a corporate level. Again, the fog of uncertainty seems to have cleared somewhat here as the UK begins to benefit from the political stability of two broadly centrist parties battling it out at the general election.

It is worth considering that it is not always what a country does itself; rather, its position relative to others that can alter perceptions of risk and uncertainty.

The Stock Market is Still Not the Economy

Investors withdrew £14 billion worth of UK equity assets in 2023, marking the eighth straight year of net outflows. These withdrawals were consistent throughout the year as investors sold out of UK equities month on month. The biggest sellers were retail investors, equating to £10.18 billion outflows. Retail investors were instead buying into the perceived safety of the IA Volatility managed and IA Short-Term Money Market sectors – the latter saw net inflows of 2.2 billion last year alone.

It seems somewhat surprising then that with such a negative backdrop the UK Equity Market Index reached an all-time high in February 2023, underscoring a moment of significant strength within the market whilst the public perception of UK plc bumped along the bottom. This peak reflects the dynamic nature of the market and once again shows areas of robust performance even in the face of broader economic challenges. It is often said that the stock market is not the economy, but it is equally valid that markets don’t necessarily reflect the mainstream media’s view of a country. As a further example, in recent weeks, we have witnessed many European markets hit all-time highs whilst having sluggish economic backdrops and outlooks clouded by geopolitical headwinds and wars.

So, is the UK market currently being overlooked?

Significant Periods

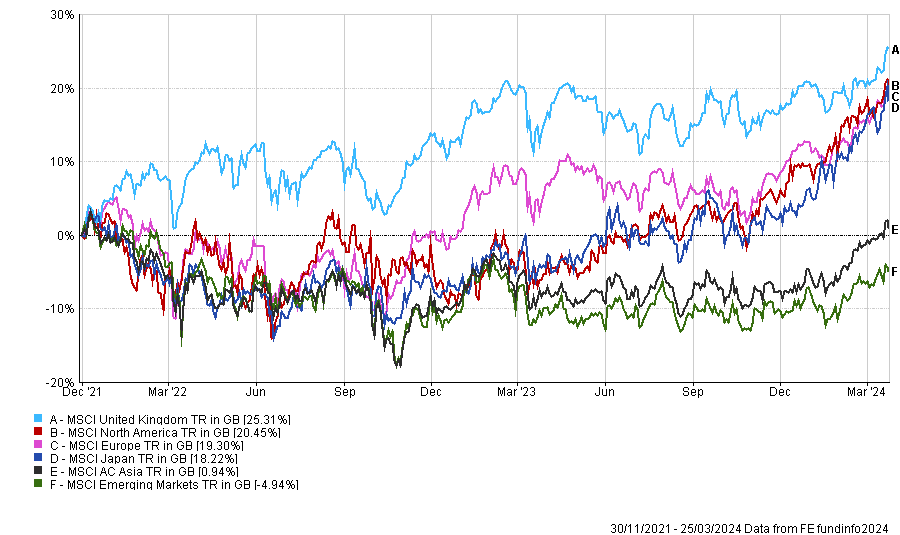

For significant periods since the turn of the year, the UK has been held back by its lack of tech stocks and relatively high exposure to some of the more defensive sectors, such as basic materials and telcos, which have often been underperforming. Year to date, the MSCI UK Index has underperformed much of the developed world. Calander years, just like rolling cumulative periods, might interest some investors but shed little light on the bigger-picture or why and how they were achieved. Market conditions can often be grouped within specific dates, and we find focusing on periods within important market-moving events or central bank decisions considerably more enlightening.

The example below covers the period since The US Federal Reserve finally woke up to the dangers of inflation and abruptly started raising interest rates at record speed. This period is important because until then asset prices were being valued on the assumption that inflation wasn’t an issue and that interest rates would stay lower for longer or perhaps forever. This failure by the Fed to understand inflation dynamics and their powers to control them laid the foundations for the global bond rout and asset prices to be re-evaluated globally.

When we look at funds, what was achieved in the period leading up to Powells inflation epiphany is of limited value as those market conditions will be unlikely to be repeated ever again.

MSCI UK Versus Selective Markets (1st December 2021 to 25th March 2024)*

Data source: FE Analytics

Data source: FE Analytics

The British ISA

Earlier in the month came the announcement of the Spring Budget, where Jeremy Hunt stated that the UK was on its way to becoming its own Silicon Valley for tech development and included the launch of the ‘British ISA’, which will allow an additional £5,000 annual investment for investments in UK equity with all the tax advantages of other ISAs.

The announcement of the British ISA might help offset the pervasive negative sentiment, stretching back to the vote to leave the EU. While talking about Britain becoming the next Silicon Valley remains just that: talk, any announcements highlighting the opportunities in the UK will be welcomed by British businesses.

You may not immediately consider the UK a global innovator; however, the UK ranks 4th in the Global Innovation Index, just behind the US but ahead of Singapore and Germany. So, while Jeremy Hunt’s comparisons to Silicon Valley may indeed just be talk, there is some basis for comparison.

Whatever the effects of the announcements made in the budget, we remain bullish on UK stocks. As old-school globalisation continues to retreat, we expect new winners to emerge, and the UK, with its history of entrepreneurship, is potentially one of them.

Attractive Valuations

One of the core reasons for our positive outlook on UK equities is the attractive valuation of many companies. Compared to their global counterparts, UK stocks are, on average, trading at a discount, with their price/earnings ratio now close to 40% lower than the rest of the world.

This undervaluation presents a unique opportunity for investors to gain exposure to high-quality companies with strong fundamentals, positive cash flows, and solid dividend yields at a lower entry point. The value proposition is particularly compelling in the financial services, energy, and consumer goods sectors, where several companies stand out for their resilience and growth potential.

Overall, the domestic economic outlook is also looking somewhat better, and we believe after a fairly dismal couple of years, small and mid-cap stocks are best positioned to benefit.

Conclusion and IBOSS Positioning

After their prolonged procrastination and woeful inactivity, the Bank of England’s monetary policies have finally stabilised inflation, further enhancing the favourable backdrop for UK equities.

Moreover, the current geopolitical and economic environment underscores the importance of diversification. With the UK’s unique mix of domestic and international companies, UK equities offer a natural hedge against geopolitical risks and currency fluctuations. This diversification benefit is particularly relevant as more extremist, protectionist and nationalistic policies emerge from many of our trading partners, and where investors will seek stability and growth in equal measure.

At the same time, the UK’s commitment to sustainability and corporate governance is increasingly reflected in the equity market. UK companies are at the forefront of adopting environmental, social, and governance (ESG) practices, driven by regulatory changes and investor demand. This shift mitigates risks and opens up new investment opportunities in companies leading the way in sustainability, which is increasingly a criterion for investment selection among forward-thinking investors.

So, all in all, we remain bullish on UK equities, as we have for some time. Our current UK stable of funds comprises Artemis UK Select, BNY Mellon UK Income, WS Gresham House UK Multi Cap Income, Man GLG Income, Polar Capital UK Value Opportunities, Fidelity UK Smaller Companies, and the L&G UK 100 Index Trust. This combination gives us diversification across investment styles and market-cap whilst harnessing the alpha generation of some of the best stock pickers in the UK market today.

While risks and uncertainties exist in any investment landscape, the UK market’s current conditions and underlying fundamentals present a compelling case for inclusion in any investment portfolio.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 76.3.24