As the year comes to an end, we thought it a good opportunity to pull together a selection of real life queries we have had more recently from advisers and their clients. From the AI bubble to decumulation, hopefully there is a little bit of something for everyone here, but if you have any specific queries please do get in touch with the team.

Markets have performed incredibly well this year, and I am worried about a potential market crash/ pullback.

We all know that time in the market is more important than timing the markets, and potential pullbacks can in fact act as good buying opportunities for patient investors.

That said, defending capital in falling markets is vitally important both for keeping clients on the journey and for delivering attractive long-term returns.

Fortunately, the IBOSS portfolios’ focus on maintaining a diverse range of assets has historically delivered strong defensive characteristics across a variety of market conditions.

The chart below illustrates these characteristics for the IBOSS MPS Core 4 compared to the benchmark since IBOSS’ launch in 2008. It is important to note that the benchmark consists of other multi-asset funds operating at a similar level of risk.

Defensive Characteristics Since Launch (01/11/2008 – 31/10/2025)

Source: FE Fundinfo

- Higher returns with lower risk: IBOSS MPS Core 4 has delivered higher returns while maintaining a lower level of volatility compared with the benchmark.

- Shallower drawdowns: Both the Maximum Drawdown and Maximum Loss figures show that portfolio declines have been less severe than those experienced by the benchmark.

- Lower sensitivity to market falls: The portfolio’s Beta and Downside Risk metrics demonstrate that IBOSS MPS Core 4 has tended to be more risk-averse, resulting in fewer and smaller negative periods for investors.

Real world Examples:

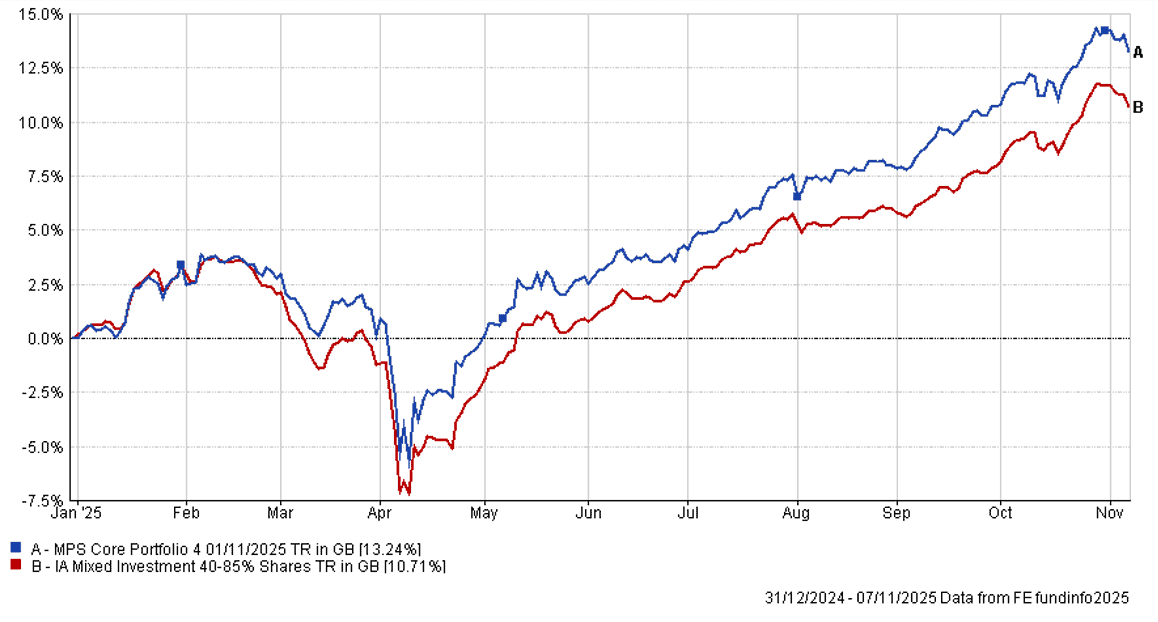

Market Pullback 2025: Liberation Day

This year markets fell abruptly on the back of mounting concerns surrounding US Tariffs and trade negotiations. One of the most heavily impacted areas were US equities which fell circa 22% from the end of January to the middle of April whilst global equities more generally saw falls of circa 18%. The IBOSS portfolio fell 5% over the same period and the benchmark fell 7.5%.

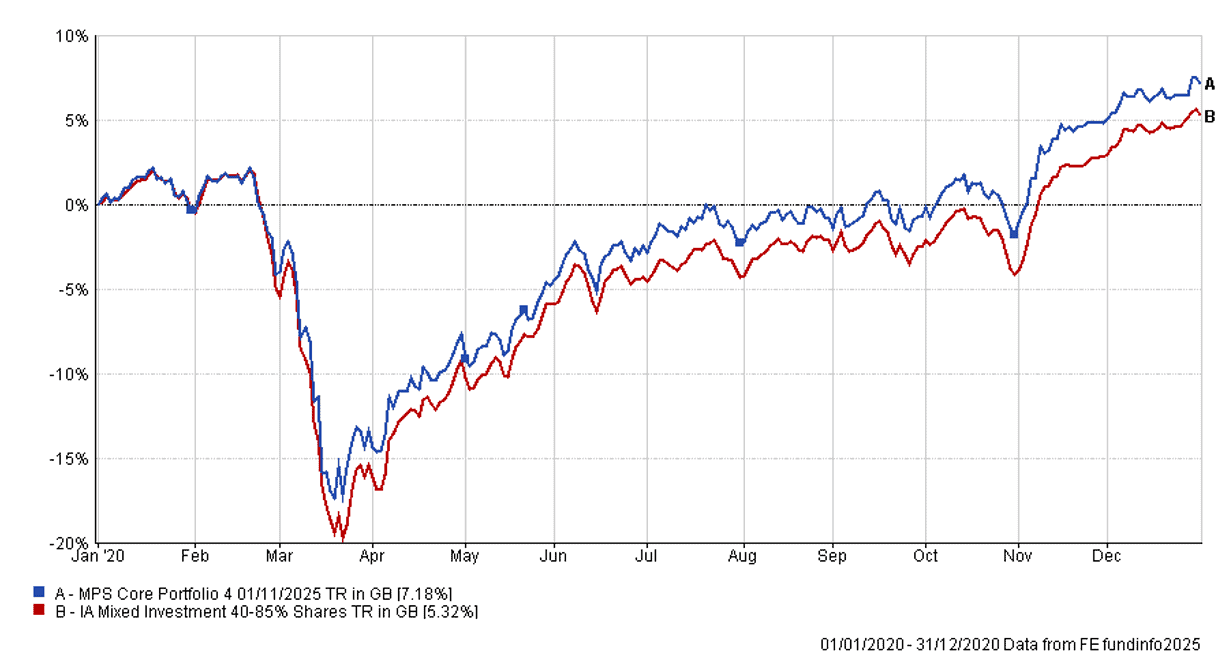

Market Pullback 2020: COVID-19

The epidemic saw investments fall across a broad selection of risk assets. Peak to trough, global stocks & shares fell on average 26%, the Benchmark fell 21% and IBOSS MPS Core 4 fell 19%.

In each case the portfolios were rewarded (on a relative basis) for holding a more diverse range of assets.

I understand IBOSS has good defensive characteristics but what about clients with more appetite for risk, are they missing out on potential returns?

Though we are aware that IBOSS has a reputation for performing well in more volatile or difficult market conditions, it is our firm belief that a fully diversified approach to investing can open a portfolio to a broader range of potential opportunities.

Hopefully this is borne out through longer-term data, which shows that all IBOSS MPS Core and Passive portfolios have outperformed their respective benchmarks since launch over more than 17 years (for Core).

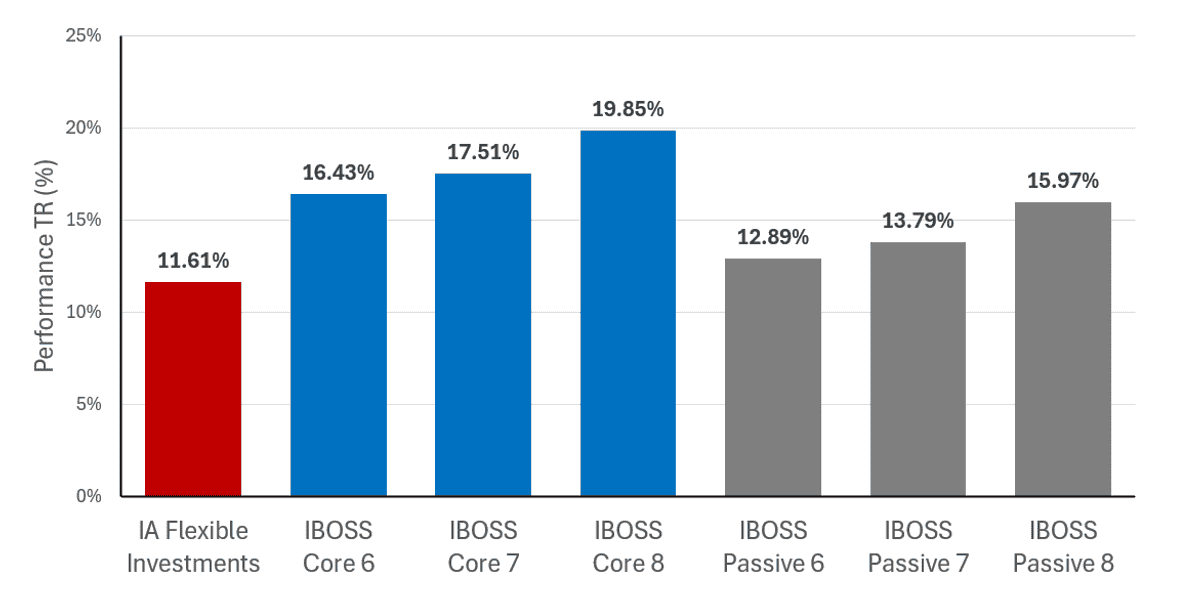

However, this year is another great example of how diversification can be beneficial in a rising market.

The chart below shows the returns of our higher risk portfolios against their benchmark this year. This outperformance has been driven by a combination of asset allocation and a broader exposure to global equity markets, including emerging markets, Europe and the UK.

2025 Performance – Higher Risk Core/ Passive Portfolios

Source: FE Fundinfo

Active management seems to have made a comeback, but passives still look superior over 5 years. Which should I invest in?

We have received a variety of these queries this year, and whilst we could discuss the benefits and drawbacks of both investment styles forever, we are ultimately agnostic over the long term as long as you remain diversified.

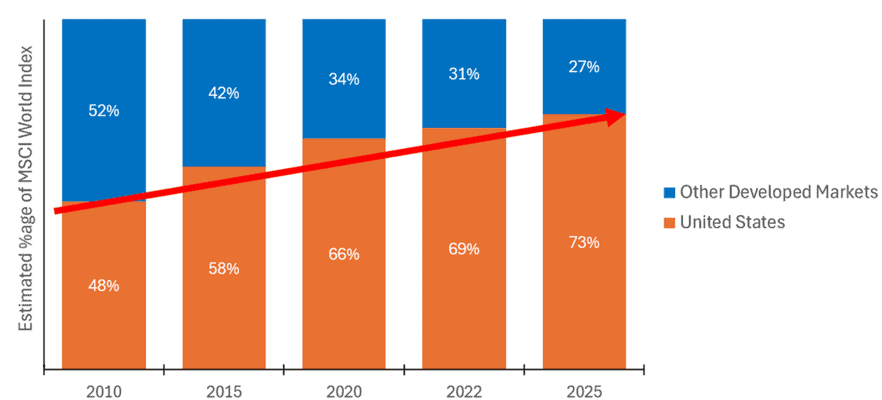

As the chart below shows, the US has become an increasingly large part of the global equity index. So much so that it is hard to argue that the index represents a broad basket of global stocks, particularly because 10 companies make up more than 30% of the index. This concentration risk is one that we feel must be actively managed irrespective of your bias toward passive or active.

MSCI World – US weighting over time

Source: FE Fundinfo

We have recently launched our blended range, which combines our Passive and Core MPS ranges. Interestingly, advisers have been moving away from Passive and toward the Blend, perhaps indicating that many feel as we do that active managers might currently have the edge.

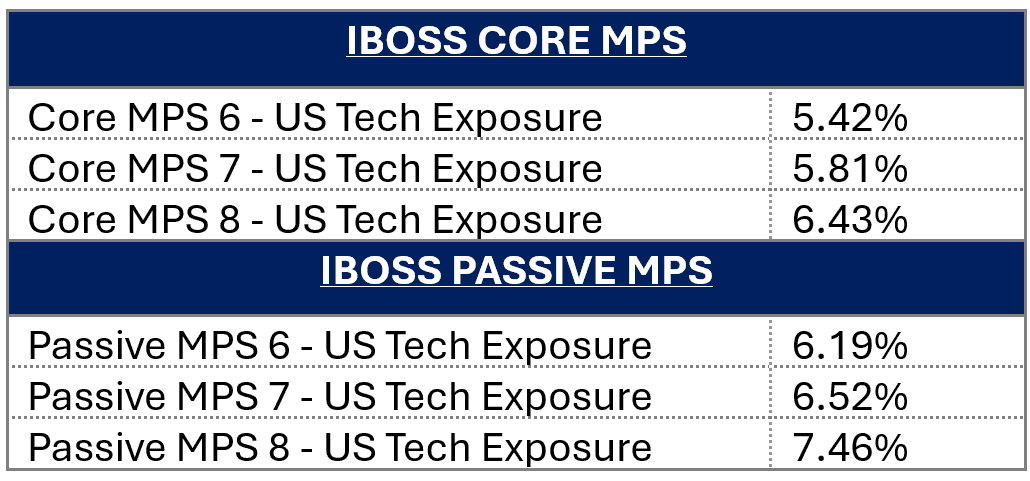

With all the talk of a potential AI bubble, how exposed am I in the IBOSS portfolios?

It is no secret that companies involved in AI-related technologies have seen some strong returns, no more so than the poster child of all things AI: NVIDIA.

However, with valuations reaching all-time highs and NVIDIA becoming one of the largest companies in history, many end clients and advisers have asked this year how exposed we are to the area.

The chart below demonstrates our exposure to US tech for the portfolios with a higher equity content.

As you can see, each portfolio still has a meaningful position in this more exciting area of the market but is unlikely to be fully dictated by the success or failure of one industry.

US Technology Exposure – November 2025

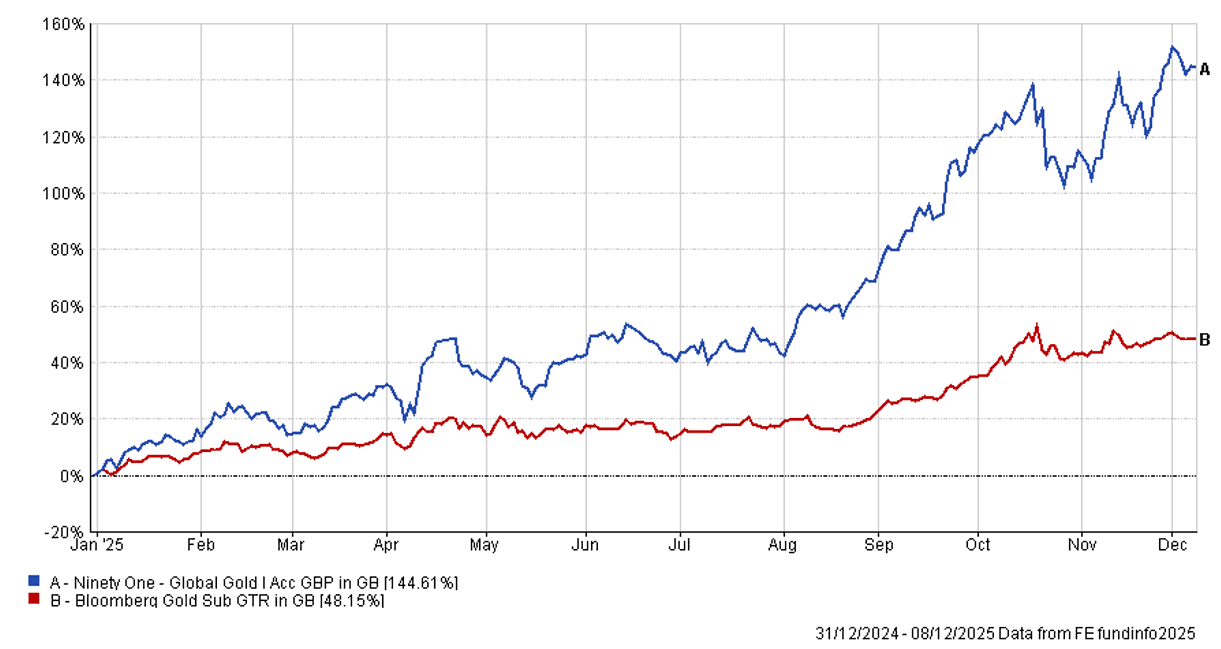

IBOSS does not seem to have any investments in gold despite the continuing good performance of gold.

The IBOSS portfolios have gold exposure through the Ninety-One Global Gold Fund, JPM Natural Resources Fund and Troy Trojan Ethical Fund. This exposure is primarily via gold miners and related assets rather than direct gold, though the Troy fund holds around 12% in a gold ETC (direct gold).

Gold miners generally track gold prices over the long term but with greater volatility. Given our modest 1–2% allocation, we can tolerate this volatility, and even a small position in gold miners can have a meaningful impact on the portfolio’s return.

The chart below compares the performance of the Ninety-One Global Gold Fund with the gold price year to date.

Looking ahead, we anticipate that the forces supporting gold’s recent performance, including heightened geopolitical risk, dollar weakness and robust central-bank demand, will persist.

Year to Date performance to 08/12/2025

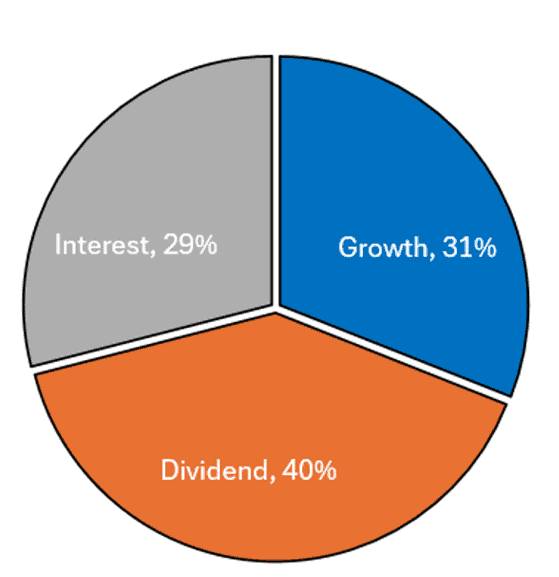

Why do I need a Decumulation portfolio when a growth portfolio should suffice to meet withdrawals?

The Retirement Income Advice Review made one point very clear: decumulation is fundamentally different from accumulation. While that does not automatically rule out growth-orientated solutions for clients drawing an income, it does mean we must assess suitability through a different lens, one that places greater emphasis on sequencing risk, sustainable withdrawals and the stability of returns.

Considering many of these characteristics exist within our core range through low volatility and historically reduced drawdowns, advisers have asked why a specific decumulation portfolio may be necessary.

In short, our decumulation range looks to provide an attractive yield, and as such offers a more diversified return stream than a strictly growth portfolio. The chart below demonstrates how returns have historically been delivered for IBOSS MPS Decumulation 4. In short, if growth dries up, then there are other means of generating returns, a factor which can soften drawdowns and help limit the impact of a sustained bear market. This is something many investors have not had to think about for the last decade but is ultimately one of the biggest risks for decumulation clients.

For more information on our decumulation range, please contact a member of the team.

Return profile – IBOSS MPS Decumulation 4

Source: FE Fundinfo

Where are you positioned going into 2026?

2025 has been an exceptionally rewarding year for investors with well-diversified portfolios. As illustrated in the chart below, the divergence in performance across different asset classes has been significant, and it would have been difficult at the start of the year to predict which areas would outperform.

IA Sector Performance Year to Date (to 30/11/2025)

Source: FE Fundinfo

Looking ahead to 2026, we expect investors to continue to be rewarded for diversification as global uncertainty remains high. As a result, investors can anticipate a similar approach from IBOSS: one that remains focused on broad diversification, risk management and the ability to participate in growth across a wide range of markets and asset classes.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

We provide the DFM MPS as both distributor and manufacturer. Details of our target market assessment can be found in our compliance investment procedures, available upon request. Each fund will be assessed independently, but it is highly unlikely that any one fund held in our portfolio will meet the target market in isolation—detail of why the inclusion collectively will be suitable is included within our research. The DFM MPS performance and displayed underlying portfolio charge is produced using the preferred share classes, this may differ from platform to platform and is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited, registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 361.12.25