Few people would question China and India’s economic rise over the last few years, but what’s next for the world’s second and fifth largest respective economies and, more importantly to us, the investment opportunities?

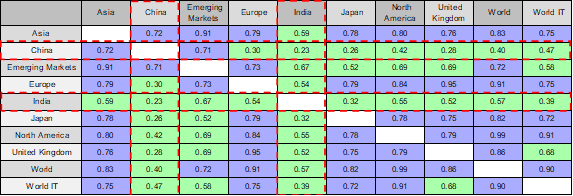

Well, for a start, it is becoming increasingly apparent that due to China and India’s mixed economies, i.e., ones based on both command and free-market components, Chinese and Indian equities offer a significant degree of diversification (fig.1). This is somewhat ironic because the Fed leads the equity market around by the nose in the US. Yet, historically, the US equity market would be described as ‘free’, and the economy the living embodiment of free-market principles.

MSCI DEVELOPED MARKETS 3 YEAR CORRELATION TABLE (fig.1)

The Chinese government has recently demonstrated their willingness and ability to bring to heel their tech behemoths and their entrepreneurial leaders. The last-minute cancellation of the eagerly anticipated Ant IPO after the Chinese regulators had so recently approved it showed the determination of the government machinery to do things their way. Markets wobbled in China and Asia more widely as participants came to terms with such unprecedented actions but overall, they remained pretty resilient. Contrast with what might have happened if, say, the US if regulators had stepped in to stop such a launch at the behest of the government. Of course, we cannot say for sure because it has happened (yet), but our best guess is it would have caused market carnage.

MSCI INDIA & CHINA VS MSCI WORLD 21 YEAR PERFORMANCE CHART (fig.2)

Investing in India brings its own distinctive elements, but again, as shown in the table (fig.1), it has excellent diversification benefits as measured by 3-year correlation. The correlation is particularly low against China (0.23), but even against the broader MSCI World index (0.57), it has considerable merit as a diversifier. Between them, these two economic powerhouses are on numerous issues experiencing ongoing political disputes. The merits of investing in both countries, however, remain clear with almost unequalled growth potential. Although the relative returns have varied considerably for sustained periods, the outcome over the last two decades has been outstanding.

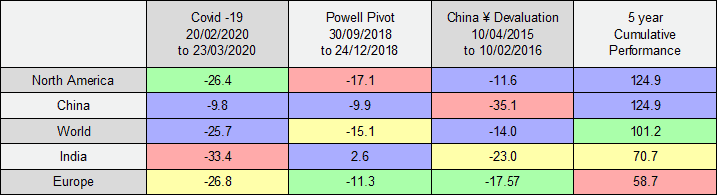

From a pure investment perspective, what many see as government interference in issues such as currency or anti-trust matters can mean the respective economies and stock markets of countries such as China and India can perform differently to say the US, UK and mainland Europe. In these more developed economies with longer-standing political structures, although the government does play a role in market developments, it has really been all about the role and actions of the central banks for the whole of the last decade. As shown in the table (fig.3), during the previous three market drawdowns, it is not necessarily the more developed markets that offer the most protection.

MSCI SELECTED COUNTRY PERFORMANCE AND DRAWDOWNS (fig.3)

To summarise, we believe there is merit from both growth and diversification angles by investing in India and China as a part of our global equity allocation. Not only are there significant opportunities per se, but an investors journey can, during many periods, actually be smoothed by adding these idiosyncratically volatile countries.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients. It does not purport to be all-inclusive or contain all of the information which a proposed investor may require in order to make a decision as to whether to invest or not. Nothing in this document constitutes a recommendation suitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 145.4.21