China has investors scratching their heads. Is it better to sit it out, or are valuations so low as to make it an opportunity not to be missed?

We recently introduced China-specific funds into more portfolios, which has prompted client and adviser questions about the investment case for China. The issues and opportunities of investing in the world’s second-largest economy are complex and ever-evolving.

Our Core portfolio range aims to beat the relevant benchmark over as many periods as possible, with less than benchmark volatility and lower drawdowns, across all risk ratings. After winding down the regulatory crackdown (for now at least) and because valuations have fallen so far in China, we think it is sensible to include some explicit holdings within our portfolios.

To explain our decisions clearly and to assist you with similar client concerns regarding China, we have put together a series of bullet-pointed notes that outline our reasons why China, and why now?

- China has the second-largest economy in the world, after the US, when measured by nominal GDP.

- Due to rising incomes and steady wealth creation, living standards in China have improved significantly. Moving beyond the basic necessities, people are willing to pay more and upgrade to premium goods and services. This leads to strong growth and higher revenues for Chinese consumer companies.

- Chinese companies across the board have been investing in research and development (R&D) to move up the value chain. Improved technological capabilities can lead to better quality products or more efficient processes, which generally means higher profits.

- Compared to global peers, industry leaders in China are only a fraction of the size.

Additionally, many Chinese companies are becoming more competitive in the overseas market and are gaining market share. This suggests that Chinese companies have the potential to grow much larger over time.

- It is in the process of cutting interest rates as opposed to the developed world raising them because China is in a different part of the economic cycle.

In broad terms raising interest rates is bad for risk assets and cutting rates is supportive of them.

In addition, China is starting to ease regulations in certain sectors to boost growth, which should be supportive of risk assets though this is never guaranteed.

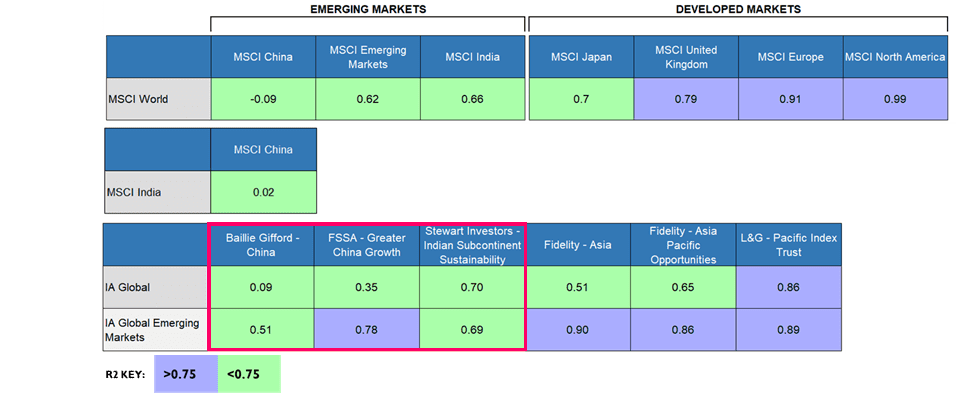

- China (and India) have very low correlations to other global equities (fig1). This means Chinese equities often move either in a different direction from other global equities or with a China-specific level of magnitude.

Assets with a low correlation to global equities have become increasingly rare, but opportunities for diversification can still be found outside of developed markets.

FINDING DIVERSIFICATION IN EQUITIES | THE BENEFITS OF INDIA & CHINA EQUITY MARKETS (fig 1)*

3 YEAR CORRELATION DATA TO 31/07/2022 | source: FE Fund Info

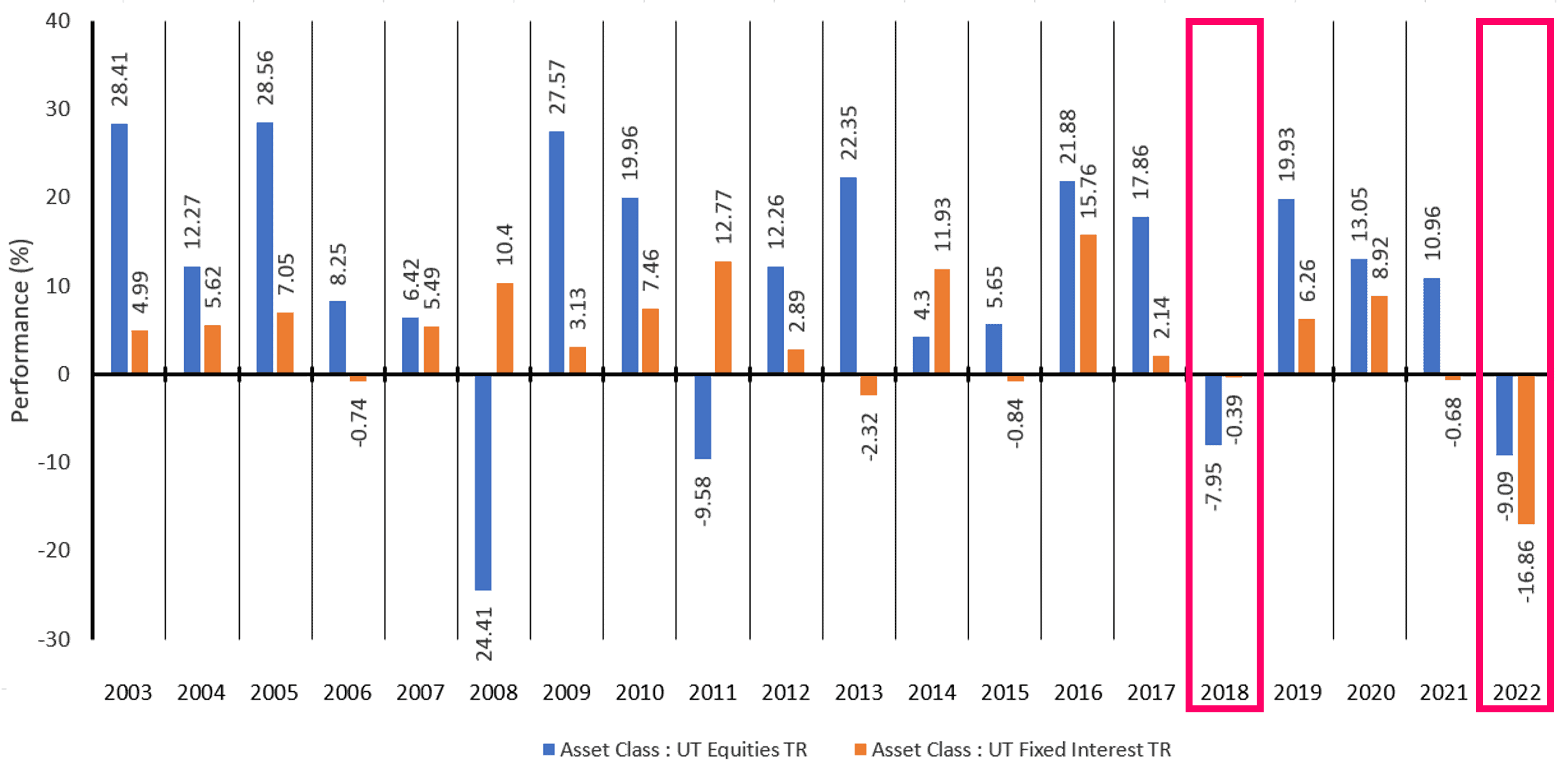

- Non-correlated assets have become increasingly hard to find as central bank policies have driven both bond and equity performance in the same direction (fig 2).

BONDS & EQUITIES | UNPRECEDENTED TIMES (fig 2)

DATA TO 31/08/2022 | source: FE Fund Info

- The Chinese economy has been faltering for some time, and with the so far muted response from the authorities, a good deal of bad news is in the price of some Chinese assets.

- As long-term investors, we concentrate on the factors that will likely be positive in the coming quarters and years and not necessarily in the next few weeks. We think the above points will collectively act as supportive tailwinds to Chinese risk assets.

- We remain mindful of several risks to our positive thesis on China’s assets but would note that all investment comes with a degree of risk.

For example, holding a large amount of cash as a UK investor with our own Bank of England forecasting inflation to hit 13% carries an obvious risk.

Many US assets are now back to elevated price levels, which could leave them susceptible to market corrections in an era of rising interest rates.

In the case of China, we see the three main risks:

- A continuing failure of the Chinese authorities to either develop an effective covid vaccine or a policy where draconian lockdown policy can be avoided.

- The leaders, in whatever guise, fail to back up their more market-positive rhetoric with hard policy support.

- The situation with Taiwan escalates and affects China’s and other nations’ trading policies. For example, it is estimated that over $3trillion of trade passes through the Taiwan Straits each year. Although a blockade or worse would harm international trade, it would also considerably impact China’s economy.

- So, in summary, we believe an allocation to China is prudent from a diversified portfolio perspective and a pure investment opportunity. We are aware of the risks as we see them, but we must also be mindful of the opportunities.

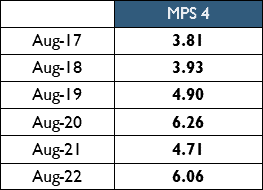

- It is important to highlight that whilst we have increased our use of explicit China funds, the country still only makes up 6.06% of our Core MPS portfolio 4 (as of August 2022). To put this into perspective, our current North American holdings in the same portfolio are 11.57%.

The weighting of Chinese holdings over the last five years for Core MPS portfolio 4 can be seen below.

China & Hong Kong exposure (%) | source: fund houses

*Some information displayed may be short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years. Past performance is not a reliable indicator of future performance, please refer to our important information for a full list of risk warnings.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same group, Kingswood Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 224.8.22