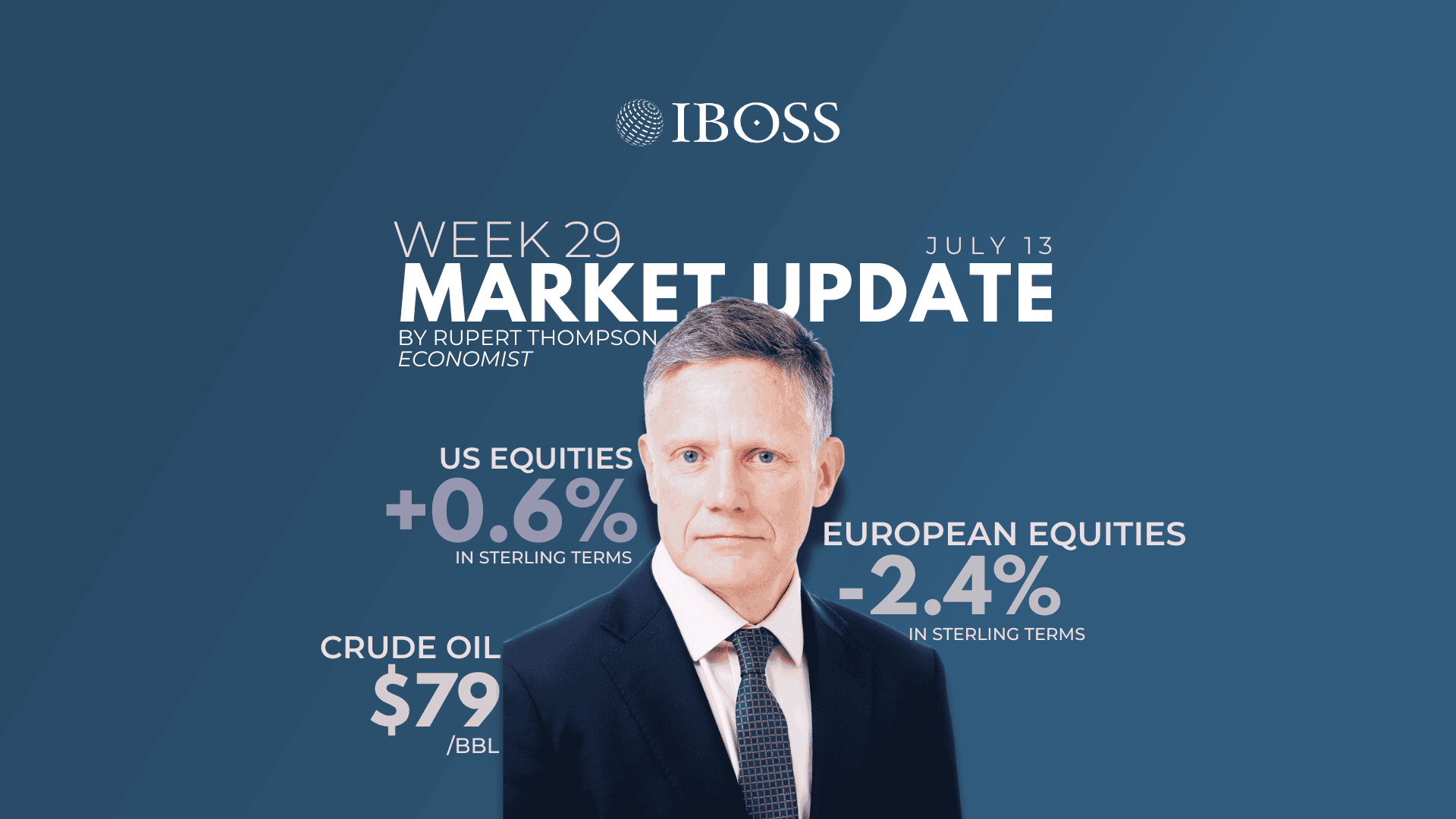

Global equities were little changed last week, gaining 0.2% in local currency terms and edging down 0.1% in sterling terms. The US outperformed with a gain of 0.6% in sterling terms, helped by its relative insulation from the renewed conflict in the Strait of Hormuz and strong gains in some US tech stocks.

Other regions, by contrast, saw losses with the UK and Japan both down around 1.5% while Europe and Emerging markets were down 2.4% and 2.1% respectively.

The memorandum of understanding – or misunderstanding as it has been dubbed – between the US and Iran has come under renewed threat with the US and Iran engaging in further rounds of tit-for-tat retaliation, peace negotiations back on and then off again, and the Strait itself now closed according to Iran – but open according to the US.

Crude oil prices have duly unwound some of their decline with the Brent price back up to $79 per barrel from a low of $72 earlier in the month. But this remains a far cry from the highs above $100 seen earlier in the year. Even though the risk of a major re-escalation of the conflict has clearly increased, it still appears to remain quite low because it is ultimately in the interest of neither party to see this happen.

Rather, recent events just confirm how difficult it will be to reach a long-lasting peace deal. The most likely state of play going forward remains a partial reopening of the Strait with periodic flare-ups. Oil prices therefore look very likely to remain around current levels, some way above where they were pre-crisis but well below their highs.

Meanwhile, the tech sector continued to be a source of some volatility with the announcement of stellar results for some chip companies now being greeted with share price declines rather than rises, following the surge in their prices this year. Samsung, the Korean chip maker, was the latest to suffer this fate, echoing the performance of the US chip maker Micron the previous week.

Even so, areas of enthusiasm certainly remain within the tech area. The US listing of the Korean chip company SK Hynix went well and Nvidia and Meta also saw gains of as much as 8% and 15% last week.

On the macro side, it was a quiet week with the only event of note being the release of the minutes of the latest Fed meeting. These did nothing to dissuade the market from its newfound conviction that the Fed could well raise rates by 0.25-0.5% later this year. Along with the higher oil price, this led to government bonds yields edging up and US Treasuries and UK gilts both posting losses of around 0.5%.

Corporate earnings have been the big driver behind the strong equity performance seen this year and will be centre stage over coming weeks with the big banks kicking off the US second quarter reporting season on Tuesday.

The banks are expected to post excellent results on the back of a surge in investment banking fees, and the S&P 500 overall is also anticipated to see another quarter of strong earnings growth. Following an outsized 29% increase on a year earlier in the first quarter, earnings are forecast to be up 24% this quarter.

These strong earnings gains should continue to represent a favourable underlying tailwind for markets. That said, there are two reasons to believe equities could well see a further period of consolidation over the summer – global markets are little changed from their high in early June – before resuming their upward trend.

First, a lot of good news on the earnings front is now priced in, leaving markets vulnerable to any disappointments. We have already started to see this recently within the tech sector, as discussed above.

Second, the possibility or even probability that the US Fed will raise rates later this year means Fed policy is no longer the positive for markets that it has been over the last couple of years when it was cutting rates. In the past, the move to a more hawkish Fed has generally taken a few months for equities to digest before they resume their upward trend.

This week, Tuesday will be a big day for markets with the big US banks reporting, June US inflation numbers released and Fed Chair Kevin Warsh testifying before Congress. We also have Chinese second quarter growth numbers out on Wednesday. And then for the UK, there is a certain sporting event in Atlanta on Wednesday and May GDP data on Thursday.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.