At the risk of sounding like a broken record, the events of May 2026 have once again reminded us why we are investors, not traders.

If you spend your days watching the financial news, May felt like a rollercoaster. We saw sharp swings driven by the latest inflation prints, sudden shifts in geopolitical rhetoric, and the ongoing tug-of-war between high-flying tech valuations and the realities of a shifting global economy.

But when we step back and look at the underlying investment conditions, the narrative seems much clearer, the market landscape has fundamentally changed from the last decade, and the portfolios that win tomorrow are likely to look very different from the ones that won yesterday.

The End of the One-Way US Trade

For the better part of a decade, the recipe for market-beating returns was simply to buy US equities, specifically large technology companies, and ignore the broader opportunity set. That muscle memory is deeply ingrained in many clients.

However, as we moved through May, we saw a continuation of a trend that has been building since early 2025. The US exceptionalism trade is becoming more challenged. Under the current US administration’s shifting trade tariffs and inward-looking policies, the rest of the world has been forced to adapt and forge new alliances and look after its own supply chains.

This has created a tailwind for regions that have been unloved for years. We have seen sustained resilience in UK, European, and Emerging Market equities. This isn’t to say that the US can’t still perform well and shouldn’t be part of your portfolio (of course it can and of course it should) but perhaps some caution is necessary to ensure returns aren’t only generated by one very concentrated subset of the market.

Technology: The Difference Between a Good Theme and a Good Price

We cannot talk about recent market moves without addressing the elephant in the room – Artificial Intelligence and the technology sector.

May saw further volatility in the software and tech spaces. Make no mistake, AI is driving real, structural change across industries. But as we saw with the recent sell-offs in software-as-a-service (SaaS) companies, technological disruption creates losers as well as winners.

We are now entering a more precarious period for markets, characterised by a wave of high-profile IPOs. These listings highlight willingness among investors to pay extreme valuations for compelling growth narratives. However, when companies come to market already priced for near-perfect outcomes (despite significant uncertainties) they offer very little margin of safety for long-term investors and increase the risk of sharp repricing if expectations are not met.

In this environment it is our passionate belief that diversification becomes increasingly important, and a well-constructed portfolio should provide exposure to these more exciting names but also a broader opportunity set. The start of June demonstrated just how quickly things can change for some of these areas.

Fixed Income: No Longer Just “Attic” Material

Understandably, investors are still suffering from the trauma the bond market crash of 2022. However, circumstances have changed, yields are much higher and we may well be coming into an environment where bonds can make meaningful contributions to clients portfolio.

Throughout May, we saw fixed income step back into its traditional role as the portfolio shock absorber. With government and high-quality corporate bonds offering attractive yields. More importantly, if economic growth stalls or inflation decisively cools, these assets have the room to generate meaningful capital gains.

Important Takeaways

- Diversification is the only free lunch: By design a diversified portfolio will always have elements that are underperforming the hottest current trend. However, a key part of generating long term returns is ensuring that clients are not overly exposed to the downside when inevitably the hot trend cools.

- The “Rest of the World” matters again: The 2010s were dominated by the US. The latter half of the 2020s is shaping up to be much broader. Exposure to UK, Europe, Asia/Emerging Markets, and Japan is currently providing a necessary buffer against US volatility and geopolitical posturing.

- Yield is your friend: We are back in an environment where cash and fixed income generate an attractive yield. This takes the pressure off equities to do all the heavy lifting in a portfolio.

- Volatility is normal: Short-term shocks dominate headlines but rarely derail long-term financial plans. Time in the market remains infinitely more valuable than trying to time the market.

With these points in mind, we continue to tilt the portfolio to areas of future opportunity and ensure the portfolio maintains high levels of diversification. We remain of the opinion that one of the biggest risks to investors is investing using the rear-view mirror, rather than positioning toward future opportunities.

IBOSS Performance Update

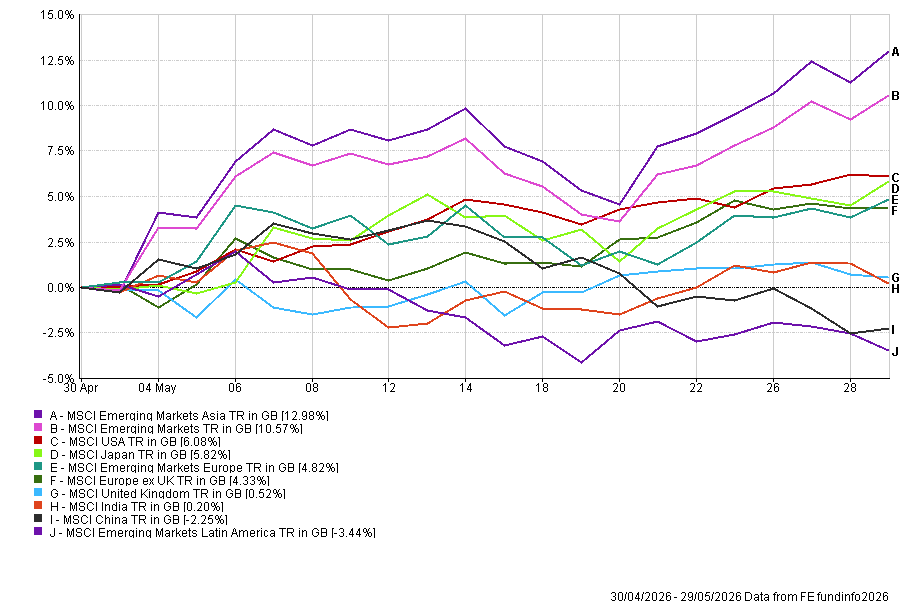

All IBOSS portfolios across the MPS range delivered positive absolute returns in May 2026, ranging from 1.5% to 4.5% across the risk spectrum. For the most part, portfolios with higher equity allocations performed best relative to their benchmarks, benefiting from a volatile but ultimately positive month for equities, led by Emerging Markets (despite a high dispersion of returns between EM regions, see figure below), as well as US and Japanese equities.

Active fund selection has continued to contribute positively to performance year to date, as reflected in the results. All Core and Decumulation portfolios have outperformed their benchmarks over this period.

Equity Indexes 1 Month Line Chart (Figure 1)

Source: FE FundInfo

The data presented covers a limited time period due to the context of this metric. Short-term performance may not be indicative of long-term trends. Investors should consider longer-term performance data and other relevant factors before making investment decisions.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Mattioli Woods Limited is registered in England and Wales at Companies House, Registered number 3140521.

Registered Office is: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.