What’s the purpose of a Benchmark?

As many of you are aware the IBOSS investment team has a borderline obsession with benchmarks. We use benchmarks to assess the performance and risk characteristics of our own portfolios, the portfolios’ underlying funds and any potential new funds. This may be an obvious point but identifying and measuring against a selection of truly relevant peers is, in our opinion, the best way to assess performance, risk and relative positioning.

Without going too far down the rabbit hole, many investors look to assess funds and portfolios through a variety of techniques – risk mapping, volatility targets, and asset allocation to name but a few. Though useful, many of these approaches are by themselves, in our opinion, potentially too inflexible and we contend there is as much art as science when it comes to investing. This is a pertinent point considering recent market movements. The relatively strong uptick in market volatility has broken through volatility parameters and inadvertently upped many risk-rated profiles for current clients – despite no real change to their portfolio or retirement goals. In the case of using asset allocation as a measure of risk the same problems have occurred. Those equity assets considered by many to be safe (e.g. developed market & income equities) underperformed and those considered relatively riskier saw limited drawdowns, especially Chinese and some emerging market equities.

Using a suitable benchmark and measuring the risk relative to that benchmark over time is, in our opinion, a potentially more suitable measure of risk and return. The benchmark changes to reflect market movements through time and the current average market positioning – asset allocation. In short, the correct benchmark should maybe demonstrate the market reality filtered by the changing mindset of peers instead of through an algorithm?

Benchmarks gone rogue

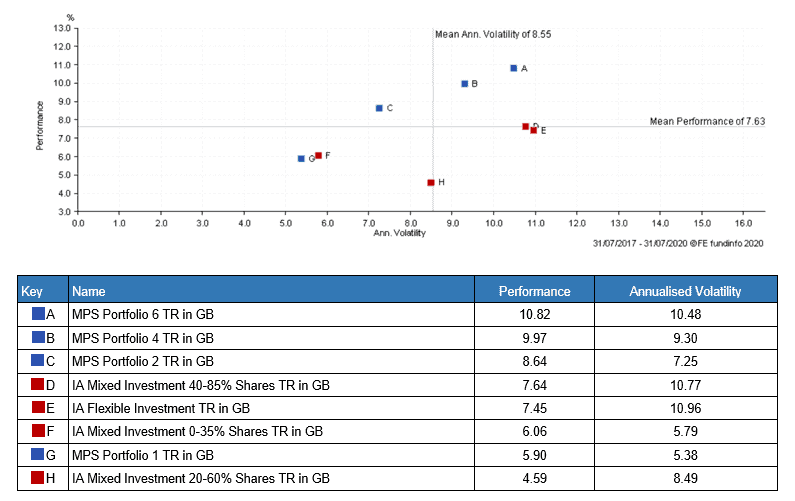

Considering our focus on the IA sectors used as benchmarks for our portfolios, we thought it worth highlighting the particularly strange shape of the benchmarks over the last 3 years. I have included the chart below as a basis for these comments.

Looking at the MPS portfolios you can see a very clear efficient frontier, with relatively equal distant performance and volatility spacing between the lowest risk IBOSS portfolio and the highest. The same cannot be said for the IA benchmarks, which have clustered together at the higher end of the risk spectrum and become fully detached at the lower end. So why has this been the case?

3 Year Scatter Chart – MPS portfolios against benchmarks

The Managed Portfolio Service (MPS) past performance figures include simulated performance to 1st November 2018. Simulated figures are based on the actual performance figures of the Portfolio Management Service provided by IBOSS Limited and is not a guide to future performance.

Source of data: FE Analytics

Why has the IA Mixed Investment 0-35% Shares performed so well?

Funds in this sector tend to be less influenced by movements in equity markets due to their relatively lower equity content. What this usually means then is that the fixed income position of the multi-asset funds have a much larger impact on total returns.

To answer the question most simply, the sector has performed very well on the back of large positions in Gilts and other Sovereign bonds, relative to the other sectors and other multi asset holdings. It is worth mentioning that Gilts have outperformed corporate bonds & cash by a relatively wide margin.

Performance table to 24/08/2020 – ranked within table

Past performance is not a guide to future performance.

Source of data: FE Analytics

Why has the IA Mixed Investment 20-60% Shares performed so badly?

This sector is by far the outlier; considering the rapid rebound in global equity assets and the relatively strong performance of fixed income assets, you would expect the sector to have performed well.

However, many of the funds within the sector have an overweight toward income producing assets as a way to increase equity content without (theoretically) increasing risk. As we discussed in our last blog, income producing assets underperformed considerably in the market fall, and have failed to take part in the equity market rally of recent months.

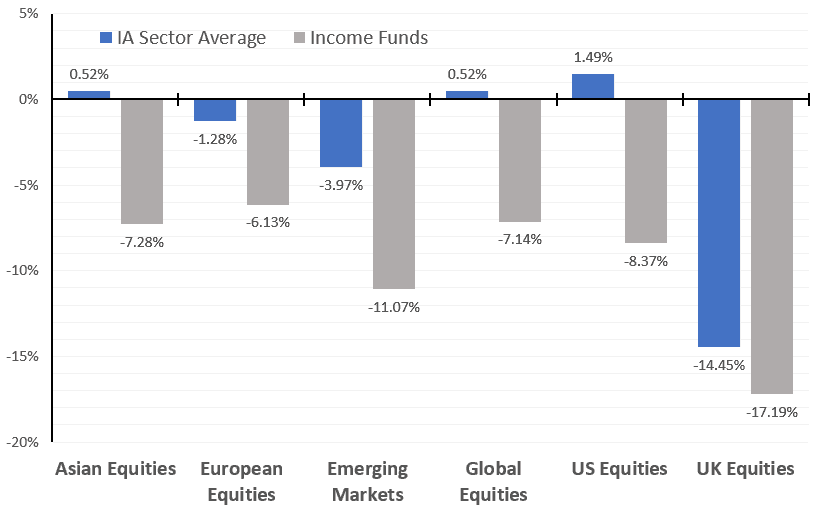

1 Year Performance of Equity Income funds vs IA sector average to 31/07/2020 – split by Geography

Past performance is not a guide to future performance.

Source of data: FE Analytics

In every geography the income constituents of each sector have underperformed the IA sector.

Why are the Medium & Higher risk benchmarks clustered together?

We have indicated for some time that we have become increasingly concerned with the shape and content of an average “medium risk” client’s holdings. The clustering together of both the higher risk benchmark and the medium risk benchmark suggests to us that investors that are looking for a more balanced portfolio have, in many cases, unintentionally been taking on more risk.

This increase in risk (and here we are particularly not limiting to volatility as the proxy for risk) has not solely occurred due to an increase in equity content – although this has had an impact. Rather the increase in risk seems to be related to the ever-increasing US equity position for many balanced investors. It is no secret that US assets have performed extremely well over the recent past, and that investors have progressively flocked to an ever-narrowing selection of stocks. It is worth mentioning that many multi asset funds in the 40-85% sector have an equity allocation nearing the upper band, coupled with an overweight toward US assets. This combination of increased equity risk (beta to global equities) and increased concentration risk could turn out to be a particularly dangerous place to be. In fact, we would argue that many funds in the flexible managed sector are more diverse than those in the 40-85% having a larger allocation to, for example, Asia and emerging markets.

Diversification as Key

We confess we have been guilty of referencing the underperformance of income stocks frequently over the past few months, but the reason we have done this is to highlight the risks of holding assets which may be too concentrated or correlated with each other. The performance of the 20-60% benchmark overall has been dire, due principally to the over reliance on income products. The point we are attempting to stress here is that it is noticeable that each of the IA Mixed Asset sectors has significant biases within them, biases that are in most cases yet to impact negatively on returns.

As ever, we believe that much of the answer is genuine diversification and by being aware of these biases and positioning our portfolios accordingly, we feel we can provide more consistent and balanced investments – relative to their respective benchmarks.

This communication is designed for Professional Financial Advisers only and is not approved for direct marketing with individual clients.

The MPS range portfolio performance is produced using the preferred share classes, this may differ from platform to platform.

The MPS range is shown net of fund fees only, they do not incorporate platform costs, adviser’s client fee or DFM service charge.

Past Performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise and investors may get back less than they invested. Risk factors should be taken into account and understood including (but not limited to) currency movements, market risk, liquidity risk, concentration risk, lack of certainty risk, inflation risk, performance risk, local market risk and credit risk.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IAM 254.8.20